Write something

10h •

These are the FAQs I get about DSCR loans:

❓ If my purchase price is 50% of the value of the house, will the DSCR cover 100%? ▶️ Answer: No. DSCR lenders will take the lesser of the purchase price and value ❓ Can I get 80% LTV on a cash out refinance? ▶️ Yes, depends on the state ❓ Can I use an income approach on a single family or fourplex? ▶️ Answer: No. 1-4 unit properties are residential and appraised using a Sales Income Approach ❓ Can I refinance a manufactured home? ▶️ Yes! You can get up to 75% LTV with the right lenders, too. ❓ I don’t own anything, can I still get a loan? ▶️ Yes! These loans are perfect for new or seasoned investors. ❓ Can I remove the prepayment penalty period? ▶️ Yes, generally. Your interest rate or fees would slightly increase, as a result. ❓ Can you DSCR multifamily? ▶️ Yes! Residential and commercial properties can qualify. ❓ Do I need a 1.2 DSCR to get this loan? ▶️ NOPE! Most lenders will approve a 1.0 DSCR (some, even lower, but don’t buy a property that’s negatively cashflowing) ❓ What states do you not lend in? ▶️ North and South Dakota 😔 ❓ Can I get a DSCR to buy and renovate a property? ▶️ No, DSCR loans do not give you funds to rehab a property. Use a Hard Money Loan. What questions do you still have?

0

0

Jun 2 •

Wanting to scale and expecting everyone to bend to your terms aren't two things you get to have at the same time.

I had a call last month with an investor with an active deal flow and a good private money network. They got on the call because they already knew their private money lenders were tapped out — and they saw the value in what our lenders could do for them. But when the terms came up, everything changed. "The lender should change their process to show they want to work with me." That was almost verbatim what they said. But the more deals you do, the more you should understand how these processes work. It sounded like somewhere between their first deal and their tenth, “cheap” private money capital stopped being a tool and started being the only way they knew how to operate. PSA: Hard money and private money aren't competing. They're complimentary. But you don't get to build that stack on your own terms. That's not how collaboration works — and that's not how scaling works either. An unwillingness to work within a lender’s terms is the biggest problem I see with growing investors. That's the only thing standing between where they are and where they are trying to go.

0

0

May 11 •

**Don't Sign Until You Read This**

A lot of people think once they hand over their paperwork to a lender, their job is done. It's not. Closing a deal is teamwork. Your job doesn't stop at the documents. Here's what to watch for: 👉 Did the terms change from what you agreed to at the start? 👉 Does anything in the closing docs look different? 👉 Did anyone warn you about changes, or did they surprise you at the table? **Four steps to stay on top of it:** 1. 1️⃣ Make a Google Drive folder for your Chris Deal 2. 2️⃣ Save your term sheet 3. 3️⃣ Ask along the way: "Are the terms still the same?" 4. 4️⃣ Read your closing docs before you sign A borrower of mine signed for an adjustable rate loan WITHOUT KNOWING IT until they were sitting at the title company on closing day. We caught it and fixed it in time, but that's not always how it goes. Four steps, maybe 10 minutes total. And most investors skip all of them. Don't. be. that. investor.

0

0

Apr 28 •

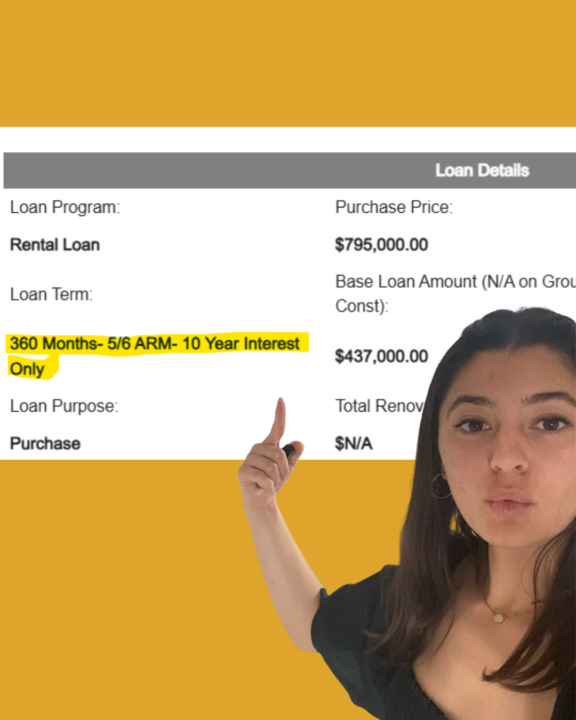

A price drop that doesn't sell your flip can also kill your refinance.

I had a borrower come to me last week with a flip that wouldn't move. $50K into rehab. Priced at $700K. Dropped it to $650K trying to get traction. Meanwhile, he's bleeding hard money fees every month with no exit in sight. He decided to refinance and keep the property as a rental to stop the bleeding. Most flippers assume refinancing is straightforward once the rehab is done — especially if the appraisal comes in strong. So they drop the price, wait for the right buyer, and plan to refi if it doesn't sell. ☝️ What they DON’T know is that price drop just became the number their lender has to work with. If your property is listed — or was listed in the last 6 months — a DSCR lender cannot use appraised value. They use the lowest list price on record. So his math changed fast. Property appraised at $700K. Loan at 75% LTV. He wanted $525K out. But the lender had to base the loan on that $650K price drop. His actual loan came in at $487,500. That's $37K less than he was counting on. The fix: don’t drop and delist before you apply. 👉 Most lenders need 6 months off market before they can ignore the list price history and go back to appraised value. Know this before you cut the price. If you're sitting on a flip that isn't moving and you're thinking about refinancing out, get off market first. THEN start the conversation with your lender. Timing this wrong is an expensive lesson. Hopefully this saves someone from learning it the hard way.

1

0

Apr 17 •

“I have a new bank account for my business – do I have to season my funds for 60 days?”

We’re working with an investor right now who asked this exact question. His situation: - He’s refinancing a property into a new LLC - The bank account for that new LLC was just created Most DSCR lenders want to see **2 months of bank statements** with funds in the account to verify liquidity. Most DSCR lenders want 2 months of statements with funds sitting in the account to verify liquidity — so he was worried he'd have to wait 60 days before he could close. The good news was he already had the funds. They were just spread across other accounts. Our lenders aren't going to reject someone because a brand-new LLC account doesn't have a long history. They want to see where the money actually lives. As long as he sends: - Bank statements from the accounts that actually hold the funds - Operating agreements for any accounts owned by an LLC he’s in the clear. If you're in a similar spot — new LLC, new account, working on a refi — before you panic about seasoning, get clear on: 1. Where does the money actually sit right now? 2. What entity owns those accounts? Once you know that, pull the statements and operating agreements. You're probably closer to a clean approval than you think. 😁

1

0

1-30 of 41

powered by

skool.com/real-estate-30-days-challenge-5427

Achieving financial freedom and building wealth are easy if you know where to start.

Our #1 goal is accelerating your growth with real estate!

Suggested communities

Powered by