Write something

4h •

Poll: Would You Find Value In Watching Live Deal Reviews?

One of the biggest gaps between learning acquisitions and actually buying a business is seeing how experienced operators think through real situations. Every acquisition is different. A seller changes their mind. A lender asks unexpected questions. Due diligence uncovers new risks. The original deal structure no longer works. That's where judgment is developed. I'm considering opening a limited number of live sessions where members can observe actual deals being evaluated by our community. We'd walk through real financials, discuss valuation, evaluate risk, explore financing options, review negotiation strategies, and talk through the decisions being made along the way. These wouldn't be hypothetical case studies. They would be real acquisition opportunities, discussed in real time, with the goal of helping members understand not only *what* decisions are made, but why they're made. Before putting something like this together, I'd love your feedback. Would you participate in live deal review sessions?

Poll

Cast your vote

0

0

3d •

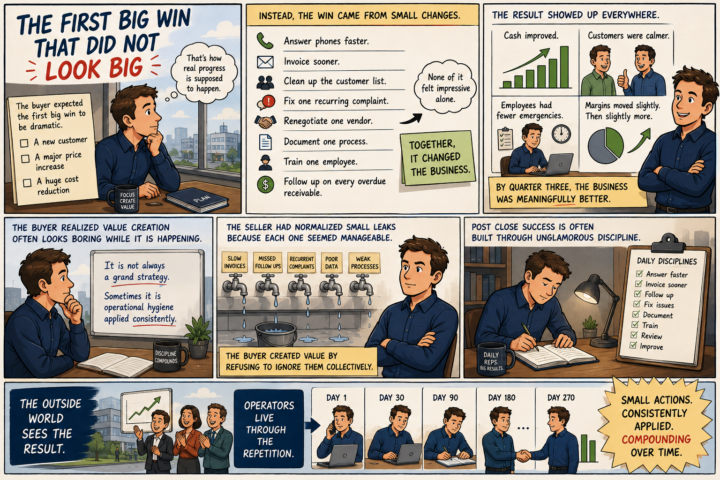

The Exit He Started Building Before He Wanted To Sell

When the buyer acquired the business, selling it was the last thing on his mind. He had spent years searching for the right opportunity, and now his focus was on building, improving, and growing what he had just purchased. Yet only six months after closing, he began preparing the company as though a sophisticated buyer might review it at any moment. Not because he wanted to sell. Because he realized the discipline required to build an attractive business was the same discipline required to build a better one. He started with the fundamentals. Monthly financial statements became more consistent and easier to understand. Add-backs were documented clearly instead of relying on memory. Operating processes were written down, customer concentration was tracked, vendor contracts were organized, employee responsibilities were clarified, equipment maintenance was logged, and key performance indicators were reviewed regularly. Even management meetings began producing written notes and action items. At first, the team questioned why so much documentation was necessary. They weren't planning to sell the company, so it felt like unnecessary work. Over time, however, the benefits became impossible to ignore. Decision-making became faster because reliable information was readily available. Conversations with lenders became more productive because the business could answer questions with confidence. New employees were onboarded more quickly, reporting became cleaner, and planning for future growth required far less guesswork. The buyer eventually realized that exit readiness had very little to do with exiting. It was about building a business that was understandable, transferable, and financeable. In many ways, the characteristics that make a company attractive to a future buyer are the very same characteristics that make it a better business to own today. Looking back, one lesson stood above the rest. Enterprise value isn't created only through higher revenue or larger profits.

9d •

The Employee He Never Knew He Needed

Three weeks after closing, Chris received a text message that changed everything. One employee had resigned. At first, it didn't seem like a big deal. But over the following days, customer appointments were missed, invoices stopped going out, and employees kept asking the same question: "Did Maria handle that?" Chris soon realized he hadn't just lost an employee. He had lost the person holding the business together. A powerful lesson in key person risk, institutional knowledge, and why due diligence goes far beyond the financial statements.

