Activity

Mon

Wed

Fri

Sun

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

What is this?

Less

More

Owned by Antoinette

This community helps people understand credit, read their reports, clean up errors, and learn a step-by-step dispute process.

Memberships

The Mogul Millionaire Map

19 members • $150/month

Royale Marketing Lab 🧪

357 members • $12/month

Skoolers

196.1k members • Free

Rose Credit Academy

827 members • $47/month

FI Wealth Academy

110 members • $100/year

Paid Ad Secrets

18.7k members • Free

Credit to Keys Lab

4k members • Free

Goins Consulting Group

108 members • Free

Credit2Capital Accelerator

117 members • Free

20 contributions to Elevate WithEva Credit Inner⭕️

24d •

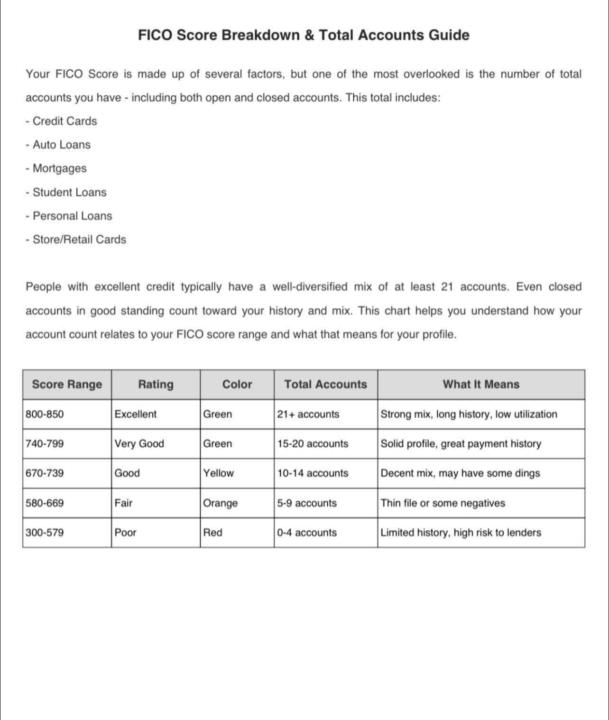

🔍 Understanding the Chart: FICO Score vs. Total Accounts

🔍 Understanding the Chart: FICO Score vs. Total Accounts Your FICO score is not just about paying bills on time, it’s also about how deep and diverse your credit history is. That’s where Total Accounts come in. This includes open and closed accounts like: • Credit cards • Auto loans • Mortgages • Student loans • Personal loans • Store cards The more well-managed accounts you have over time, the stronger your credit profile becomes. 📊 Breakdown by Score Range: 🟢 800–850 (Excellent) • 21+ accounts • You’ve built strong credit over time with a good mix (loans + cards), long history, low utilization. • You’ll qualify for the best rates, highest approvals, and most funding options. 🟢 740–799 (Very Good) • 15–20 accounts • Still in great shape! You may not have as long of a history or as many accounts, but you’re seen as low risk by lenders. 🟡 670–739 (Good) • 10–14 accounts • You’re on the right track. A few more accounts or better credit mix can push you to “Very Good.” • You may still qualify for good rates, but not always the best. 🟠 580–669 (Fair) • 5–9 accounts • Thin credit file or some negative items (like late payments or collections). • You’ll likely face higher interest rates or denials. 🔴 300–579 (Poor) • 0–4 accounts • Very limited credit history, recent negatives, or major derogatory marks. • You’ll need to rebuild your credit with secured cards, credit builder loans, and positive reporting accounts 💡 Why This Matters: • FICO likes to see both variety and responsibility. • You don’t need all your accounts open, even closed accounts in good standing help. • Don’t rush to open too many accounts at once. Focus on adding quality over time.

0 likes • 24d

Thank you

Mar 3 •

Retaining Clients

I have to figure out how to retain clients they get one round and see a little results but don’t follow through with the next round.

1-10 of 20

@antoinette-gupton-5755

My name is Nette. I look forward to learning more about leveraging credit the right way.

Active 21h ago

Joined Dec 13, 2025