Write something

14d •

What's the Best Way to Build a Solid Buyers List?

There are at least a dozen ways to build a strong buyers list. You want buyers who are hungry for deals, able to move quickly and clear on what they want. My current top 3 methods for finding buyers I can count on: - InvestorBase - REIA meetups - "Goldilocks" agents: Not your hot top producers and team leaders, but not agents who've only sold one deal in the past 12 months. You want agents in the middle of the pack who are active, investor-friendly, and hungry for deals These are what's working best for me as of today. What's works best for you?

0

0

Jun 4 •

Which to Get First - Deals Under Contract, or Cash Buyers?

A lot of would-be successful wholesalers struggle with this question. I see it as a chicken and egg scenario. I've made over 300 offers since January of this year. Out of those, I got four house deals u/c, thinking they'd be no-brainers for buyers. What I discovered is (a LOT) more buyer reluctance and wariness of the current market than I'd imagined. I released every one even before my EMD deadline had passed. All agents were appreciative of the effort and swift decision during the DD period. However if I hadn't gone under contract and really got a sense of what the few buyers I'm in touch with at this point (my #1 priority right now is building that bench) were feeling, I'd be way less in touch with my market and what really flies in the acquisition offers I'm making. What do you see as your greatest hurdle to successful deal-making at this point?

0

0

May 31 •

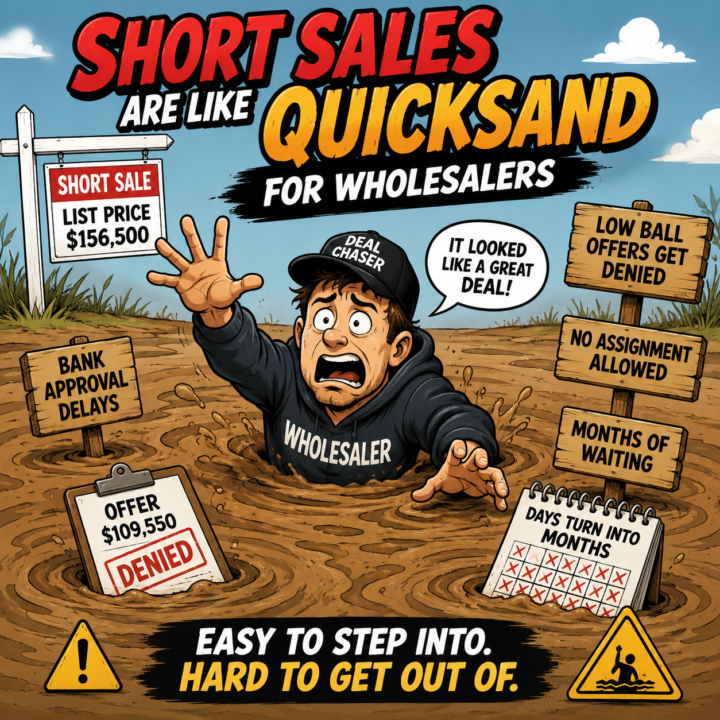

Are Short Sales Worth Pursuing as a Wholesaler?

Received this response from the listing agent to my offer at $109,550: "Well will you go to $156,500 with no assignable contract? Otherwise it will automatically be denied by the bank with this being a short sale (with appraisal in file)." So, are short sales worth pursuing as a quick cash flow strategy? The answer, especially if you are early in your investing journey is an unequivocal NO. Let us count the reasons why: 1. 𝗕𝗮𝗻𝗸𝘀 𝗔𝗿𝗲 𝗡𝗼𝘁 𝗠𝗼𝘁𝗶𝘃𝗮𝘁𝗲𝗱 𝗦𝗲𝗹𝗹𝗲𝗿𝘀: A distressed homeowner may be motivated, but the bank usually isn't. (Or at least tries to make like they're not.) They're just trying to minimize loss and justify the payoff internally. 2. 𝗔𝘀𝘀𝗶𝗴𝗻𝗺𝗲𝗻𝘁𝘀 𝗔𝗿𝗲 𝗙𝗿𝗲𝗾𝘂𝗲𝗻𝘁𝗹𝘆 𝗥𝗲𝘀𝘁𝗿𝗶𝗰𝘁𝗲𝗱: Many short sale approval letters prohibit assignments, double-close markups, same-day resales, or even resale within a certain period. 3. 𝗔𝗽𝗽𝗿𝗼𝘃𝗮𝗹 𝗧𝗮𝗸𝗲𝘀 𝗙𝗼𝗿𝗲𝘃𝗲𝗿: Wholesaling is all about speed, certainty and momentum. Short sales are all about waiting, more waiting and additional waiting. 4. 𝗧𝗵𝗲 𝗦𝗽𝗿𝗲𝗮𝗱 𝗚𝗲𝘁𝘀 𝗦𝗾𝘂𝗲𝗲𝘇𝗲𝗱: Suppose ARV = $250k, rehab = $60k and you think the deal is worth $120k. The bank appraisal says $165k. Guess who usually wins? The bank. Oops, there went your spread. 𝗠𝗼𝗿𝗮𝗹 𝗼𝗳 𝘁𝗵𝗲 𝘀𝘁𝗼𝗿𝘆: Except in rare instances where it's worth your while to exercise extreme patience, stay away from short sales. (See attached)

