Write something

Apr 24 •

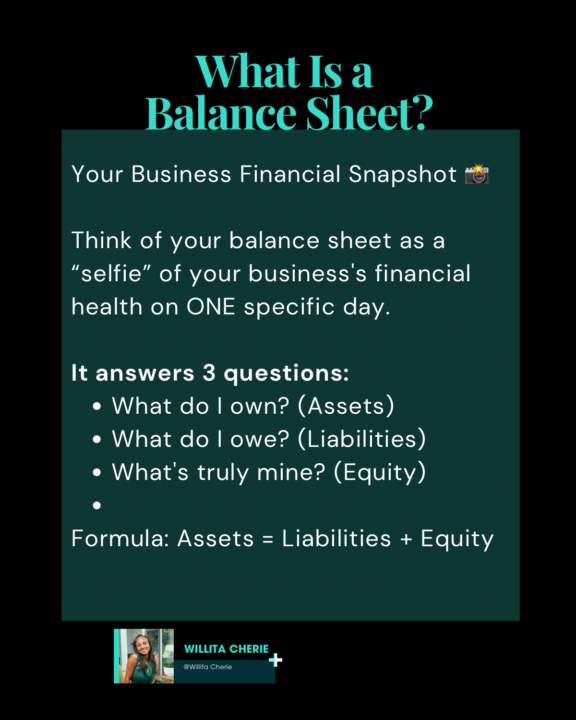

What to put on your Balance Sheet 🤔

In bookkeeping there are three financial reports you want to keep track of and keep current: the Balance Sheet, the Income Statement (also called a Profit and Loss or P&L), and the Cash Flow Statement. Today you’re learning the purpose of the Balance Sheet and what actually goes on it. So what is a Balance Sheet? The simplest way I can put it is think of it as a “snapshot” of your business’s financial position. You won’t get the full picture of everything that’s happened, but you will get an overall summary of the health of your business. Now let’s talk about what goes on it and where. I’m going to be completely transparent. I got so confused when I first learned about the Balance Sheet. So hopefully I can give you a much easier way to remember it. Everything on the left side shows what you have. Think cash in your bank account, invoices clients still owe you, your laptop, your equipment, maybe a business vehicle. If your business owns it or is owed it, it goes on the left. Everything on the right side shows who owns it. That breaks into two things: what you owe others like a credit card balance, a loan, or a vendor bill you haven’t paid yet, and what actually belongs to you as the owner. Whatever is left after all the debts are accounted for is your ownership stake in the business. Here’s the part that makes it all click. Both sides have to equal the same number. That is literally why it’s called a balance sheet. If they don’t match, something was recorded incorrectly and that is exactly why keeping your books current matters. The good news is you don’t have to build this by hand. Your bookkeeping software like QBO or Zoho generates it for you automatically.

0

0

Apr 17 •

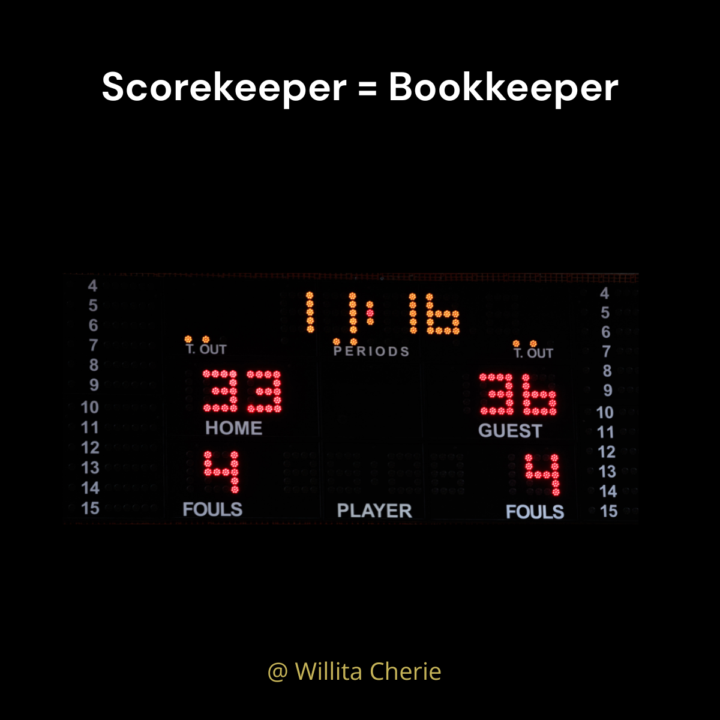

Your Bookkeeper and your Accountant are not the same person.

You might be paying for the wrong person, or missing one entirely. Think about a basketball game. Your bookkeeper is the scorekeeper at the table. Every point, every quarter, every play, they record it as it happens in real time. Your accountant is the analyst in the booth. They take the full game film and tell you what it all means. Where you left points on the board. What plays cost you. What to do differently next season. Your analyst cannot do their job if your scorekeeper never kept score. And if you have a scorekeeper but no analyst, you are just collecting stats with no strategy behind them. That is exactly what happens in your business when these two roles are missing or mixed up. You hand your accountant a pile of receipts at tax time instead of clean financial statements because no one was keeping score all year. Or you have a bookkeeper, but no one ever looks at what your numbers actually mean for your growth. Your bookkeeper keeps your books clean and current every month. Your accountant uses those clean books to advise you, file your taxes, and help you make bigger decisions. One more thing worth knowing: some bookkeepers have an accounting background, and some accountants have done bookkeeping work. The title alone does not tell you everything. Always ask what they actually do before you hire them. So where are you right now? Do you have a scorekeeper, an analyst, both, or neither? Drop it in the comments.

0

0

Mar 20 •

I apologize for my silence…..

Please don’t think that I have forgotten about you all. I have had a lot of big events happening in my personal life that has required a lot of my time. I should be good to go in April. In the meantime, I encourage you to review the content that I have posted to the page. Take care, Willita

1

0

Mar 3 •

Welcome New Members

We have new members in the community, but to kick off this month. I would like all the members in this community to introduce yourself and network 👇

0

0

Feb 20 •

Making good money but have NO idea if your business is actually healthy?

Look, I get it. You’re crushing it with your consulting/agency/service business. Money’s coming in. Life’s good. But here’s the thing nobody talks about… Just because you’re profitable doesn’t mean you’re financially stable. 😬 Think of it like this: Your profit & loss is like checking if you ate healthy today. Your balance sheet? That’s your full medical checkup. Meet Michael. He runs Strategic Growth Consulting and makes $485K a year. Sounds great, right? But when I dug into his balance sheet, some wild stuff popped up: 1. He’s hoarding cash like Uncle Scrooge (60% just sitting there doing nothing!) 2. Clients have already paid him $47K for work he hasn’t done yet 3. His business is actually worth $175K more than he realizes The crazy part? Most business owners like Michael have zero clue about any of this. I broke down Michael’s actual numbers in the carousel below. Don’t worry, I made it super simple. You’ll see: ✅ What you actually own vs. what you owe ✅ The 2 numbers that’ll tell you if you’re headed for trouble ✅ How to actually USE this info to make better decisions Drop a 🤯 if you’re realizing you should probably know this stuff too.

0

0

1-30 of 39

powered by

skool.com/cash-flow-confident-2227

Tired of 3 am money stress? Get simple systems to manage your cash flow so you can sleep at night and focus on growing your business.

Suggested communities

Powered by