Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

What is this?

Less

More

Owned by Richard

Set up, protect, and optimize your 1099Anesthesia income:Taxes, entities, contracts, & rates. Find the leaks.Make the leap. Create your leverage.

Memberships

Clief Notes

40k members • Free

The Sauce. (Resource Hub)

21 members • Free

Claude Code Club

6.3k members • $9/month

Skoolflow

290 members • Free

Community Builders - Free

11.4k members • Free

AI Automation Society

415k members • Free

🏛️ Coaching Academy

3.8k members • Free

The Great AI Shift

3.4k members • Free

The Iron Forge Brotherhood

36.2k members • Free

40 contributions to 1099AnesthesiaAdvantage

13d •

DON’t miss! See you Thursday!

We’ve had some great conversations over the last couple of weeks. A few things have been brought to light. Some stories surprised us. Others confirmed what many of us have been experiencing all along. The best part? Providers sharing what they’ve learned so the next person doesn’t have to figure it out alone. I can’t wait to dive into some of these conversations on Thursday. If you’ve been curious about 1099 life, bring your questions and join us. See you there.#1099AnesthesiaAdvantage

0

0

May 27 •

Introduce Yourself

Every week brings new members. Let's make sure you're known. Drop a comment below with: - Your credential (CRNA or MD) - Your state - Your current setup (W-2, already 1099, considering the switch) - One thing you want to fix or figure out in the next 6 months That's it. We'll reply, point you to the right tools, and if there are other members in your state or situation we'll tag them so you're not navigating alone. This is the post that makes the community not feel like complete strangers!

