Write something

11h •

🎓 Is Your Degree Setting You Up for Success — or Struggle?

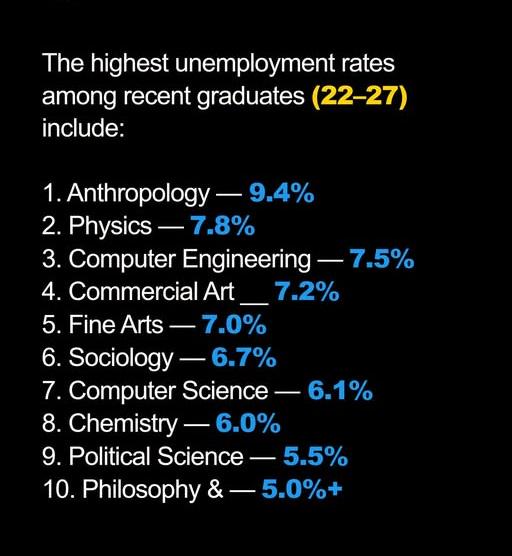

Every year, millions of students spend years of their lives and thousands of dollars on a college degree, believing it will open doors to a stable career. But the latest data from the Federal Reserve Bank of New York tells a sobering story — not all degrees are created equal when it comes to finding a job. The overall unemployment rate for recent college graduates hit 5.7% in early 2026, one of the highest levels in years. And for certain majors, the numbers are even more alarming. Here are the 10 degrees with the highest unemployment rates right now, and why. 𝟏. 𝐀𝐧𝐭𝐡𝐫𝐨𝐩𝐨𝐥𝐨𝐠𝐲 — 𝟗.𝟒% Fascinating field, but most career paths here require a Master's or PhD. A bachelor's degree alone leaves graduates with very few direct job options, and funding cuts in universities have made things even harder. 𝟐. 𝐏𝐡𝐲𝐬𝐢𝐜𝐬 — 𝟕.𝟖% One of the most demanding degrees out there, yet roles in research and academia are extremely limited and competitive. Without further education, it's hard to turn a physics degree into a stable private sector job. 𝟑. 𝐂𝐨𝐦𝐩𝐮𝐭𝐞𝐫 𝐄𝐧𝐠𝐢𝐧𝐞𝐞𝐫𝐢𝐧𝐠 — 𝟕.𝟓% Yes, even tech. A.I. tools are now doing what junior engineers used to do, and waves of tech layoffs since 2022 have flooded the market with experienced workers. Fresh graduates are left competing for very few entry-level spots. 𝟒. 𝐂𝐨𝐦𝐦𝐞𝐫𝐜𝐢𝐚𝐥 𝐀𝐫𝐭 & 𝐆𝐫𝐚𝐩𝐡𝐢𝐜 𝐃𝐞𝐬𝐢𝐠𝐧 — 𝟕.𝟐% A.I. image tools have disrupted this field faster than almost any other. Logo design, marketing visuals, social media content — things that once required a skilled designer can now be generated in seconds. Companies are cutting design teams as a result. 𝟓. 𝐅𝐢𝐧𝐞 𝐀𝐫𝐭𝐬 — 𝟕.𝟎% Most fine arts graduates rely on freelance work, commissions, and self-promotion to make a living. Stable full-time jobs are rare, and financial stability after graduation can take years to achieve. 𝟔. 𝐒𝐨𝐜𝐢𝐨𝐥𝐨𝐠𝐲 — 𝟔.𝟕% Sociology gives you a broad understanding of society, but that breadth works against graduates in the job market. Employers want specific, practical skills, and sociology alone often doesn't provide them.

1

0

1d •

Retirement numbers are starting to look absolutely ridiculous, and this is exactly why so many people feel like they are falling behind before they even get started.

A million dollars used to sound like the finish line, but for younger generations, that may barely cover a lean retirement once inflation, healthcare, housing, taxes, and longer life expectancy are factored in. That does not mean everyone needs to panic and assume they are doomed. It means people need to stop treating retirement like something they can figure out later. The math gets ugly when you wait too long. If you are in your 20s, 30s, or 40s, your biggest advantage is not picking the perfect stock, timing the market, or chasing the next investment trend. Your biggest advantage is time: • Time to invest consistently. • Time for compound growth to work. • Time to increase your income. • Time to avoid stupid debt. • Time to build assets before life gets even more expensive. The scary part is not that these numbers are big. The scary part is how many people are still saving like retirement will somehow magically work itself out. Retiring well is not about hoping Social Security, your employer, or the government figures it out for you. It is about taking ownership now, while you still have time to make the math work in your favour.

