Activity

Mon

Wed

Fri

Sun

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

What is this?

Less

More

Memberships

Garage Truth – Learn-Fix-Grow

2.7k members • Free

The Trader’s Launchpad

191 members • $29/month

Financial Engineering School™

427 members • Free

Lifetime Income Ladder

115 members • $49/month

Art Of Mobility Live

457 members • $49/m

Built To Move

23 members • Free

One Movement

13 members • Free

Peakvest Society

12.7k members • Free

Invest & Retire Community

3.3k members • Free

20 contributions to Invest & Retire Community

2d •

Happy 2026 to all

Wishing everyone a great new year. Stay safe, focus on your health and invest wisely in 2026.

2 likes • 2d

Happy New Year , and wishing you the same.

2 likes • 23d

thanks for sharing

Nov '25 •

Happy Thanksgiving to you! :)

As we approach the end of the year, it is important to be grateful. This year has its downs (tariff war) and also its ups (subsequent recovery). Whether the market is up or down, or a V shape recovery, the most important thing is the people around you and the relationship you have with them. Money will come (as the overall market goes up by 10% per year). And it is important to treasure the little moments with our families, as we still can. Happy Thanksgiving! Here's the FINAL Black Friday discount to join Investing Accelerator, where you get an interest-free instalment over 12 months & 33% discount off the regular price: https://5mininvesting.thrivecart.com/black-friday After you join, you can schedule a free one-on-one call to ask any questions you have about your life, your situation and retirement. You can also use this call for technical support if you wish to have it later. I will set up a message / group chat to initiate the onboarding process. Cheers, Eric ---- Eric Seto Chartered Professional Accountant (CPA) Chartered Investment Manager (CIM) Founder of 5MinInvesting.com In December, my goal is to help 20 people without a financial background to master investing through Investing Accelerator. Investing Accelerator is designed for people without a financial background. The goal is to achieve 30% return per year. In the first phase, you will learn long term investing and targeting 30% for tax free compound growth. This will help accelerate your overall wealth. In the second phase, you will learn monthly passive income to provide a more predictable cash flow (target 30% per year) which can cover your expenses. This will help accelerate your retirement goals. Here's a step by step guide on how to join Investing Accelerator for free: https://www.skool.com/invest-retire-community-1699/how-to-join-investing-accelerator-for-free

5 likes • Nov '25

Happy Thanksgiving Eric and thank you everyone for sharing your trade , ideas and knowledge to become a better trader!!!

Aug '25 •

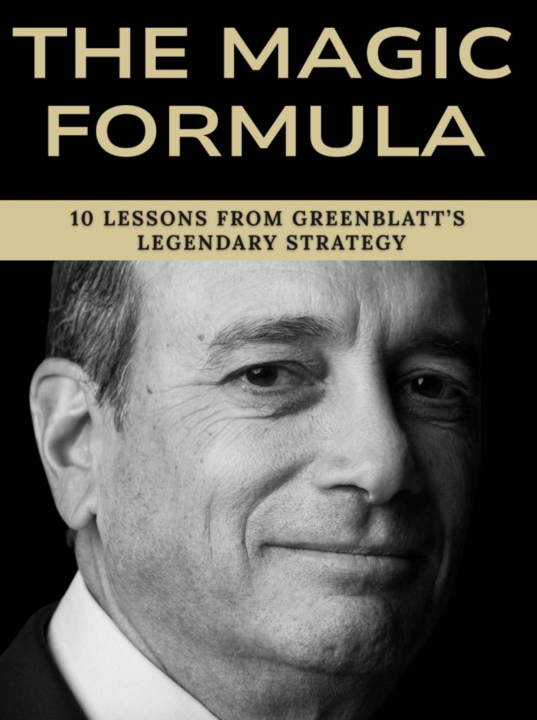

The Magic Formula

Joel Greenblatt averaged 40% annual returns. Not once. Not twice. But for over 20 years! He shared his exact method in The Little Book That Still Beats the Market. Here are the 10 biggest lessons: 1. Stocks aren’t lottery tickets 2. The market is moody 3. Good investing is boring 4. Buy great companies 5. But don’t overpay 6. The Magic Formula = quality + cheap 7. You will doubt the formula 8. Most investors fail this test 9. Simplicity beats complexity 10. You can do this

4 likes • Sep '25

Thanks for sharing

Sep '25 •

ROTH IRA & WHY YOU MUST KNOW IT IS A POWERFUL TOOL!

I have posted same topic under “What I Would Do If I were In My 20’s & Working (USA)?” Today, I will elaborate deeper on this topic. ROTH account is one of the most POWERFUL TAX-FREE strategies for retirement & inheritance portfolios available in the United States. (I believe similar vehicle is available in Canada.) ✅ PROS 1. Tax-Free Growth and Withdrawals. You contribute with after-tax money, but your investments grow tax-free. In retirement, all QUALIFIED (see note 1 below) withdrawals (contributions + earnings) are 100% tax-free. 2. No Required Minimum Distributions (RMDs): Unlike traditional IRAs, Roth IRAs don’t require withdrawals during your lifetime, allowing you to leave funds invested or pass them to heirs tax-free. 3. Flexible Withdrawals: You can withdraw your contributions (not earnings) at any time without penalty or taxes, providing liquidity for emergencies or other needs. 4. Estate Planning Benefits: Heirs inherit Roth IRAs tax-free, though they must take distributions within 10 years (post-SECURE Act rules). 5. Hedge Against Future Tax Hikes. If you expect to be in a higher tax bracket in retirement, a Roth IRA protects you by paying taxes now. Note 1: Very important to make qualify distributions which requires you to meet BOTH of the following conditions: 1. The 5-Year Rule. The Roth IRA must have been open for at least 5 tax years. The clock starts on January 1 of the year you made your first contribution (not the exact day). 2. A Qualifying Event (Age or Exception). One of these must also apply: You’re age 59½ or older, OR You’re disabled, OR You’re using up to $10,000 for a first-time home purchase (lifetime limit), OR Your beneficiary is making a withdrawal after your death. - Always verify your account’s status and consult IRS guidelines (e.g., IRS Publication 590-B at irs.gov) or a tax professional, as rules can be complex, especially for conversions or inherited Roth IRAs. ❌ CONS 1. No Upfront Tax Deduction as taxes paid upfront: Contributions are made with after-tax dollars, so there’s no immediate tax break, unlike traditional IRAs.

4 likes • Sep '25

Thanks for sharing 👍

1-10 of 20

Active 6h ago

Joined Dec 27, 2022

Powered by