Activity

Mon

Wed

Fri

Sun

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

What is this?

Less

More

Memberships

multifamily

342 members • Free

4 contributions to multifamily

Nov '24 •

Our Toughest Deal Refinances to Agency - 3 years in the making

This was the most difficult project in our career, and I’m proud of this story of perseverance and ultimately preservation of capital. In a time where there is much negativity towards Syndications and multifamily, this story hopefully gives hope to the operators out there doing the right thing, giving every bit of smarts and execution to protect capital. This story is a save. I don’t know many other operators that would have been able to pull off what we did and the challenges we faced, how we survived and thrived. Our strength as GP guarantors at Sharpline, our track-record, our relationships with Freddie and Fannie were the key. It’s a testament to Sharpline and the commitment of our team as well as the patience and belief from our investors. I want this post to be a reality check and not considered bragadocious but give homage to the people in Sharpline and the many partners (lenders, vendors, consultants, investors) that helped get this insurmountable project to where it is today. Here we go. 3 years ago we bought this as a heavy value-add post covid. We couldn’t get new roofs that were leaking for 7 months, so this inhibited our reposition to improve the property, which kept some of the bad elements at the community there longer than we wanted. Fire property management company 1 , Fire property management company 2 (proverbial jump out frying pan into the fire, scary). Decided to self-manage project. This was in an early stage of our self-management journey about 2 years ago (we now self-manage 1500+ units). We purchase one half of the project with cash and the other with a bridge loan with floating rate debt (our only floating rate Sharpline has ever done, we didn’t buy a rate cap either, not smart) 4% bridge loan. We begin to execute capex plan successfully (we ripped the mansards off #MansardSlayer). The process of reposition took longer than we liked because of construction delays and bad PM companies, but we ultimately had the safety net of the 24 unit townhouse project that was getting higher occupancy that we purchased with cash as part of the syndication. So we refi’d the 24 unit with a local bank and GPs personally guaranteed the loan as we continued to do projects. This allowed us to free up liquid capital to continue executing to get higher occupancy, but we were still not there yet. We were at 65% overall occupancy on 128 units and the community was improving.

2 likes • Apr 20

Thank you so much for sharing this story Chris! I think it's amazing that you had all this going on and were still managing all your other SharpLine properties! When I first invested in SharpLine, I knew very little about you. I'm confined to a power chair, so I had no way to visit properties, or meet you in person. I invested with SharpLine, solely on the advice of Jeff Gebhart, a long-time childhood friend, who's opinion I trust. As an investor in other SharpLine deals, this story gives me a great sense of confidence, that your team will buckle down and do what is necessary, to preserve our investment! 💯

1 like • Jun 2

Hey Chris, Have you put this story to video? Might make a good marketing piece for SharpLine... 🤔

Apr 19 •

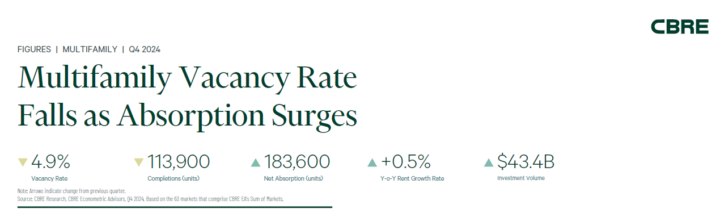

Historic Absorption in 4Q2024 for Apartments - KC Focus

🏢 Q4 2024 Multifamily Market Overview – RECORD PERFORMANCE 🔥 Record-Setting Absorption - 183,600 units absorbed in Q4 2024 — the highest Q4 total ever recorded by CBRE. 🏙️ Every Market Grew - All 69 tracked markets recorded positive net absorption — first time on record for Q4. - Top Q4 markets: 📉 Vacancy Rate - Dropped to 4.9%, below the long-term average of 5.0%. - 63 markets had vacancy rate declines QoQ (only two increased). - Providence (2.4%) and New York (3.1%) posted the lowest vacancy. 💰 Investment Volume - $43.4B in Q4, up 59% YoY. - Annual 2024 total: $142.6B, a 19% increase over 2023. - Multifamily accounted for 36% of total CRE investment for both Q4 and full-year 2024. - Cap rates compressed to 5.4% in Q4 (down from 5.6% in Q3). 📊 Rent Trends - Effective rent growth averaged 0.5% YoY in Q4. - Midwest led regional rent growth at 2.8%, followed by Northeast (2.3%) and Pacific (0.4%). - Negative rent growth persisted in Mountain (-2.8%), South Central (-2.5%), and Southeast (-1.1%), though moderating. 🏗️ Construction Pipeline - 608,400 units under construction as of Q4 (3.4% of inventory). - New York (58,800 units), Dallas (34,100), and Austin (27,800) lead in new supply. KC Focus 📊 Market Fundamentals - Net Absorption: In Q3 2024, Kansas City recorded a net absorption of 1,635 units, marking a 70% increase compared to the same period in 2023. Year-to-date absorption reached 4,580 units, significantly outpacing the 2,974 units delivered during the same timeframe. MMG Real Estate Advisors - Occupancy: The average occupancy rate rose to 93.5% by the end of Q3 2024, with submarkets like Johnson County achieving rates as high as 95.1%. MMG Real Estate Advisors - Rent Growth: Average rents increased by 3.3% year-over-year in Q3 2024, placing Kansas City among the top-performing U.S. markets for rent growth. Submarkets such as Johnson County and Leavenworth County reported rent increases of 4.8% and 4.1%, respectively. MMG Real Estate Advisors

1 like • Apr 19

Very interesting! 🤔

Mar 5 •

You missed it. It's Official. Apartment Sales Rise First Time in 3 Years,

Apartment sales rise first time in 3 years. Int rates lowered. Recession looming. “Multifamily is bad” “Syndicators are worse” It’s time to get in the game again for those that sat on the sidelines. We are self managed and team is stronger than ever ready to continue to take advantage of this dislodgement in the market. We have been getting access to newer product more than we have ever before. Because we stayed in the game we are getting the first call. The tailwind has begun. https://www.multifamilydive.com/news/apartment-transaction-multifamily-property-vales-cap-rates/741397/?blaid=7150630&fbclid=IwY2xjawI1NsNleHRuA2FlbQIxMQABHb1voXjiOLNmcAokJ5Y0yOFI1l84sXUCMPlgWfsl3hZTA53wkryj_ioM5Q_aem_1wi_NCm8Yf5521JrXV96-g

1 like • Mar 6

Full confidence in SharpLine, for sure! 💯 Can't wait to get equity out of the Columbus 2-Pack and put it to work on new opportunities!

Jan 10 •

Bottom for Office in 2025?

What do you think? This metric is pretty interesting. (PS no we are not buying office now ) https://product.costar.com/home/news/shared/1377331389?culture=en-US&source=sharedNewsEmail&t=eyJhbGciOiJIUzI1NiIsInR5cCI6IkpXVCJ9.eyJjdWx0dXJlQ29kZSI6ImVuLVVTIiwiaWF0IjoxNzM2NTM2Njg0fQ.XFsdgCh96e4JMfhjMDgXrImD0GeGDaWqMzQj1gOg3ng

0 likes • Jan 10

It would be nice to see the dollar amount of rented space, compared to 2019 (adjusted for inflation) That would be a better comparison than square feet available. 🤔 There may be a lot of discounted space out there.

1-4 of 4

Active 197d ago

Joined Sep 12, 2024

Powered by