Pinned

6d •

🚀 Premium Live Call Recap: GetRunway.Trade Updates (July 29)

In yesterday’s live session, we covered critical updates on our development roadmap, infrastructure, and current market positioning. Here are the key takeaways: 🔄 Trading Agent Migration We are migrating our trading agent from Hyperliquid to GMX. This shift is essential to mitigate regulatory risks and ensure we are operating on a completely permissionless platform. 🛠️ Infrastructure Strategy We’ve decided to keep our current Telegram-based trade tracking system for now instead of migrating to Google Cloud. This keeps operations lean so we can focus on building a verified performance track record before scaling up our tech stack. 📉 Market Strategy: Scaling Short Outlook: Bearish on Bitcoin ($BTC) and Ethereum ($ETH). Execution: Actively scaling into short positions at $15,000 per day through end of July. Goal: Reaching our full short position by the first week of August. 📊 Macro Outlook We are keeping a close eye on rising bond yields, which continue to signal heightened risk for the broader equity market. ⚡ What’s Next? My current focus is finalizing the agent’s readiness for mainnet execution. 💬 Over to You: What’s your take on the current market setup? Drop your thoughts and strategies in the comments below! 👇

Pinned

Jul '25 •

Welcome to DeFi U!

Hello everyone and welcome. As we begin building out DeFi University together, please know that any ideas you may have for a new tool, a new live call, a new course, anything that you'd like to build or incorporate in to add more value for us, the community members, that is 100% a yes here. This community is AI first, which simply means that we learn together how to use AI tools to build what will generate more value for us, the community members. We hope to foster an environment of learning and growth in many different areas of life within our DeFi University community, and now with these new AI tools any suggestion that any member has which will add value can quickly be built out and incorporated in. It's a very exciting and transformative time that we live in. To foster a sense of community spirit, please introduce yourself in the general chat as you join, and share a bit about yourself so that we can all get to know one another better. Live calls in the community take place every day Monday through Friday and they are open to all members. See you on the next live call and in the DeFi U chats! -David

Apr 2 •

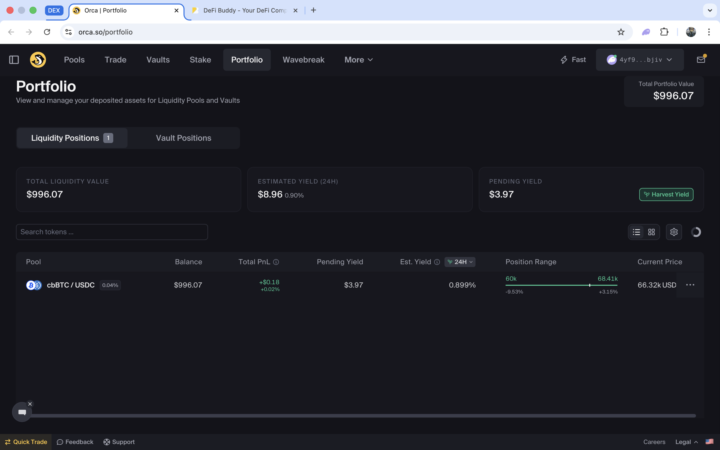

Public Portfolio

Yesterday, I started a Public Portfolio (no joke). I will show every step I make. I opened a single sided LP $1000 cbBTC/USDC and I will document every step on X.

Mar 6 •

🤖 The Invisible Edge: How Algorithmic Bots Are Outsmarting Human Intuition on Polymarket

