Write something

15d •

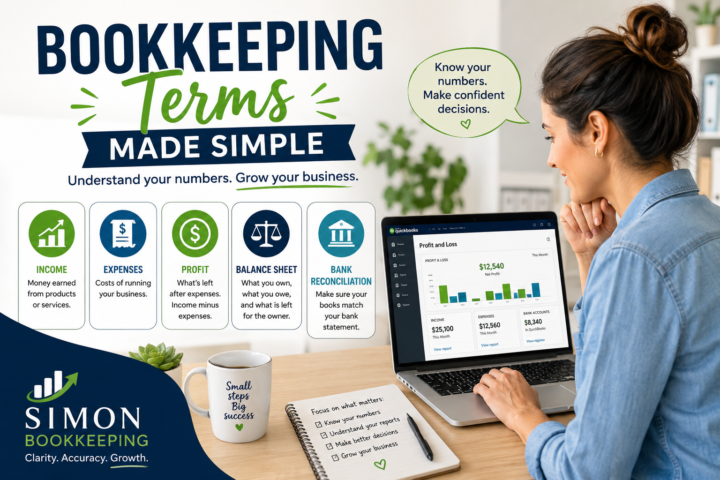

📚 RESOURCE - Basic Bookkeeping Terms for Small Business Owners

Basic Bookkeeping Terms Every Small Business Owner Should Know Bookkeeping does not have to feel complicated. These basic terms will help you understand what you are looking at when you open QuickBooks Online or review your business reports. Profit and Loss Report A Profit and Loss report shows how much money your business made and how much it spent during a certain period. It usually includes: - Income - Expenses - Profit or loss In simple words: Did your business make money or lose money? Income Income is the money your business earns from selling products or services. Examples: - Customer payments - Service fees - Product sales Expenses Expenses are the costs of running your business. Examples: - Rent - Supplies - Software - Advertising - Insurance - Professional services Profit Profit is what is left after your business pays its expenses. Simple formula: Income minus expenses = profit Loss A loss happens when your expenses are higher than your income. This does not always mean the business is failing, but it is something you should understand and review. Balance Sheet A Balance Sheet shows what your business owns, what it owes, and what is left for the owner. It includes: - Assets - Liabilities - Owner’s equity In simple words: What does the business have, what does it owe, and what is its overall financial position? Assets Assets are things your business owns or controls. Examples: - Bank account balance - Equipment - Vehicles - Inventory - Money customers owe you Liabilities Liabilities are what your business owes. Examples: - Loans - Credit card balances - Bills you have not paid yet - Sales tax owed Equity Equity is the owner’s share of the business after debts are considered. Simple formula: Assets minus liabilities = equity Accounts Receivable Accounts Receivable means money customers owe your business. Example: You sent an invoice, but the customer has not paid yet. Accounts Payable Accounts Payable means money your business owes to others.

2

0

17d •

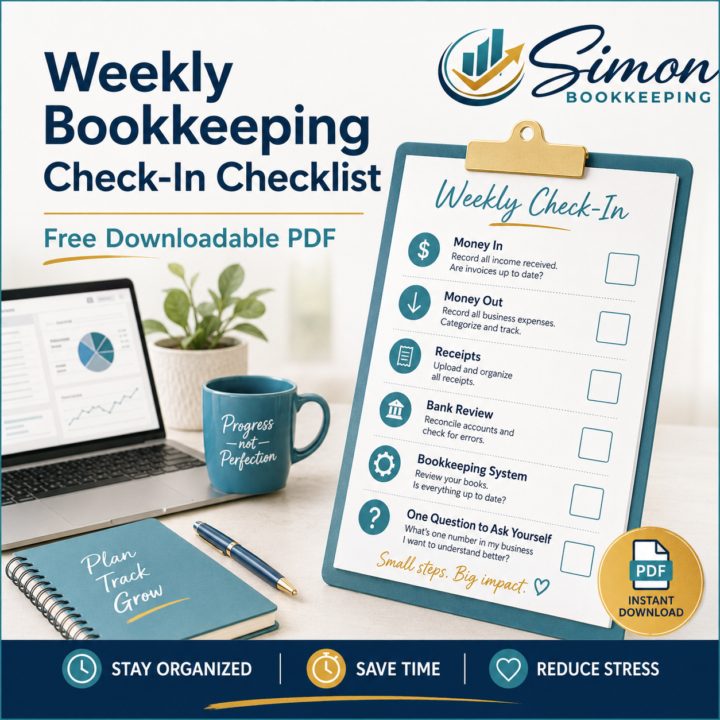

📚 RESOURCE - Free Weekly Bookkeeping Check-In Checklist

Get Your Weekly Bookkeeping Check-In Checklist https://forms.gle/FnwsXDBPXys3VB776

2

0

22d •

📚 RESOURCE - How AI Helps My Bookkeeping Process

I use AI to improve efficiency. Examples: ✔ Research ✔ Workflow support ✔ Content creation ✔ Administrative assistance But human review and judgment still matter. https://simonbookkeeping.com/about-us

2

0

22d •

📚 RESOURCE - Free Consultation

Thanks for being part of the community. If you'd like a second set of eyes on your bookkeeping: 📞 Schedule a free 30–45 minute consultation. We'll discuss: • Current bookkeeping process • Challenges • Opportunities for improvement No pressure. Just a conversation.

1

0

22d •

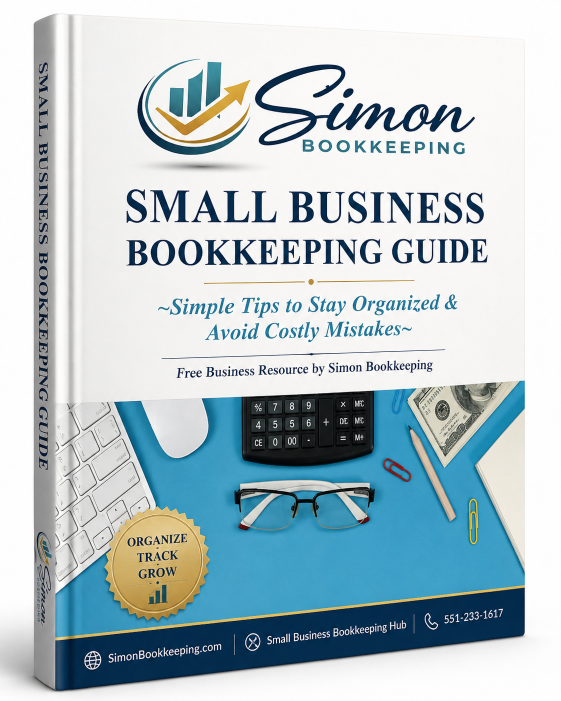

📚 RESOURCE - Free Bookkeeping Guide

Download: Small Business Bookkeeping Guide - Simple Tips to Stay Organized & Avoid Costly Mistakes Inside you'll learn: ✔ Basic bookkeeping habits ✔ Common mistakes to avoid ✔ How to stay organized year-round ✔ Tax-time preparation tips Get the Guide Here: https://forms.gle/9xrC7Ge3PfjhhwxFA

1-5 of 5

powered by

skool.com/small-business-bookkeeping-hub-9336

This free community is for small business owners, freelancers, and startups who want to better understand their bookkeeping and finances.

Suggested communities

Powered by