Activity

Mon

Wed

Fri

Sun

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

What is this?

Less

More

Memberships

Scholar Career Network

295 members • Free

Data and Ai Automations

1.5k members • Free

Dissertation Help Community

3.3k members • Free

Let's Master English

5.3k members • Free

Study Smarts

122 members • Free

Studicata

16.8k members • Free

Superior Students

20.6k members • Free

The DIY Engineering Club

2.5k members • Free

Mechanical Engineering Mastery

308 members • Free

44 contributions to The Energy Data Scientist

6d •

Interactive Map with Energy Projects

Found and sharing an interactive energy infrastructure map hosted by GlobalGrid2050. It maps renewable energy and storage projects for the United Kingdom only. It is including solar PV, onshore and offshore wind, and battery storage . It is getting them from the UK's Renewable Energy Planning Database (REPD). You can filter projects by technology type, planning status (from "in planning" through to "operational"), and capacity range in MW. It also overlays grid infrastructure like substation density and water utility locations. It is a useful tool for visualising the spatial relationship between generation, storage, and network assets. https://globalgrid2050.com/repd_atlas_grid_model/

0 likes • 5d

Thanks. Maps all the projects on a map so we know the geographical and other details.

6d •

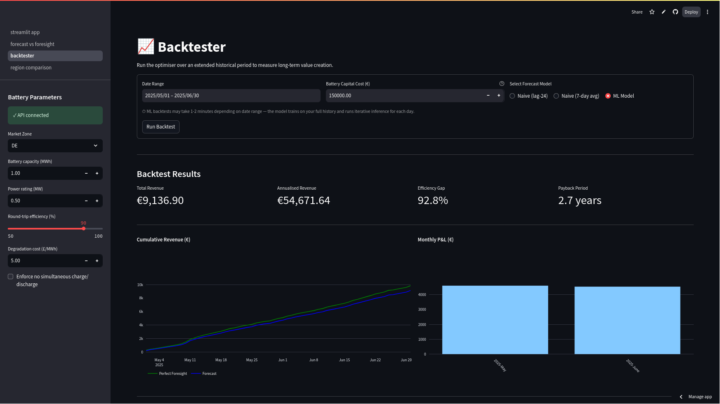

Battery Arbitrage Project

Hi everyone! I've been exploring the battery arbitrage space for the past few months and wanted to share my most recent project: I built a battery arbitrage backtester that finds the optimal charging schedule using LP, and tests it against three forecasting approaches(two rolling averages, one ML) and measures how much of the theoretically available market value was captured. I pooled data from different EU market zones to train a LightGBM model and trained a separate one for Britain, which is why the rolling average model overtook the ML model in Germany's results, for example, which was an interesting result. Article and Streamlit dashboard to play around with here if anyone's curious: https://kilowatthours.substack.com/p/building-a-battery-arbitrage-backtester https://bessarbitragedemo.streamlit.app/ I'm currently working on multi-battery coordination and whether batteries "knowing" more about the grid's topology can improve dispatch results, and using a neural network for the congestion signal. Curious to hear your feedback, and if anyone's working on battery optimization or grid ML, would love to connect.

1 like • 5d

Quite impressive . I like that you benchmarked against the theoretical market value instead of just reporting raw profits. That makes the results much easier to interpret. The Germany result is especially interesting because it shows where a simpler model can still win when transferability is limited. Have you looked at whether zone-specific feature engineering could close that gap for the ML model?

13d •

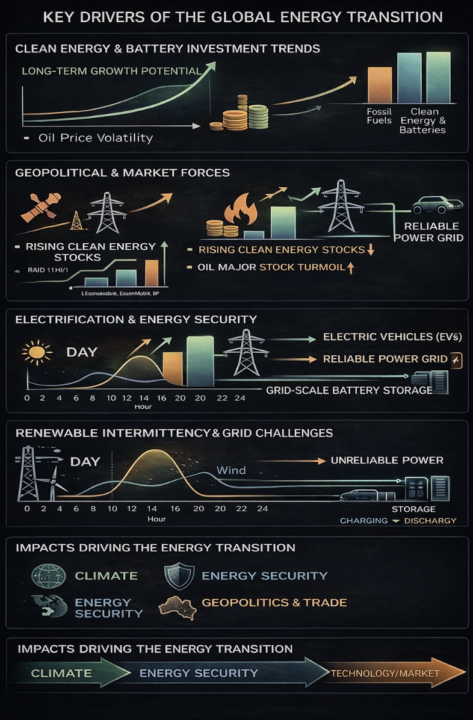

Energy Security and Batteries

Rising conflict and growing energy insecurity have made batteries, clean energy, and electrification more attractive as long-term investments than fossil fuels alone. Companies such as CATL, BYD, and Sungrow have benefited strongly, as battery and energy storage technologies support electric vehicles, renewable power, and grid reliability. The energy transition is increasingly being shaped not only by climate goals, but also by war, trade risks, and the need for stronger domestic energy security. A new report on this topic has now been published in Classroom, at the very end under “Energy Industry Support” , a special section featuring reports that explain the current status and key trends in the energy sector. The report explains these developments in clear, simple language, includes illustrative graphs, and shares official sources such as the Financial Times, Bloomberg, Wall Street Journal, The Economist, Forbes, and Investors Chronicle. This report can be downloaded for your use. See the attached screenshot.

0 likes • 13d

This is a strong argument for why batteries matter now. They help countries rely less on unstable fossil-fuel imports. That gives them both strategic and economic value.

Mar 8 •

Notes from Recent Talks: Employment Trends

I pulled together some notes from recent discussions on employment conditions across countries, especially for energy/utility roles. Sharing here in case it helps anyone comparing markets. I have attached the Excel file. The file is broader employment/job-market comparison by country, and only one part of it is energy-related via the “Utility Sector Security” column.Useful if you’re comparing job stability vs compensation in the broader energy sector. Big picture: - USA = highest salaries, but weaker general job security and social safety net - UK / Australia = strong employment protections and very stable utility-sector roles - France = strongest labor protections and very hard to dismiss employees - Switzerland = very high salaries with a strong financial safety net

0 likes • Mar 8

True. NZ/Aus is as explained. .

Mar 3 •

Reminder: Global Energy Market & Job Search

Just a little reminder ! I was in an energy conference in Australia travelling, and it was about energy jobs. Here are some points from top recruiters (eg director of HR in Chevron, director of HR in Total etc): --> energy is a global marketplace. Companies in Australia/Europe/Asia/Africa/America hiring people from all over the world And they sponsor VISAs. And no lay offs! No AI threat. Energy is considered TOO critical and humans are needed. Also be careful with CVs!!! dont just send randomly ! Many people apply to 20, 50, even 100 jobs…And still get no response. Why? Because job application today is not about volume it’s about alignment. Are you: • Applying to roles that truly match your experience? • Reading the job description carefully? • Positioning yourself based on what the employer is actually asking for? • Following application instructions properly? One small mistake in your application can cost you an interview. So you must: • Apply strategically instead of randomly • Align your experience with job requirements • Structure strong application responses • Navigate remote, hybrid, and on-site roles confidently Job searching is competitive, but with the right approach, you can stand out. I strongly recommend you use the service of CV feedback here. Everytime you apply for a job! Don't just send a CV. Same for interview! And last: BELIEVE THAT YOU CAN GET THE JOB. Stop thinking negatively. Tell yourself "I DESERVE THIS JOB."

1-10 of 44

@kahu-ngata-5552

Renewables Researcher, Univ. of Auckland alumni - wind energy consultant for 10+ years

Active 5d ago

Joined Sep 20, 2025

Auckland, New Zealand