Write something

3d •

Dispute

Can someone direct me what to do I accidentally disputed something on my report that wasn’t suppose to be disputed. Can I call and remove it ? Will my credit score drop? What the easiest way to have credit bureau update my information if am able to remove that dispute

9d •

Can they?!! 😬😬

I had a department store credit card through Comenity Bank for $100. That card was charged off and now it's in collection. I paid it off in Sept. 2025, but there was a residual balance of less than $20, possibly even $5-$8. I was not aware of that, because I assumed I paid it in full. After reviewing the trade line pages, I closed it in 10/2025 (listed as consumer closed), yet it didn't charge off until several months later. So here is the million dollar question, if the trade line page states that the limit was $100, how and why would the creditor let allow it to snowball to $362? That seems predatory & excessive!!! Also, I've had cancer residual issues over the past 2 years needing multiple surgeries and being out on FMLA, twice, so I wasn't cognizant of checking routinely. I am officially in clean up mode so I can get a newer car soon. Any tips? I haven't disputed anything yet, I'm cleaning up personal information at the moment, but this $362 issue is annoying me! Lastly, I can see myself doing this in the future, in helping others. Any newbie side hustlers in this realm? Tips? I think this is me liking the challenge and then add my active paralegal skill set, I strangely like the paper work documentation/organization. 😆 Thanks for reading!

May 6 •

New here Guys

Hey everyone! 👋 I’m Badmus from United States. I’m really excited to be part of this amazing community and connect with like-minded entrepreneurs! 😊 A little about me I run a successful Shopify dropshipping business that’s scaled to six figures, and I’m truly passionate about helping others explore the same path. Outside of business, I’m a huge luxury car enthusiast and love traveling to experience new cultures. Thanks to e-commerce, I’ve also been able to start investing in real estate and building a small luxury watch collection both things I used to only dream about. Looking forward to learning, sharing, and connecting with everyone here!

3

0

May 5 •

📜 The History of Credit Repair: From "Neighborhood Gossip" to Legal Rights

If you think credit repair is just about "deleting stuff," you’re missing the most important part. It’s actually about exercising your legal rights under laws that were created to stop corporations from ruining people's lives with bad data. Before the 1970s, the credit industry was like the Wild West and the consumer always lost...so here’s how we got to where we are today. 🏛️ The "Wild West" (Before 1970) Before the laws we use today existed, credit bureaus were private companies that kept "character files." They didn't just track your bills; they tracked you. - The "Lifestyle" Blacklist: Investigators would interview your neighbors or coworkers. If a neighbor told them you "seemed to party too much" or had "questionable morals," that subjective opinion became a permanent part of your file. You could be denied a house because of a neighbor's grudge. - The Permanent Scarlet Letter: There was no "7-year rule." A single missed payment in your 20s could stay on your record until you were 60. There was no such thing as a "clean slate." - The "Secret" File: You had no legal right to even see your own credit report. If a clerk mistyped your social security number and merged your file with a stranger's, you were stuck with their debts and had no way to prove the mistake. ⚖️ The Two Laws That Changed the Game • The FCRA (Fair Credit Reporting Act) – Born 1970 The FCRA was the first time the government told credit bureaus: "The consumer owns their reputation, not you." The Mission: Accuracy, Fairness, and Privacy. The Power: It mandates that if information is inaccurate, incomplete, or unverifiable, it must be removed. This created the "30-day investigation" rule we use for disputes today. The Result: It ended the era of "neighborhood gossip" and forced bureaus to use actual data. • The FDCPA (Fair Debt Collection Practices Act) – Born 1977 As credit became common, debt collectors became aggressive. They would call at 3:00 AM or threaten jail time.

Apr 29 •

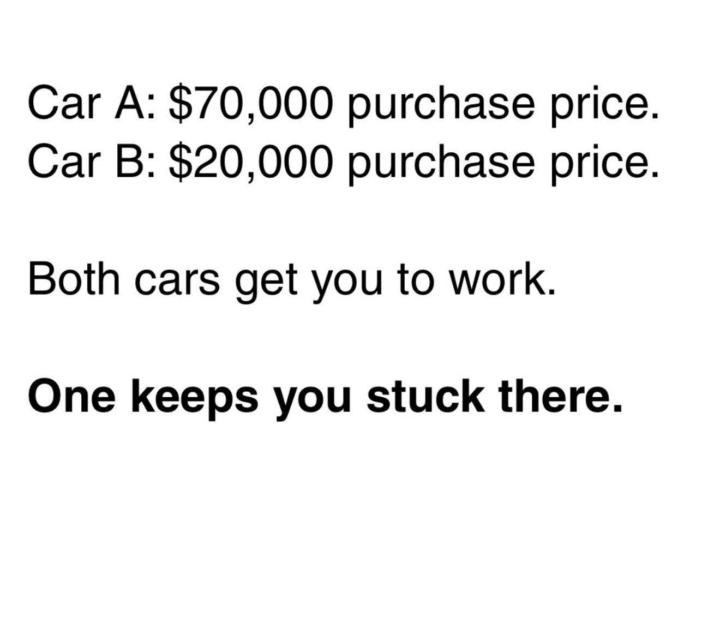

🛑 The "Credit Trap" vs. The Wealth Bridge

We talk about credit all the time in this community because, used correctly, credit is the ultimate leverage. It’s the fuel that can accelerate your journey to financial freedom. But here’s the reality… Leverage works both ways. When access to credit falls into the hands of those who haven't mastered their mindset, it becomes a cage. Car A might look better in the driveway, but Car B is the one that actually buys you your time back. If you use your credit for material things that depreciate the moment you drive them off the lot, you aren’t using leverage, you’re being leveraged by the bank. How to actually use your leverage: Instead of financing a lifestyle you haven't earned yet, use that credit to acquire assets and skills: • 🏠 Real Estate: Buy a property to rent out for monthly cash flow. • 🛠️ Fix & Flip: Use a line of credit to renovate a distressed property and pocket the profit. • 📦 Business Infrastructure: Purchase equipment for a service-based business that generates daily revenue. • 🧠 Self-Education: Invest in a high-level course or a coach. The ROI on a new skill often dwarfs any real estate deal. The goal isn't to look rich; it's to be wealthy. One car keeps you stuck at a 9-5 just to cover the monthly payment. The other gives you the margin to build an empire. What’s one "material" purchase you’ve passed on recently so you could reinvest that capital into your future instead? 👇

2

0

1-30 of 200

powered by

skool.com/level-up-your-life-8251

Stop paying thousands for credit repair. Learn the secret to doing it yourself.

Suggested communities

Powered by