Activity

Mon

Wed

Fri

Sun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

What is this?

Less

More

Memberships

Sacred Wealth Systems-Fundops

123 members • Free

Credit 2 Wealth Academy (FREE)

498 members • Free

13 contributions to Sacred Wealth Systems-Fundops

Apr 6 •

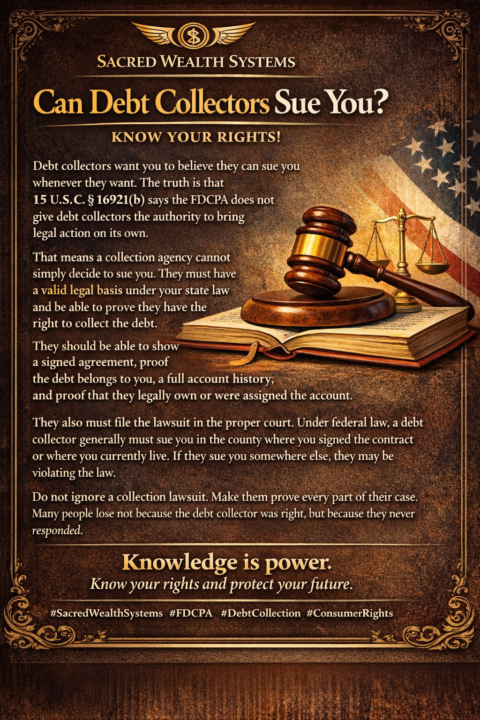

Title 15 1691i (b)

Debt collectors want you to believe they can sue you whenever they want. The truth is that 15 U.S.C. § 1692i(b) says the FDCPA does not give debt collectors the authority to bring legal action on its own. That means a collection agency cannot simply decide to sue you. They must have a valid legal basis under your state law and be able to prove they have the right to collect the debt. They should be able to show a signed agreement, proof the debt belongs to you, a full account history, and proof that they legally own or were assigned the account. They also must file the lawsuit in the proper court. Under federal law, a debt collector generally must sue you in the county where you signed the contract or where you currently live. If they sue you somewhere else, they may be violating the law. Do not ignore a collection lawsuit. Make them prove every part of their case. Many people lose not because the debt collector was right, but because they never responded. Knowledge is power. Know your rights and protect your future. #SacredWealthSystems #FDCPA #DebtCollection #ConsumerRights

5 likes • Apr 6

That’s solid knowledge!!

Mar 31 •

Fundops Clients

Check the master credit stacking Google Drive. New sub folder = 0% Cards. We are currently deep in research gathering ALL states 0% credit cards as a reference guide !!

3 likes • Mar 31

Much appreciated

Mar 6 •

Friday Personal Credit Stacking Play 🚨

Friday Funding Play 💳 Sacred Wealth Family… tap in for this week’s Friday Funding Play. A lot of people think every credit card application works the same way. You apply, the bank slaps a hard inquiry on your credit, and then you sit there hoping the approval comes through. But the reality is the system isn’t always that straightforward. Right now there are a few issuers where we’re consistently seeing a different type of workflow. Instead of hard pull first, decision later… the process is showing up as soft pull → approval → accept. In plain English, that means you can sometimes see whether you’re approved — and even see the limit — before you actually commit to the account. If you’re strategic about how you move, that changes the game. Let’s walk through the main cards where we’re seeing this behavior. First up is the Apple Card. Apple runs their credit card through Goldman Sachs and they typically check TransUnion. What makes this one interesting is the approval process. You submit the application and Apple will show you whether you’re approved and exactly what your credit limit and APR will be before you accept the card. At that stage the check is a soft pull, so you’re not committing to anything yet. If you decide to accept the offer, that’s when the account moves forward. Next is Citizens Bank, including some of their Private Client and Private Bank cards. Citizens typically pulls Experian and they have a pre-qualification tool that runs through a soft inquiry. That tool allows you to see if you’re likely to be approved before you move into a full application. This bank is more regionally concentrated, mainly operating across states like Massachusetts, New York, Pennsylvania, New Jersey, Florida, Michigan, and a handful of others along the East Coast and Midwest. Then you have BMO — Bank of Montreal — which has been expanding heavily across the U.S. market. BMO often checks TransUnion, and what we’re seeing is soft-pull pre-approvals showing up frequently, especially if you already have a relationship with them as a banking customer. When the system recognizes an existing relationship, approvals can sometimes be shown up front before the final acceptance happens.

4 likes • Mar 6

Great information timo🔥

Feb 26 •

Planning promotes progress for perseverance.

Timo and Egypt set me up to meet with two banks today. I went in and came out with $46K. Second Banker (US BANK) said the third approval was low because of the recent hard inquiries. So, he suggested that I wait a little while before the fourth application. Timo's relationship managers took care of me, and now I am creeping closer to my funding goal. #booya!

7 likes • Feb 27

🔥🔥🔥🔥

Feb 25 •

⏰Capital One Closing Down Credit Cards ⏰

People are opening their banking apps and finding every Capital One card gone no email, no missed payments, no heads-up. Tens of thousands in available credit wiped out overnight. Here’s why it’s happening 👇🏽 1️⃣ Credit Cycling Running a balance up and down multiple times in the same billing cycle looks like you’re spending more than you were approved for.Even if you pay fast and avoid interest, banks see this as risk. Fraud systems get involved. Accounts get reviewed and sometimes closed. 2️⃣ New Negative Info Anywhere Capital One regularly rechecks your entire credit profile.A late payment, collection, or charge-off with another lender can trigger action on your Capital One cards. This is called universal default if one lender sees trouble, all assume risk. 3️⃣ Returned Payments 🚨 This is the fastest way to lose accounts.A bounced or returned payment signals liquidity stress, even if you fix it immediately. Capital One often responds by reviewing or closing all cards, not just one. A clean on-time payment is better than an early payment that bounces. 4️⃣ Inactivity Leaving a card unused for too long can get it closed.Banks won’t keep open risk they’re not earning from. When old cards close, utilization jumps and scores often dip. 🧠 Sacred Takeaway Banks don’t reward effort they reward predictability and clean signals. If you’re building leverage and funding power, you must play the game strategically, not emotionally. Rewire. Reclaim. Receive.

3 likes • Feb 26

Solid..

1-10 of 13

Active 6m ago

Joined Feb 1, 2026

Powered by