1

0

2d •

🚨 DON’T BUY A CAR JUST TO LOOK RICH

Here is why, step by step. 𝐒𝐭𝐞𝐩 𝟏: The moment you buy a car, it stops being just a car. It becomes a monthly bill. A fuel bill. An insurance bill. A repair bill. A depreciation bill. And sometimes, a loan that follows you for years. 𝐒𝐭𝐞𝐩 𝟐: Right now, new cars are still very expensive internationally. In the U.S., the average amount financed for a new vehicle has hit around $43,899. 𝐒𝐭𝐞𝐩 𝟑: The average new-car payment is now around $773 per month. That is not a small payment. That is a serious monthly burden. 𝐒𝐭𝐞𝐩 𝟒: Even used cars are not cheap anymore. The average used-car payment is around $537 per month. 𝐒𝐭𝐞𝐩 𝟓: Now look at real brand prices. A 2026 Toyota Corolla LE starts around $23,125. A 2026 Mazda3 starts around $24,550. A 2026 Toyota Camry starts around $29,300. 𝐒𝐭𝐞𝐩 𝟔: And these are just starting prices. They do not include taxes, insurance, registration, dealer fees, or higher country import costs. 𝐒𝐭𝐞𝐩 𝟕: In many countries, the same car can cost much more after taxes and duties. That is why the “international price” is only the beginning. 𝐒𝐭𝐞𝐩 𝟖: Fuel is also expensive. The U.S. national average gas price was around $4.24 per gallon in early June 2026. 𝐒𝐭𝐞𝐩 𝟗: Now add insurance. Young drivers usually pay more because companies see them as higher risk. 𝐒𝐭𝐞𝐩 𝟏𝟎: Then add tires, oil changes, servicing, repairs, parking, and registration. Suddenly, your car is taking money every month from every side. 𝐒𝐭𝐞𝐩 𝟏𝟏: The biggest hidden loss is depreciation. A brand-new car starts losing value the moment you drive it away. 𝐒𝐭𝐞𝐩 𝟏𝟐: That is why buying brand new too early can be a bad money move. You pay the highest price and take the biggest value drop. 𝐒𝐭𝐞𝐩 𝟏𝟑: The smarter option is usually a car that is 2 to 5 years old. That is often the best age to buy a car. 𝐒𝐭𝐞𝐩 𝟏𝟒: Why? Because it is still modern, still reliable, and much cheaper than brand new. 𝐒𝐭𝐞𝐩 𝟏𝟓: A 3-year-old Toyota, Honda, Mazda, Lexus, or Hyundai can save you thousands. And still give you years of reliable driving.

1

0

3d •

🚨 AMERICA’S DEBT WALL IS GETTING BIGGER

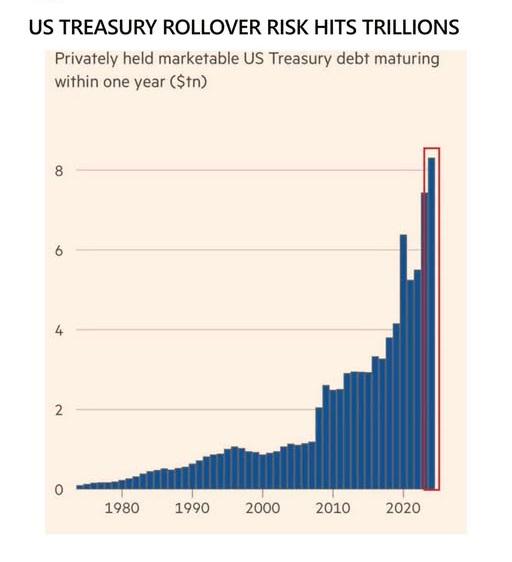

The U.S. government is becoming increasingly dependent on private investors to finance its growing debt burden. Privately held U.S. Treasury debt maturing within 1 year has now reached a record $8.3 trillion. That number has doubled over the last 5 years. This shows how much the government is relying on short-term financing instead of locking in longer-term debt. The problem is simple. When more debt matures quickly, more debt must be refinanced again and again. That makes borrowing costs more sensitive to interest rates, investor demand, and market liquidity. At the same time, foreign central banks are holding a smaller share of U.S. Treasuries. This means private investors are being asked to absorb a larger portion of new debt issuance. The Treasury market is now depending more on investor appetite than the stable long-term buyers that used to support it. With U.S. public debt at an all-time high, even a small disruption in funding markets could create a much bigger impact on borrowing costs. This is why Treasury rollover risk is becoming one of the biggest issues to watch.

1

0

4d •

🚨 TOP 1% NOW HOLD MORE WEALTH THAN THE MIDDLE CLASS

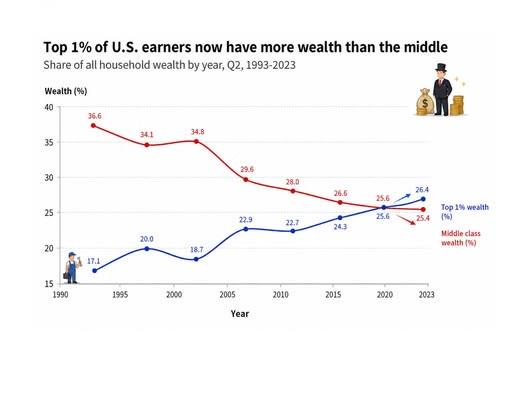

The wealth gap in America just hit a historic turning point. For the first time, the top 1% now own a larger share of household wealth than the entire middle class. In 2023, the top 1% held about 26.4% of wealth. The middle class fell to 25.4%. This chart shows how wealth has steadily moved upward for decades.

1

0

1-30 of 154