Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Memberships

HRC Credit Mentorship

741 members • $129/month

6 contributions to HRC Credit Mentorship

3d •

Looking for Tips on Doing Inquiry Sweeps

I know some of y’all in here have done inquiry sweeps b4. I’m tryna learn the process myself. If anybody’s willing to share how u did it or got any tips, lmk. Appreciate it.

7d •

Kickoff play

Yoo that navy pledge loan play work for kickoff where you pay like 90% and let the rest report?

1 like • 7d

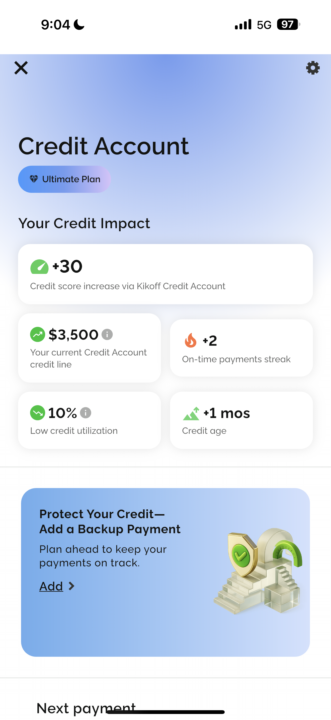

It isn’t exactly the same. The Navy pledge loan works because it’s an installment loan showing 90%+ paid while staying open. Kikoff’s $3,500 account is a revolving tradeline, so the goal is just to keep utilization low (around 10% or less). If you’re talking about the Kikoff builder loan, then leaving a small balance until the end can work, but Kikoff already reports it in a pretty optimized way

7d •

Question About the “Have I Been Pwned” Play

I’ve been seeing the “Have I Been Pwned” play all over recently. What’s your take on it? Can you explain what you think about it and whether you believe it’s actually useful or just another trend?

8d •

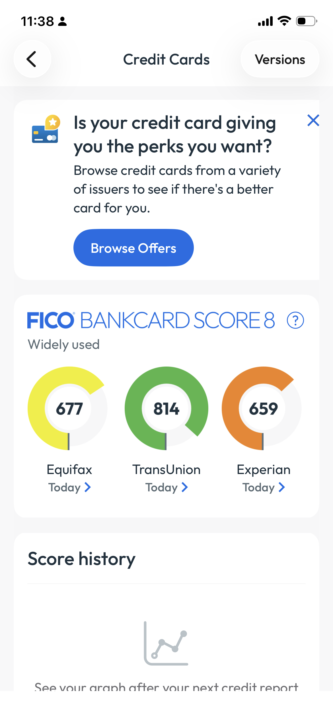

Yo my Fico 8 score on TU is 800🚀

Idek how I didn’t get approved with NFCU even with that 260 internal score. What else bank pull from TU. I need new credit card⁉️

1 like • 8d

NFCU doesn’t approve based on the internal score alone. They also look at things like recent inquiries, utilization, income, existing relationship, and anything negative on your credit report. A 260 internal score isn’t a guarantee of approval. Before applying anywhere else, I’d review the denial letter to see exactly why NFCU declined you. That can help you avoid another hard inquiry if the same issue would cause another denial.

1 like • 8d

@Deangelo Holmes That’s a play I been wit NFCU for like 6 years now that internal matters a lot wit them. I haven’t tapped into the business side yet, I can’t even speak on it.

🚀

9d •

the credit builder loan that builds installment history from scratch wit money u get back at the end 💎

wassgood fam. droppin a real one for u today 🔋 most yall got a couple cards n u grindin ur utilization but ur file still feel stuck. heres why. u only got ONE type of credit on there. all revolvin. no installment. n that caps how high u can climb. heres the deal. ur score looks at ur credit MIX. thats havin different KINDS of credit. revolvin (cards) n installment (loans). its bout 10% of ur score. a file thats all cards n no loan is missin a whole lane. u could have perfect cards n still leave points on the table just cause u aint got no installment tradeline. now most yall thinkin i dont wanna take out no loan n owe nobody. u dont gotta. theres a move built exactly for this. a credit builder loan. heres how it work. the bank dont hand u the money up front like a regular loan. they lock it in a savings account in ur name. u make a small monthly payment. like $25 a month. n every payment they report to all 3 bureaus as a installment loan. equifax. experian. transunion. so u buildin payment history AND addin a installment tradeline at the same time. then at the end of the term u get ALL that money back. it was ur savings the whole time. so u aint really borrowin. u savin money n buildin credit at the same time. thats why this move so clean for a thin file. the play step by step. first. pick one that reports to all 3 bureaus. some only hit 1 n that aint worth it. ask before u sign. second. keep the payment small. $25ish a month is plenty. u aint tryna strain urself. third. set it to autopay. a late on this hurt u the SAME as a late on a card. so u never wanna miss one. keep it perfect. fourth. let it ride the full term. dont close it early. u want that clean finished installment history sittin on ur file. at the end u get ur cash back. big catch u gotta know. read the fees before u pick one. some charge a lil admin fee up front. n u only need ONE of these. dont go openin 3. one installment tradeline reportin clean does the job. real talk. this the missin piece for a lotta yall. u been grindin cards n wonderin why u stuck in the 600s. u aint got no installment history on ur file at all. one credit builder loan fix that n hand ur money right back at the end.

2 likes • 9d

@Jacob PerezIt depends on what you’re trying to accomplish. Kikoff reports up to a $3,500 revolving trade line, while Credit Strong can report up to a $10,000 trade line, depending on the plan you choose. A pledge loan is also an installment loan, which helps diversify your credit mix and can help you build a relationship with the bank or credit union that issued it.

1 like • 8d

@Richard Jones You welcome fam

1-6 of 6

@jamare-brown-1570

Here to learn, network, and take action. Building strong personal and business credit, growing my LLC, and mastering funding.

Active 13h ago

Joined Jun 25, 2026

Powered by