Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

What is this?

Less

More

Memberships

FXminds - Trading - 🌍

145 members • Free

Volturon Trading Systems

222 members • Free

🥷 Trading FX | DMS Free

103 members • Free

Alpha Trading Academy

205 members • Free

GPG Forex Trading Community

99 members • Free

Day Trading For Beginners

483 members • Free

Shinobi Trading Dojo

11 members • Free

Belle Wealth Trading Circle

259 members • Free

Checklist Trading

158 members • Free

1 contribution to Options Jive

Jan 22 •

Converting a SPY Put Ratio Into a Risk-Free Butterfly 🦋 (Again)

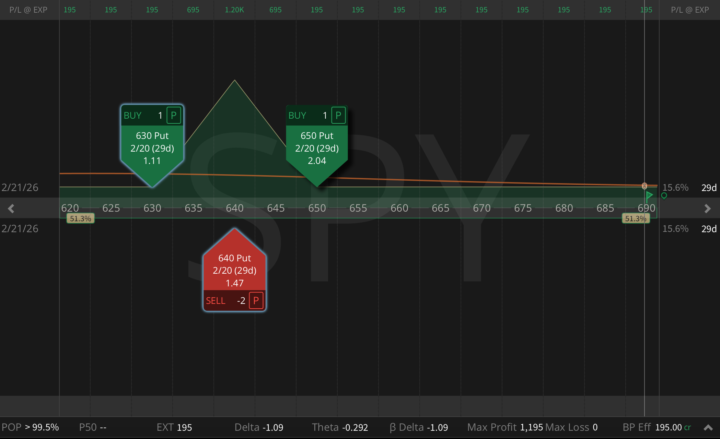

Tuesday was one of those sessions where headlines hit like market orders, and implied volatility reprices faster than most traders can think. The catalyst was political, but the effect was purely mechanical: demand for downside protection spiked, put skew steepened, and short-dated IV inflated as Trump escalated trade threats tied to his Greenland push. I opened a SPY 650/640 put ratio spread (1x2), 31 DTE, for a $306 credit. Why enter into a volatility spike? Because in these moments the options market often overpays you for two things at once: downside convexity (puts get bid aggressively) and crash insurance embedded in skew (OTM puts become disproportionately expensive). Then came the key adjustment. I just bought the 630 put for $1.11, and that single move converted the entire position into a risk-free butterfly. And once you complete a symmetric fly for a credit, the payoff becomes pure geometry: - Zero downside risk - Zero upside risk - Max profit: $1,200 (peaks near 640) - Min profit: $195 (everywhere else) - Probability of Profit (PoP): 100% This is the part most retail traders don't internalize: in high volatility, you're not predicting direction; you're engineering a distribution. When everyone's panicking, you can sometimes build free trades because the market overpays for convexity first, and then later hands you the wing cheap enough to lock the structure. I do this setup on SPY all the time, but you can structure it on any liquid ticker: QQQ, IWM, even single names with tight markets. The full playbook (when I complete the wing, and the management tree if price accelerates) is broken down step by step inside The Trading Plan

1 like • Jan 24

Was going through posts and this insight is a game changer for me that "a single move converted the entire position into a risk-free butterfly". It was an eye opener for me and i will use it coming week. Thanks.

1-1 of 1

Active 4h ago

Joined Dec 27, 2025