1 like • 18d

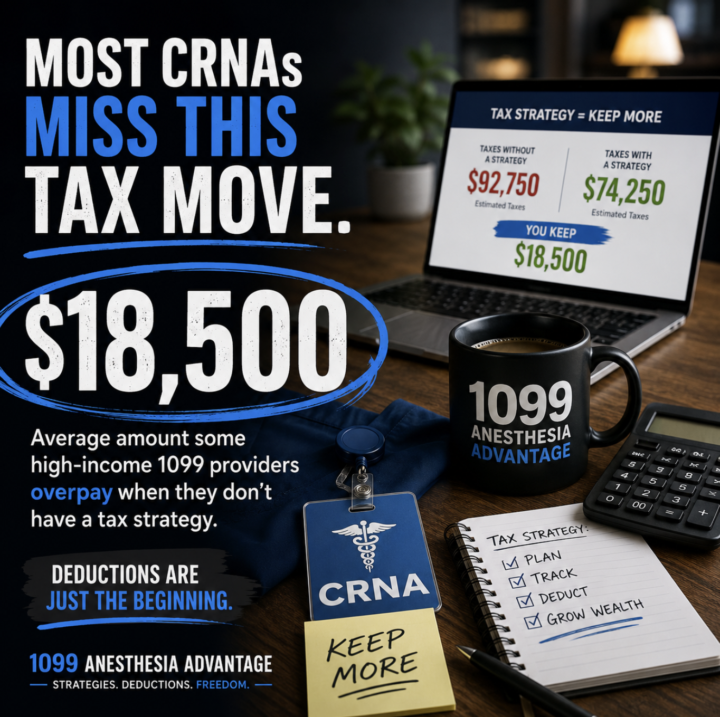

@Bryan Taylor Bryan thanks for sharing this. This is exactly the kind of story the community exists for. And the painful part is your CPA's framing is wrong. "1099 CRNAs don't have enough deductions" is the giveaway. Deductions are usually the smallest lever. The bigger fixes are structural. Three things that almost always matter more than chasing more deductions: 1. Entity structure. If you were taxed as a sole prop on your 1099 income, you paid 15.3% self-employment tax on every dollar of net profit. An S-Corp election splits that into reasonable W-2 wages (subject to FICA) and distributions (no FICA on distributions). For a CRNA at your income level, this single move usually saves more than every deduction combined. 2. Retirement structure. SEP IRA is fine, but Solo 401(k) is usually better for a 1099 CRNA. You can contribute as both employee and employer. Your W-2 403(b) is using up your employee deferral, but the employer-side contribution on your 1099 income (up to 25% of net SE income) stacks on top. Solo 401(k) also opens up Roth, profit sharing, and Mega Backdoor Roth in some plan designs. SEP can't do any of that. 3. State planning. That $7K Missouri pass-through caught my eye. Missouri has a PTE election where the entity pays the state tax and the entity deducts it federally, working around the $10K SALT cap. If your CPA didn't make that election, you paid $7K to Missouri that didn't reduce your federal tax bill the way it should have. May be amendable, definitely fixable for 2026. Two other things worth asking your CPA about. Augusta Rule, section 280A(g), where you rent your personal residence to your S-Corp for up to 14 days a year for legitimate business use. Tax-free income to you, deductible to the entity, usually $5K to $15K a year for a CRNA. And an Accountable Plan, where your S-Corp reimburses you tax-free for home office, mileage, phone, CE, equipment, professional dues. Not a deduction. A reimbursement. Cleaner and much harder to challenge.

0 likes • 18d

OK that simplifies the diagnosis. The S-Corp is in place, so the leak is somewhere downstream of the entity decision. With an S-Corp plus MFJ plus W-2 spouse, the most common gaps I see are: 1. The salary/distribution split. What's your reasonable W-2 salary from the S-Corp versus what gets paid out as distributions? This is the FICA optimization lever. Too high and you're paying FICA you don't need to. Too low and the IRS challenges it, AND your retirement contribution capacity drops because the Solo 401(k) employer-side contribution is capped at 25% of your S-Corp W-2 wages. There's a sweet spot, and most CRNAs miss it in one direction or the other. 2. Accountable Plan. Does your S-Corp reimburse you tax-free for home office, mileage, phone, internet, CE, professional dues, equipment, software? If you're paying those personally without a written Accountable Plan in place, you're missing reimbursements that should be flowing out of S-Corp profit, not your after-tax wallet. 3. Section 199A QBI deduction. CRNAs are usually classified as SSTB (Specified Service Trade or Business). The deduction phases out for MFJ filers in the upper $300K range, roughly $383K to $483K of taxable income depending on the tax year (adjusted for inflation). If your taxable income is under that threshold, you should be getting a 20% deduction on your S-Corp pass-through income. Worth confirming that's actually on your return. 4. Missouri PTE election. Same flag as before. If your CPA didn't elect this for 2024 or 2025, the $7K Missouri tax didn't get the federal deduction it should have via the SALT cap workaround. Possibly amendable depending on the year. 5. Retirement, correction to my earlier note. Since you're S-Corp, the employer-side Solo 401(k) contribution is 25% of your S-Corp W-2 wages, not net SE income. So your salary level directly caps the employer contribution. If your PRN W-2 403(b) is using up your employee deferral, the value of opening a Solo 401(k) is the employer match on top of your S-Corp wages.

20d •

Question of the Day

You can only ask ONE question before signing your next 1099 contract. What are you asking? Drop it below. The best question gets broken down and answered in this week's live Q&A. Let's crowdsource the questions everyone is thinking but nobody is asking.

22d •

The Cost of “I’ll Figure It Out Later”

A lot of CRNAs spend years planning patient care. We prepare for emergencies. We think through complications. We always have a backup plan. But when it comes to our own finances? Many of us say: “I’ll figure it out later.” Later turns into years. Years turn into missed opportunities. Retirement accounts never get opened. Tax strategies never get implemented. Contracts never get negotiated. And suddenly you’ve worked thousands of hours without maximizing the opportunities that were available all along. This isn’t about being perfect. It’s about taking one step today instead of waiting for the perfect time. What’s one financial move you wish you had made sooner in your career? 👇 I’d love to hear it. #CRNA #NurseAnesthetist #CRNALife #LocumCRNA #1099CRNA #FinancialFreedom #HealthcareProfessionals #AnesthesiaLife #CareerGrowth

29d •

True or False

A CRNA making $300,000 can legally pay thousands less in taxes than another CRNA making the exact same income. Same profession. Same income. Different strategy. Most providers never learn the difference. What's the biggest tax mistake you've seen someone make? 👇

0

0

1-10 of 40