Write something

1d •

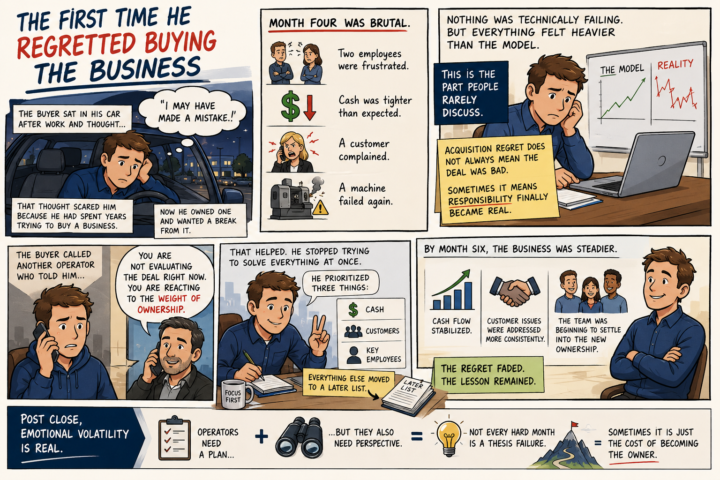

The First Time He Regretted Buying The Business

Month four was brutal. Two employees were frustrated. Cash was tighter than expected. A major customer complained, and a machine that had already caused problems failed again. At the end of another long day, the buyer sat alone in his car and thought something he had never expected to think. *"I may have made a mistake."* The thought scared him. He had spent years trying to buy a business. He had searched for deals, analyzed financials, negotiated with sellers, raised capital, and imagined what life would be like when he finally became an owner. Now he owned the business. And some days, he wanted a break from it. Nothing was technically failing. Revenue hadn't collapsed. Customers weren't leaving in large numbers. The company wasn't approaching bankruptcy. But everything felt heavier than it had in the model. That is the part of business ownership people rarely discuss. Acquisition regret doesn't always mean the buyer purchased a bad business. Sometimes it means the responsibility of ownership has finally become real. The buyer called another operator and explained what was happening. After listening, the operator told him something that changed his perspective. *"You're not evaluating the deal right now. You're reacting to the weight of ownership."* That conversation helped him recognize that he had been trying to solve every problem at once. So he stopped. He narrowed his focus to three priorities. Cash. Customers. Key employees. Everything else went onto a list to address later. The business didn't suddenly become easy. The problems didn't disappear overnight. But the buyer became more focused. By month six, cash flow had stabilized. Customer issues were being addressed more consistently. The team was beginning to settle into the new ownership. The regret faded. The lesson remained. Post-close, emotional volatility is real. Operators need financial models, operating plans, and systems. But they also need perspective. Not every difficult month means the acquisition thesis was wrong.

0

0

2d •

The Employee He Never Knew He Needed

Three weeks after closing, Chris received a text message that changed everything. One employee had resigned. At first, it didn't seem like a big deal. But over the following days, customer appointments were missed, invoices stopped going out, and employees kept asking the same question: "Did Maria handle that?" Chris soon realized he hadn't just lost an employee. He had lost the person holding the business together. A powerful lesson in key person risk, institutional knowledge, and why due diligence goes far beyond the financial statements.

0

0

4d •

🎉 Congratulations To Our New AON Students! 🇺🇸

First, I want to congratulate everyone who has already taken advantage of our 250th Anniversary Independence Day Sale and enrolled in one of our Acquisition Operator Network courses. You're not just buying a course. You're investing in a skill set that can compound for the rest of your career. Every great acquisition starts with a better operator, and every better operator starts with better decisions. That's exactly what these courses are designed to help you build. If you haven't enrolled yet, there's still time. ⏰ The sale runs through Midnight, July 4th (Eastern Time). After that, all courses return to their regular pricing. 🇺🇸 Anniversary Sale Pricing 📘 The Self-Paced Acquisition Blueprint Regular: $997 Now: $747 📗 The Operator Blueprint Regular: $2,500 Now: $1,875 📕 The Acquisition Accelerator Regular: $7,500 Now: $5,625 Whether you're evaluating your very first acquisition, actively negotiating deals, or preparing to become a stronger operator after closing, there's a course designed specifically for your current stage of the journey. 👉 Simply visit the Classroom tab inside AON and select the course that best matches where you are today. Don't wait for the "perfect" deal to start learning. The buyers who consistently find great opportunities are usually the ones who prepared long before those opportunities appeared. Congratulations again to everyone who has already joined one of the programs. I look forward to seeing your progress, hearing about your deals, and watching you grow into confident acquisition operators. The countdown is on. Midnight, July 4th (EST) is the deadline. Don't miss it! 🇺🇸

0

0

6d •

⏳ 48 Hours Left To Save 25% On Every AON Course 🇺🇸

Time is running out. Our 250th Anniversary Independence Day Sale ends in just 48 hours, and with it goes the 25% discount on every Acquisition Operator Network course. If you've been thinking about taking the next step in your acquisition journey, now is the time. 📚 Anniversary Pricing 🔹 The Self-Paced Acquisition Blueprint Regular: $997 Now: $747 🔹 The Operator Blueprint Regular: $2,500 Now: $1,875 🔹 The Acquisition Accelerator Regular: $7,500 Now: $5,625 Whether you're just learning how to evaluate your first business, actively pursuing acquisitions, or preparing to operate after closing, there's a course built specifically for your current stage. 👉 To enroll, simply visit the Classroom tab inside AON and select the course that best matches where you are in your acquisition journey. Remember... Knowledge compounds. Experience compounds. Ownership compounds. The sooner you begin building your acquisition skillset, the more opportunities you'll be prepared to recognize and execute. ⏰ The sale ends on July 4, 2026. After that, all courses return to their regular pricing. Don't let this opportunity pass you by. Visit the Classroom today and take the next step toward becoming an Acquisition Operator.

5d •

The Customer Who Almost Left

Shortly after closing, one of the company's largest customers called with concerns. Service had begun to slip, and while they still liked the business, they weren't sure how the ownership transition would affect the relationship going forward. The buyer had several options. He could have replied with a reassuring email or scheduled a quick phone call. Instead, he got in his car and drove two hours to meet the customer face to face. He spent most of the meeting listening. He didn't over-explain the situation. He didn't blame the previous owner, and he didn't make unrealistic promises about fixing everything overnight. Instead, he asked one simple question. "What matters most to you over the next 90 days?" The customer identified three priorities. Clear communication. Consistent delivery. One accountable point of contact. The buyer built the entire account plan around those three expectations. The customer stayed. Even better, six months later they expanded their business with the company. That experience changed how the buyer approached important customer relationships. He realized that showing up in person can completely change the emotional temperature of a difficult situation. Not every customer concern requires a discount. Sometimes it requires proof that the new owner cares enough to invest their time. One of the biggest post-close lessons was this: Customers aren't only evaluating the quality of your service. They're evaluating whether the new owner understands the value of the relationship. Sometimes, a visit communicates more than an email ever could.

1-30 of 92

powered by

Suggested communities

Powered by