Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

What is this?

Less

More

Memberships

LetsGetFunded PRO

689 members • $63/m

LetsGetFunded Inner Circle

1.7k members • $97/month

LetsGetFunded Starter (Free)

18.2k members • Free

46 contributions to LetsGetFunded Starter (Free)

1d •

What is Your Industry Code?

Do you know what industry code Dun & Bradstreet or Experian Business has for your business? Business bureaus, banks, & other lenders will have on file a business code linked to your business. If you didn’t provide the information, they could have an incorrect high-risk code associated with your business. Every industry has an identification code. All plumbers have the same code. All hair salons will have the same code. The U.S. Government tracks Gross Domestic Product Revenue (GDP) using these codes and it makes it easier to identify the primary activity of the business on tax forms. The two main codes used are the SIC Code and NAICS Code. Standard Industrial Classification code and the North American Industry System Classification code. Lenders, banks, insurance companies and business credit reporting agencies use the two business classification systems to determine if your business is a high-risk industry classification. This means that you could get a denial for a loan or a business credit card. And it could be based solely on your business classification. Some codes trigger automatic turndowns, higher premiums, and reduced credit limits. The choice of Industry code is yours. There is nothing wrong with choosing the SIC code which will not get you automatically denied by lenders. My Favorite SIC/NAICS Codes: SIC code 8741/NAICS code 541611, Management Services SIC Code 8742/NAICS code 561110, Management Consulting Services SIC Code 8748/NAICS code 541618, Business Consulting Services. Remember when speaking with lenders or providing your code to the business bureaus, instead of actively being in your industry, you can use codes that indicate you are a consultant in that industry. Example: Instead of being a real estate investor (which is a high-risk industry), be a business consultant to real estate investors. SIC Code 8748/NAICS code 541618. Or provide management services to real estate investors SIC Code 8741/NAICS code 541611. If using a real estate business code, use SIC Code 6531/NAICS code 531311 Residential Property Management. A lower risk code.

3

0

6d •

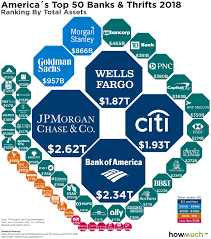

Have a Relationship With Banks You Are Targeting for Credit Lines

It pays to have a relationship with banks you are targeting for credit lines. Many banks and other financial institutions utilize “internal credit scores” in addition to the traditional credit scores from credit bureaus (like FICO or VantageScore) to evaluate the creditworthiness of their current clients. Comprehensive view: While credit bureau scores provide a general assessment of credit risk, banks can gain a more holistic and in-depth understanding of a client's financial health by incorporating their own internal data and insights. Behavior scores: Internal scoring models, sometimes called "behavior scores," leverage the bank's own data on a client's banking behavior, transaction history, loan repayment patterns within that institution, and more. Benefits for existing clients: These internal scores can be particularly valuable for managing existing accounts, determining credit limit increases, and offering relevant financial products (like mortgages, credit lines, or auto loans) to current customers based on their demonstrated financial behavior with that specific institution. Faster and more personalized decisions: By using internal data, banks can potentially make more timely and tailored lending decisions, especially when combined with alternative data sources and machine learning techniques. In essence, while traditional credit scores provide a general guideline, banks utilize internal credit scores to refine their risk assessments and offer more targeted financial solutions to their existing client base. If you have a personal checking account, a business checking account, savings account, or personal credit card in good standing with your targeted bank before applying you will probably get higher credit line offers. If you can, open business checking accounts, make consistent deposits for 3-months before applying for business credit products. Tip: Don’t apply online. Go to a local branch and meet with a Business Relationship Manager (BRM). Form a relationship. You usually receive higher credit lines with your BRM than online. This also takes your from being a customer of the bank to a client of the bank.

7d •

Do you want to pocket $8,000 to $14,000 (or more) tax free from your business income?

Lower your businesses tax burden while personally pocketing cash without paying taxes on it. Too good to be true you say? Learn about IRS Tax Code 280-A. Section 280A of the Internal Revenue Code allows for specific deductions related to the business use of one's home. It also states that renting out your home for 14 days or less in a year doesn't result in taxable income. Did you know you can rent out your residence for 14 days or less to your business entity and not have to pay tax on the income? Hold monthly meetings of your board of directors of your corporation or LLC. Keep notes for corporate compliance and benefit financially too. Learn more here: https://andersonadvisors.com/blog/section-280a-deduction-explained/

12d •

Business Line of Credit versus Business Credit Cards

I speak to many business owners and most everyone wants a traditional business line of credit. They prefer a BLOC over a BCC. I’d like to point out an advantage credit cards have over traditional lines of credit. Business credit cards are easier to obtain. They often come with 0% interest rates from 6-18 months. And they provide points or cash back which doesn’t exist with a traditional line of credit. A traditional line of credit will NEVER be at 0%. You need good revenue stream for a business line of credit. You don’t need revenue to get a business credit card. Business credit cards don’t show up on your personal credit reports. They don’t report credit utilization. A credit card offering points is often a great choice for those that travel frequently or want to. Many of these branded cards allow you to enjoy luxury experiences at a discount. They are great for those that want to benefit from “higher tiers” of rewards with more usage. A credit card offering cash back is often a great choice if you don’t travel a lot, you like simplicity, and you want an easy effort way to lower your cost of doing business (ROI). After all, you are spending money on business items and expenses you pay for anyway. Cash back credit cards allow you to lower the cost of doing business. Both credit cards and traditional lines of credit are examples of unsecured lines of credit. Meaning no collateral is needed. You can obtain larger traditional lines of credit if you have good revenue and collateral but you don’t need to go that route. I prefer unsecured credit lines. Points and cash back business credit cards are a great advantage over traditional lines of credit. And there are techniques you can implement to keep your 0% rate for an extended period of time. Which product is right for your business?

2 likes • 12d

No. A BLOC is a business line of credit. A lender gives you access to a certain amount and you can use some of it or all of it. You make payments and charged interest on only amount of the credit line you use. A loan is a specific amount given to you all at once and you immediately start paying interest and equal monthly payments over the term of the loan.

0 likes • 8d

@Jessica Frueh No online business or looking for one. I am currently a Funding Manager at Let's Get Funded.

8d •

Keep Increasing Your Credit Lines

If you are not using your credit lines, there is no reason for vendors or lenders to increase your credit lines. For all business owners. If you are using the credit lines you have and are paying them on-time, be sure to continuously ask for credit line increases. This is how you go from $5,000 to $10,000 to $25,000 or higher. Lenders love people that use their credit AND make aggressive payments on those lines. This goes for the business vendors you make frequent purchases from too. Every 6-months call and ask the vendor for a credit line increase. Do the same for all your personal and business credit cards too. Continue increasing your credit lines every chance you get. Get credit when you can, before you need it ASAP! Be ready for opportunity.

1-10 of 46

@dan-ollman-4226

20 Years Experience as a Business Credit and Funding Coach. Help business owners establish funding tied to their entity and EIN#, not your SSN.

Active 2h ago

Joined Nov 28, 2025

Powered by