Activity

Mon

Wed

Fri

Sun

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

What is this?

Less

More

Memberships

Swing Trading Desk

27 members • $59/month

Amazon FBA | Start & Grow

1k members • Free

The Cyber Range

1.6k members • $129/m

Cloud Residents · US Credit

750 members • Free

10 contributions to Cloud Residents · US Credit

2d •

Experian Credit Score With Your ITIN (via Nav)

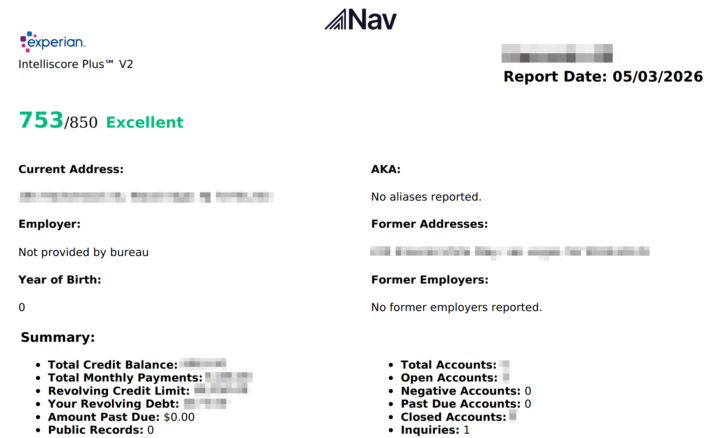

Most ITIN holders assume they can't see their Experian credit file online without a Social Security Number. You can. Sometimes. Shoutout to @momo for surfacing this method here first. Here's the updated standalone guide. Go to Nav.com, sign up for the free plan. You'll enter your name, DOB, address, and ITIN. Nav runs an Experian soft pull for identity verification and you're in immediately. If not, you can always retry. Once you're in, here's what Nav shows you: - VantageScore 3.0 from Experian - Score Factors - Payment History - Debt Usage - Credit Age - Account Mix - Debt vs Income - Hard Inquiries count - Current Address - Former Addresses Debt Usage drill-down: revolving credit limit, usage percentage, total revolving debt. Account Mix drill-down: split into mortgage, auto, revolving, and other accounts. Inquiries drill-down: total inquiries vs how many actually impact your score. Summary page: date of your first credit account, total balance across all accounts, total minimum monthly payments. Downloadable full report in PDF. This is genuinely useful if you're building US credit remotely and want to see where Experian has you — especially before applying for new cards. Now the caveats, because this matters. Nav's ITIN access for Experian is hit or miss. Some get through on the first try. Others don't, no matter what. If Nav doesn't work for you, alternatives exist: - Experian credit report by mail - Experian through Equifax Complete Premier - Experian FICO 9 through the Bilt app One more thing: VantageScore is not FICO. Almost all lenders pull FICO models when you apply. Nav's VantageScore 3.0 is directionally accurate, but don't treat a 720 VantageScore as a guarantee you'll get approved. Use it to track trends, not to predict underwriting decisions. If you try Nav with your ITIN - drop a comment below.

Poll

25 members have voted

0 likes • 2h

Got it to work, but it says connecting

9d •

When is the corporate rates module gonna be available?

I'm on the premium membership and I see that Corporate Rates Module is still pending and I have some travel planned soon but my credit score is not great yet for those Amex Cards.