8d •

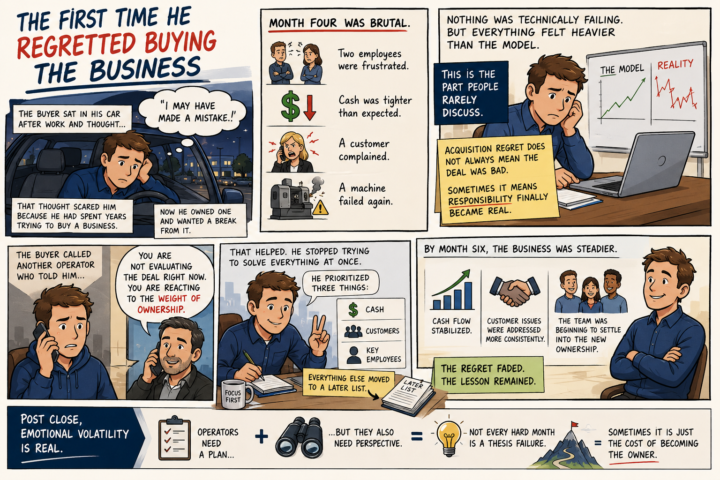

The First Time He Regretted Buying The Business

Month four was brutal. Two employees were frustrated. Cash was tighter than expected. A major customer complained, and a machine that had already caused problems failed again. At the end of another long day, the buyer sat alone in his car and thought something he had never expected to think. *"I may have made a mistake."* The thought scared him. He had spent years trying to buy a business. He had searched for deals, analyzed financials, negotiated with sellers, raised capital, and imagined what life would be like when he finally became an owner. Now he owned the business. And some days, he wanted a break from it. Nothing was technically failing. Revenue hadn't collapsed. Customers weren't leaving in large numbers. The company wasn't approaching bankruptcy. But everything felt heavier than it had in the model. That is the part of business ownership people rarely discuss. Acquisition regret doesn't always mean the buyer purchased a bad business. Sometimes it means the responsibility of ownership has finally become real. The buyer called another operator and explained what was happening. After listening, the operator told him something that changed his perspective. *"You're not evaluating the deal right now. You're reacting to the weight of ownership."* That conversation helped him recognize that he had been trying to solve every problem at once. So he stopped. He narrowed his focus to three priorities. Cash. Customers. Key employees. Everything else went onto a list to address later. The business didn't suddenly become easy. The problems didn't disappear overnight. But the buyer became more focused. By month six, cash flow had stabilized. Customer issues were being addressed more consistently. The team was beginning to settle into the new ownership. The regret faded. The lesson remained. Post-close, emotional volatility is real. Operators need financial models, operating plans, and systems. But they also need perspective. Not every difficult month means the acquisition thesis was wrong.

6d •

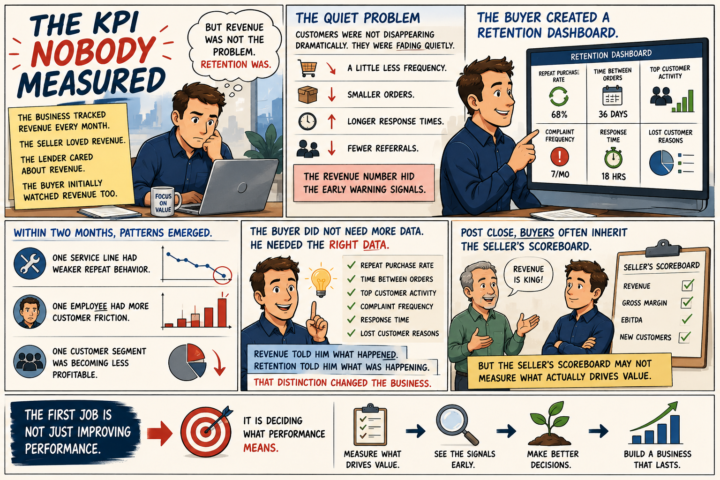

The KPI Nobody Measured

Every month, the business tracked one number above all others. Revenue. The seller loved watching revenue. The lender cared about revenue. When the buyer took over, he naturally focused on revenue too. At first, everything looked fine. Sales were holding steady, and nothing on the income statement suggested the business was in trouble. But something didn't feel right. Customers weren't leaving in large numbers. They were quietly becoming less engaged. They ordered a little less frequently. Their average purchases became smaller. Response times were getting longer. Referrals slowed down. Complaints weren't increasing dramatically, but they were becoming more common. None of those warning signs showed up on the monthly revenue report. The buyer realized he wasn't measuring what actually mattered. So he built a new dashboard. Instead of only tracking revenue, he began monitoring repeat purchase rates, time between customer orders, activity from top accounts, complaint frequency, response times, and the reasons customers stopped doing business with the company. Within two months, patterns began to emerge. One service line had noticeably weaker customer retention. One employee generated far more customer friction than the rest of the team. One customer segment, while still producing revenue, was becoming increasingly difficult to serve profitably. The buyer didn't need more information. He needed better information. Revenue told him what had already happened. Retention showed him what was happening right now. That single shift changed how he managed the business. One of the biggest post-close lessons was this: Buyers often inherit the seller's scoreboard. But the seller's scoreboard may not be measuring the things that actually create long-term value. Before you can improve performance, you have to decide what performance truly means.

1-30 of 96

powered by

Suggested communities

Powered by