0

0

Mar 26 •

Q: What’s the Best, Fastest, FREE Lead Source for Wholesaling?

Short answer: There isn’t just one. But there are a handful that consistently work — especially when you’re starting out with more hustle than budget. 𝗠𝘆 𝗖𝘂𝗿𝗿𝗲𝗻𝘁 𝗙𝗮𝘃𝗼𝗿𝗶𝘁𝗲𝘀 (𝗕𝗲𝗴𝗶𝗻𝗻𝗲𝗿-𝗙𝗿𝗶𝗲𝗻𝗱𝗹𝘆) 𝟭. 𝗔𝗴𝗲𝗻𝘁 𝗜𝗻𝗯𝗼𝘂𝗻𝗱 (𝗠𝗟𝗦 𝗿𝗲𝗹𝗮𝘁𝗶𝗼𝗻𝘀𝗵𝗶𝗽𝘀) Build relationships with agents → they bring you deals 👉 Fast, scalable, and relationship-driven 𝟮. 𝗗𝗿𝗶𝘃𝗶𝗻𝗴 𝗳𝗼𝗿 𝗗𝗼𝗹𝗹𝗮𝗿𝘀 Find distressed properties no one else is targeting 👉 Sweat equity → high-quality leads 𝟯. 𝗚𝗼𝘃𝗲𝗿𝗻𝗺𝗲𝗻𝘁 𝗟𝗶𝘀𝘁𝘀 Pre-foreclosures, code violations, evictions 👉 Built-in motivation (if you approach it right) 𝟰. “𝗗𝗶𝗴𝗶𝘁𝗮𝗹 𝗕𝗮𝗻𝗱𝗶𝘁 𝗦𝗶𝗴𝗻𝘀” Facebook groups, local posts, simple outreach 👉 Quick conversations, zero cost 𝟱. 𝗦𝗘𝗢 / 𝗔𝗜 𝗥𝗲𝗳𝗲𝗿𝗿𝗮𝗹𝘀 (Advanced but powerful) 👉 Slower ramp, but long-term inbound machine if done right 𝟲. 𝗘𝗺𝗮𝗶𝗹 𝗕𝗹𝗮𝘀𝘁𝗶𝗻𝗴 (Learning this now, a particular of mine b/c of my background in email marketing) 👉 Hearing strong things, still testing 𝗧𝗵𝗲 𝗥𝗲𝗮𝗹 𝗔𝗻𝘀𝘄𝗲𝗿 𝗠𝗼𝘀𝘁 𝗣𝗲𝗼𝗽𝗹𝗲 𝗠𝗶𝘀𝘀 It’s not the list. It’s your ability to: • Start conversations • Build trust • Follow up consistently Give two investors the same list… One makes money. One doesn’t. My Take for Beginners If I had to start over with $0: 👉 Agent relationships 👉 Driving for dollars 👉 Facebook / digital bandit signs Stack those daily and you’ll get leads. 💬 Question: What’s been your BEST lead source so far — or what are you testing right now?

0

0

Feb 22 •

"What Are the Pros and Cons of Sub-to Deals?"