0 likes • 9d

It auto unlock after being in the group for 3 months

11d •

$800 you're losing on SoFi right now

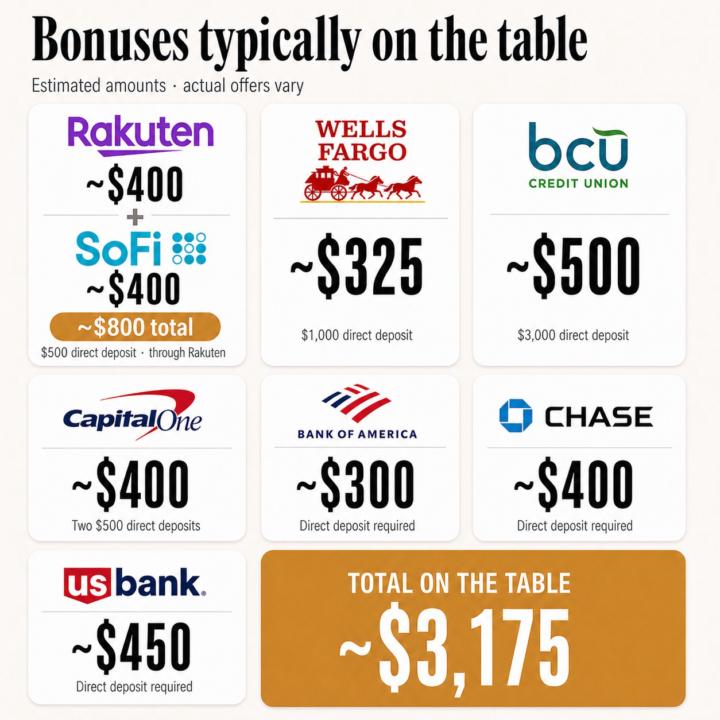

Direct deposit guide is finally live in the classroom Most US bank accounts run promotional bonuses for setting up a direct deposit. Add up the current ones across the major players: - Rakuten + SoFi stack ~$800 - BCU ~$500 - US Bank ~$450 - Chase ~$400 - Capital One ~$400 - Wells Fargo ~$325 - Bank of America ~$300 That's roughly $3,175 in cash sitting on the table right now. Some of these reset every 12–24 months, so this isn't a one-time grab - it's a yearly rhythm if you set it up right. For a lot of you, this is the easiest way to offset what you've already spent on your US setup - your ITIN, Virtual address, Phone number and your LLC, registered agent, business bank, all the small fees. One or two bonuses cover those costs. A full pass through the list pays it back several times over. _______________________________ A quick lesson before you open anything Don't rush to open a SoFi or any other account just because someone mentioned a bonus. The bonus offer needs to actually be live at the time you sign up, and the terms need to fit your situation. Before you open any account: - Confirm the bank is currently running a sign-up bonus - Check the direct deposit threshold and timeframe - Make sure your strategy can hit the requirement If there's no live bonus, you're just opening an account for nothing. The whole point is to get paid to open it. _______________________________ Why most fail to claim these The deposit has to arrive at the receiving bank with the right SEC code - specifically PPD (the code used for real Direct Deposits). Anything else - wires, push transfers from Wise, ACH credits from your business bank - usually arrives as CCD or some other code, and the bonus silently doesn't trigger. The two ways to send a direct deposit _______________________________ 1. Fake direct deposit (free, hit-or-miss) If you already have a Wise Business, Mercury, Relay or any other Business account, you can send money to your personal account with a memo like "payroll" or "contractor pay."

Poll

10 members have voted

0 likes • 11d

None that I can apply atm, still cooking my itin 🙂↕️

Feb 28 •

DCU Application Approved

It took me almost a week for this approval. It is one of the easiest Credit Union with approval time of as low as 3 hours but I got messed up with their application form ( date field ). Anyway it got approved after following them for 2 days. Documents required: - ITIN - Address proof - ID Verification You can opt-out debit card too as its not required. Tomorrow I will post about other Credit Union which got approved ( it is not easy for new ITIN but I managed to do it )

0 likes • 13d

@Apple Service you have the amazon secured card right? How many statements would you wait before applying for navy feds?

21d •

Amex Wants AI to Spend for You

Amex just signaled where payments may be heading next. They are building what they call agentic commerce, a system where AI can search, compare, and prepare purchases on your behalf using your card. Right now, the final approval still stays with the user. But the bigger story is not the approval button. It is the shift in decision-making before that step. Instead of you reviewing all the options yourself, the AI does the searching, filtering, and narrowing first. You only see the answer it decides to show you. That may sound convenient. But convenience and control are not the same thing. If the AI picks a flight, hotel, service, or product for you, you may never see: • the cheaper option it skipped • the extra fee buried in the details • the tradeoff it made without your input • whether it was optimized for your interests or someone else’s That last part matters. If these systems grow inside major card networks and platforms, members should be asking a basic question: Is the AI finding the best option for me, or the best option for the ecosystem behind it? I think this is worth paying attention to early. A lot of people here are trying to build stronger spending discipline, manage US cards carefully, and stay intentional with fees, utilization, and rewards. That gets harder when another layer starts making shopping decisions before you even review them. Today it is: “Here is the option I found, approve it.” Tomorrow it could become: • auto-approve anything below a set amount • auto-rebook travel • auto-reorder routine purchases And once spending becomes more frictionless, it usually becomes easier to overspend too. I am not against AI tools. But when it comes to money, I think AI should stay a tool, not become the decision-maker. For now, I would want full visibility, full approval control, and a clear way to audit why it picked what it picked. What about you? Would you trust AI to choose what gets charged to your card? See you in comments, Ain - Cloud Resident

Poll

25 members have voted

0 likes • 21d

Geez this is to get more of your money

1-10 of 10