Hey fam! 👋 The 15-minute BTC and ETH markets on Polymarket have become the most high-velocity arena in the crypto-prediction ecosystem. 🚀 To the retail trader, these are five-minute bursts of adrenaline fueled by: 🌊 "Vibes" 📱 Social media sentiment 🎲 The hope of catching a trend But while the "gut feeling" crowd is busy tweeting about moonshots, a silent layer of automated trading bots is reading the WebSocket feed, identifying Order Flow Imbalances (OFI) before a single price candle even moves. 🤖 🎯 This Isn't Prediction — It's Extraction This isn't a game of prediction; it's a game of sub-second extraction. Behind the curtain of the order book, bots are using pure mathematics to exploit the lag between human emotion and cold, hard probability. 🧮 Let me show you the 5 invisible edges that bots are using to print money while retail trades on vibes. 👇 💵 1. The "Dollar Rule" That Retail Panic Frequently Breaks In a binary prediction market, there is one non-negotiable law of physics: The price of a "YES" token + the price of a "NO" token must ALWAYS equal exactly $1.00. 📏 This is Invariant Arbitrage, and it is the bot's primary tool for harvesting "retail panic." 🎯 😱 When Panic Breaks the Math When news breaks — a sudden liquidation cascade or a macro data release — emotional takers flood one side of the market. This creates order book fragmentation where: $0.62 + $0.41 ≠ $1.00 ⚠️ For the bot, this is a directionally neutral gift. It doesn't care who wins; it only cares that the math is broken. 🤑 🎰 The Two Arbitrage Scenarios Case A (Buy-Merge): When the combined ask prices are < $1.00 📉 Example: YES token ask: $0.58 NO token ask: $0.40 Total: $0.98 (less than $1.00!) Bot action: Buy YES at $0.58 ✅ Buy NO at $0.40 ✅ Merge both tokens → receive $1.00 💰 Net profit: $1.00 - $0.58 - $0.40 - fees = ~$0.01-$0.02 ✅ Case B (Mint-Split-Sell): When the combined bid prices are > $1.00 📈 Example: YES token bid: $0.63 NO token bid: $0.42 Total: $1.05 (more than $1.00!)

23d •

🚀 Premium Live Call Recap: Maple Finance & The Canton Ecosystem

We dove deep into the latest shifts in institutional DeFi on our latest call. Here’s the high-level breakdown of the session for those who couldn't make it. 🍁 Maple Finance: Pivot & Perspective Maple has completed its transition from unsecured lending to a secure institutional gateway architecture. While the infrastructure is significantly improved, the current yield offerings (syrup USDC/USDT) are not currently justifying the associated borrower risks. - The Verdict: We are looking for significantly higher yields before considering deployment. - Correction: Reports circulating that Maple acquired Coinme and Sequence were incorrect; that was a metadata scraping error regarding a Polygon Labs deal. 🔒 Alpend & The Canton Network The focus shifted to Alpend, which leverages the Canton network to offer compliant, private credit workflows for large institutions (like Goldman Sachs and HSBC). - The Privacy Moat: Alpend uses "activity markers"—cryptographic proofs of economic weight—to claim network rewards without exposing sensitive user collateral or position data. - Network Discipline: The Canton network prioritizes economic discipline over "liveness." It uses aggressive L1 interventions and "kill switches" to protect monetary policy if data mismatches occur. 📉 CC Token Economic Outlook The Canton coin (CC) is currently inflationary and trading below its 200-day moving average. - The Path Forward: The chain generates ~$2.5M in daily revenue, but this isn't yet enough to offset the current inflation rate. - The Catalyst: We are watching the growth of the broader Canton ecosystem (Temple, Kantex, Acme, Helios, etc.). As these protocols go live, they act as a "virtuous cycle" sink for CC, which is necessary to reach a positive burn-mint equilibrium. ⏭️ Next Up We are setting our sights on specific strategies to optimize exposure. For our next session, we will be: - Deep-diving into Ditto: Analyzing its role in tokenized yield vaults. - Reviewing Wallets: Identifying the best options for spot exposure to CC and utilizing it within Canton DeFi.

1

0

1-30 of 500

skool.com/defiuniversity

Master DeFi from beginner to advanced. Security-first curriculum, live mentorship, gamified learning. Join us and build DeFi expertise safely.

Leaderboard (30-day)

1

+3

2

+3

3

+2

4

+1

5

+1

Powered by