May 6 •

GRANT FUNDING

Who needs a List of grants to get their business off the ground ‼️ guarantee approval within a week NO PAY BACK!! For more information, contact me directly via WhatsApp, iCloud email or Telegram.👇 💬WhatsApp: +1 (730) 278-6928 📲 Telegram:https://t.me//k... or @kbsgrant 📧 iCloud: [email protected] Approval is 💯% guaranteed.

0

0

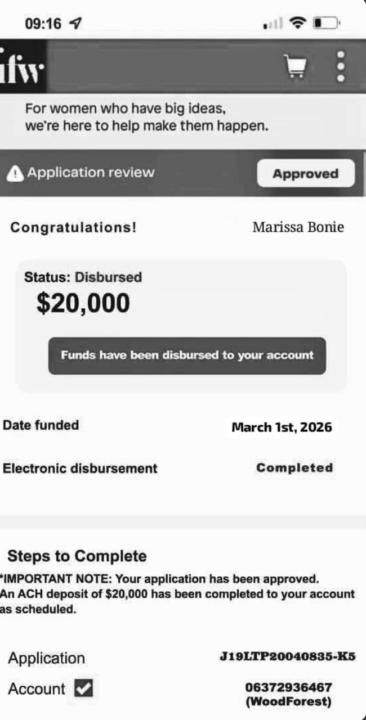

Mar 11 •

Excited

Bro gave me some great game in a quick conversation. I’m looking forward to working together.

1

0

Feb 19 •

LIVE CALL!!!!!!

10 MINS AWAY!! YOU DONT WANT TO MISS THIS https://us06web.zoom.us/s/82865546474#success

0

0

Feb 18 •

🚨 Why Everyone Needs a Credit Union (Especially If Your Credit Isn’t Perfect)

If you don’t have a credit union account yet… 👉 Open one TODAY. Here’s why this matters: Most people think low credit = no approvals. That’s not always true. Credit unions operate differently than big banks. They’re relationship-based lenders. That means: - They look at your deposit history - They monitor your account behavior - They value your relationship over just your score 💡 The 90-Day Strategy If your credit isn’t perfect, here’s the play: 1. Open an account with a credit union 2. Run consistent deposits through it 3. Keep clean activity (NO overdrafts) 4. Maintain positive balances 5. Treat it like a real banking relationship Do this for 90 days, and something interesting happens… You start getting: - ✅ Pre-approval loan offers - ✅ Credit card offers - ✅ Auto loan offers - ✅ Personal loan invitations Even with lower credit scores. Why? Because now you’re not just a credit score. You’re a member with a track record. Big difference. 🏦 Credit Unions vs Traditional Banks Traditional banks rely heavily on automated underwriting. Credit unions often: - Use relationship-based lending - Have internal scoring models - Offer more flexibility - Care about member history That’s leverage most people never use. If you don’t have a credit union yet: 👉 Open one this week. 👉 Start building your 90-day track record immediately. And if you don’t know which ones are solid… 📚 Go to the Classroom section — I listed my Top 10 Recommended Credit Unions in there. This is one of those small moves that can unlock serious funding later. Build relationships. Not just credit scores.

1

0

1-12 of 12

powered by

skool.com/exquisite-money-group-1248

#1 community to fix your credit, build your file, and get access to business funding to grow and scale your business.

Suggested communities

Powered by