Saw this question recently in a post. It's a great question. And one every serious investor should be able to answer clearly. First, full transparency: I’m not an attorney, and I haven’t personally closed a sub-to deal yet. I’ve done several direct-to-seller purchases and seller-financed deals, and I’ve studied creative finance pretty extensively… but I’m not claiming expert status here. 𝗧𝗵𝗮𝘁 𝘀𝗮𝗶𝗱, 𝗶𝗳 𝘆𝗼𝘂 𝘀𝘁𝗿𝗶𝗽 𝗮𝘄𝗮𝘆 𝘁𝗵𝗲 𝗬𝗼𝘂𝗧𝘂𝗯𝗲 𝗵𝘆𝗽𝗲 𝗮𝗻𝗱 𝗹𝗼𝗼𝗸 𝗮𝘁 𝗶𝘁 𝘀𝗼𝗯𝗲𝗿𝗹𝘆, 𝗵𝗲𝗿𝗲’𝘀 𝘁𝗵𝗲 𝗿𝗲𝗮𝗹𝗶𝘁𝘆: In a subject-to transaction, the loan stays in the seller’s name.Title transfers to the buyer. And that structure creates real risks for the seller. Here are the biggies: 𝟭. 𝗖𝗿𝗲𝗱𝗶𝘁 𝗗𝗮𝗺𝗮𝗴𝗲. 𝗶𝗳 𝘁𝗵𝗲 𝗕𝘂𝘆𝗲𝗿 𝗗𝗲𝗳𝗮𝘂𝗹𝘁𝘀. If the buyer misses payments, it hits the seller’s credit. Period. Foreclosure risk remains theirs. 𝟮. 𝗧𝗵𝗲 𝗗𝘂𝗲-𝗼𝗻-𝗦𝗮𝗹𝗲 𝗖𝗹𝗮𝘂𝘀𝗲. Most mortgages contain a clause allowing the lender to call the loan due if ownership transfers. It's not always enforced… but it absolutely can be. 𝟯. 𝗟𝗼𝘀𝘀 𝗼𝗳 𝗖𝗼𝗻𝘁𝗿𝗼𝗹. The seller no longer owns the property, yet the mortgage liability stays with them. 𝟰. 𝗗𝗲𝗯𝘁-𝘁𝗼-𝗜𝗻𝗰𝗼𝗺𝗲 𝗜𝗺𝗽𝗮𝗰𝘁.That loan still shows on their credit, potentially limiting their ability to qualify for another home. 𝟱. 𝗣𝗿𝗼𝗽𝗲𝗿𝘁𝘆 𝗠𝗶𝘀𝗺𝗮𝗻𝗮𝗴𝗲𝗺𝗲𝗻𝘁 𝗥𝗶𝘀𝗸. If the buyer neglects insurance, maintenance, or abandons the property, the seller could end up tied to a deteriorating asset. Now, can these risks be mitigated? Yes. • Loan servicing companies • Proper insurance structure • Thorough buyer vetting • Clear written agreements • Attorney review And here’s the real question… 𝙄𝙛 𝙮𝙤𝙪’𝙧𝙚 𝙥𝙤𝙨𝙞𝙩𝙞𝙤𝙣𝙞𝙣𝙜 𝙮𝙤𝙪𝙧𝙨𝙚𝙡𝙛 𝙖𝙨 𝙖 𝙥𝙧𝙤𝙗𝙡𝙚𝙢 𝙨𝙤𝙡𝙫𝙚𝙧 𝙛𝙤𝙧 𝙨𝙚𝙡𝙡𝙚𝙧𝙨, 𝙘𝙖𝙣 𝙮𝙤𝙪 𝙘𝙡𝙚𝙖𝙧𝙡𝙮 𝙖𝙧𝙩𝙞𝙘𝙪𝙡𝙖𝙩𝙚 𝙩𝙝𝙚𝙨𝙚 𝙧𝙞𝙨𝙠𝙨 𝙗𝙚𝙛𝙤𝙧𝙚 𝙩𝙝𝙚𝙮 𝙖𝙨𝙠? Because if you can’t explain the downside, you’re not advising… you’re pitching. And that erodes trust. You’ve probably seen creators like Pace Morby advocate heavily for sub-to as a powerful tool. And it can be. Used responsibly, it absolutely has its place. But there is a less risky alternative worth considering:

0

0

1-6 of 6

powered by

skool.com/realfreeco-3644

Learn how to create profitable deals like clockwork. Clear frameworks. Real numbers. No hype.

Suggested communities

Powered by