Apr 20 •

Fomo

A lot of people want to get into the markets NOW. Now that we are at all time highs… That’s a common beginner mistake. They don’t want to invest until they feel fomo and realize we are all making money in these markets. You want to be in during the move - not after. That being said - it’s never too late to get in and catch the next one. Will be on live tomorrow. I will be putting more effort into growing the community and going live every Monday and Friday. Money Mondays will be onboarding, community basics, live Q&A. Finance Friday's will be actual learning and breakdowns. This Friday, we’re going over how to understand a price chart and the basics of technical analysis so you can actually recognize when you’re buying highs, lows, or dips.

Mar 24 •

Reasons to pick ETFs vs individual tickers

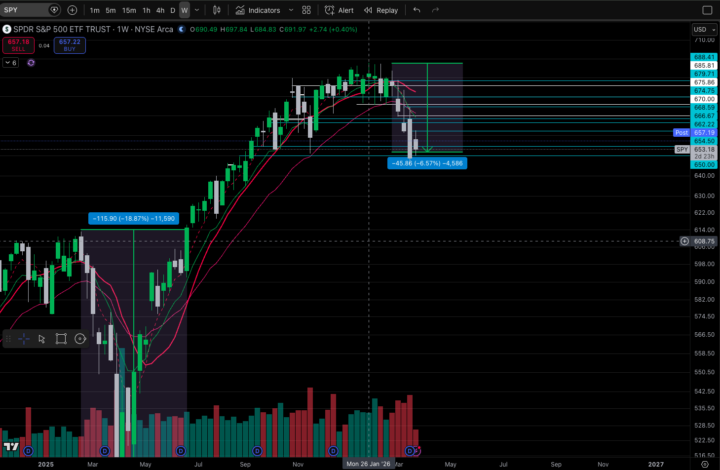

Take a look at these charts. SPY is down 7% from its high while big names like Microsoft, Netflix, and Nike are all down 20-30%. Do you want to see big swings of 30% in your portfolio? Nike stock is down real bad. Almost 70% from its highs! If you invested 10k would you rather be down $700 or $2500 in a market dip.. Thats the difference in picking an ETF vs an individual stock. Individual stocks can be more volatile and irrefutably have more risk. Now the reverse can also be true. You could've put 10k in NVDA and been up 2500. More risk = higher reward. This is why people like to pick individual stocks. But, When you buy individual stocks: • You’re taking on company-specific risk • You can experience massive drawdowns • You have to be right about that company So you have to pick your poison. For most people the takeaway is you don’t need to find the next big stock. KISS - Keep it simple stupid Just ETF AND CHILL

1

0

Mar 24 •

The 4% rule

An easier way to think about the 4% rule is this... First you need to determine what you can comfortably live off in retirement. If your comfortable # in retirement is $50k then you will need to figure out how much of that must come for your portfolio and multiply it by 25. Let me explain.. Example 1: No Other Income If you dont expect any other income sources and you will need to get the entire $50k from your portfolio then you simply multiply your comfortable retirement # number by 25. - 50,000 x 25 = $1,250,000 This means you should have a portfolio goal of 1.25 million to be able to withdraw 50k per year using the 4% rule. If you're expecting to receive additional income from another source (social security, pension, military etc.) then you will need to subtract that amount from your comfortable retirement number of 50k. Example 2: Additional Income Source If you expect $24k a year from social security that means you will only need $26k in income from your portfolio. 26,000 x 25 = 650,000. Your portfolio goal shrinks to only $650,000. These are just easy estimates. You may have less or more. But just a simple way to think about your retirement number and portfolio goals. If you want me to run your portfolio goal just comment the salary you want, if there is an additional income source (or not) and how much.

0

0

Mar 24 •

Member Portfolio build

Anyone who does not have their investment account set up and want to walk through buying their first stock on the next live? It will either be Monday or Friday. I want to encourage those who want to get started to get started ASAP and I think sometimes all it takes is someone taking you walking you through it step by step. You'll start with just $100.

0

0

1-13 of 13

powered by

skool.com/zero-to-investor-5955

Master the mindset and mechanics of investing. Built for beginners who want to start in the stock market with clarity and confidence.

Suggested communities

Powered by