Activity

Mon

Wed

Fri

Sun

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

What is this?

Less

More

Owned by Kevin

A simple path to automated futures trading. Try 45+ algos for 30 days.

Memberships

ACQ Scale Advisory

1k members • Free

Skoolers

181.4k members • Free

The 100

96 members • Free

Fit Skool

660 members • Free

Authentic Selling

38 members • Free

437 contributions to 5-Minute Futures

🚀

🔥

1d •

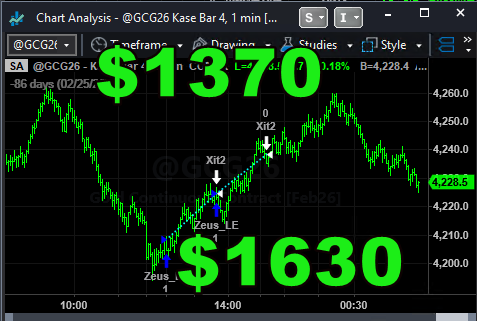

12/11/25 | Open PNL: +1.29% | Closed PNL: +1.76%

I cover what it looks like when 16+ algorithms are trading futures markets on autopilot in this quick video!

🚀

🔥

1 like • 1d

@Alec Feintuch sure thing, glad you liked it!

🚀

🔥

2 likes • 12d

Yes thank you Adam! GC was supposed to be rolled last week. I'll make a video covering this

🚀

🔥

1 like • 4d

@Mauricio Andrés Rivas Barriga I will do a big contract rollover update after 12/19/25 which includes Q4 quad witching. Nearly all charts symbols will be rolled, and included in the new Q1 2026 update

🚀

🔥

Jun 24 •

How to get VIP Tech Support👇

Need help? 1. Post a comment below 2. Use the search bar at the top P.S. For faster response times tag: @Kevin Gong

🚀

🔥

3 likes • 9d

Toolkit is working again! Make sure you're on: 1. The latest TS10 update 1443 as of 10/24/25 2. Display resolution of 1920x1080 in your VPS 3. Only work on 1 desktop with 1 workspace open at a time 4. Keep your VPS open and avoid minimizing while Toolkit runs @Adam King @Alec Feintuch @Steve Reich @James Borowiec @Scott Hemmings @Joey Wachter

🚀

🔥

1 like • 9d

@Steve Reich @Alec Feintuch lmk how it goes

🚀

🔥

9d •

Concierge Portfolio Review: 2025 November

Based on $300k starting capital: - Total Return: +2.13% - MaxDD: 8.76% - Win Rate: 37.2% - Total Trades: 121 - Average Win: $2.06K - Average Loss: $-1.13K - Expected Value: $-52.70

2

0

1-10 of 437

🚀

🔥

@kevingong

Connector of people in ACQSA | Founder @ skool.com/futures | I help investors diversify their $1M+ portfolios with futures trading algorithms

Active 27m ago

Joined Sep 22, 2024

INFP

skool.com/futures

Powered by