Write something

Nov '25 •

🔥 Who’s ready for my SUPER SECRET landlord phone script?

The exact script I used to lock up not one… but TWO off-market fourplexes from owners who weren’t even thinking about selling. No agents involved. No competition. No bidding war. Just me → making a simple phone call → using a script so clean and effective it kept every landlord on the phone long enough for me to get: ✔️ a real conversation ✔️ a yes or no ✔️ and most importantly… their price Both deals closed. Both were off-market. And both came from THIS phone script. This is the same script I use today when I’m cold calling landlords for flips, creative deals, and off-market multifamily. If you want this script word for word, 👇 DM me “SCRIPT” down below. I’ll send it to you directly.

Dec '25 •

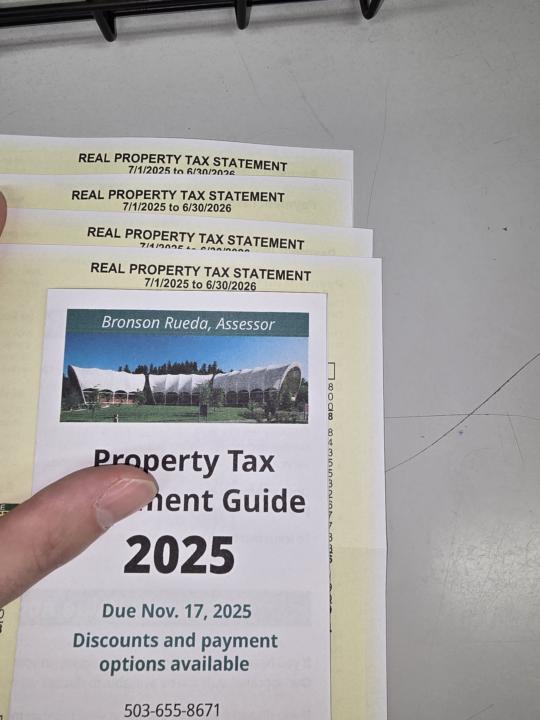

Are you ready to self-manage?

If you're not ready to deal with this you might want to hire someone.

1

0

Dec '25 •

I had to call the cops on one of my tenants 😬😬

https://youtu.be/D_NIHQMr34o?si=MrS1AqsS4FwADm94

0

0

Aug '25 •

Welcome to Small Multifamily Masters 🏘💼

This is for the long-game investors — the ones building cashflow and legacy through rentals. Inside we’ll talk about: How to analyze duplexes, triplexes, and fourplexes 🔍 Creative financing strategies 💡 Systems for management and scaling 📈 How to leverage equity to grow faster 🔑 The goal? To help you build financial freedom one property at a time. 👉 Start by introducing yourself and sharing: What’s your buy-and-hold goal over the next 12 months?

1-15 of 15

powered by

skool.com/pnw-real-estate-launchpad-2450

Join Portland investors learning flips, wholesales & rentals. Follow real projects, ask questions & start your first deal.

Suggested communities

Powered by