Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Owned by Wendy

从迷茫到自由:半年找到方向和路径,两年实现时间与财富的自由! 在这里,你将获得:战略指引,清晰路径,实操方法与高能量支持。 高价值课程,高质量分享,定期答疑,在线讨论与挑战行动,带你从迷茫到行动,从困局到自由。 欢迎添加 Wendy 微信:WendyD1051,我朋友圈的内容非常丰富。

Your 9-5 exit : Turn US equity into cash flow and wealth. Make work optional, reclaim your time, and unlock the ultimate freedom to live life fully!

Memberships

SMC Engine

1.2k members • $297

Prosperity Foundations

8.4k members • Free

Crypto Calls

461 members • $145/month

Coaching Mastermind

59 members • $999/m

Joe's Mastermind

43 members • $999/m

Crypto Calls Lite

3.7k members • $47/m

41 contributions to Equity to Life Freedom

May 20 •

Are you still in the game?

Hey everyone, I'm not sure how many of you are still using what we learned in the 6-week course. You might have been energetic during those weeks, but now you're overwhelmed by work, life, everything. You might feel value investing is a bit slow, the premiums are too small to free you up. You might want to chase the hot stocks and double your account quickly. Or you find it hard to evaluate a business and you're not sure if you're doing it right. I just want to say — no method will work if you're not consistent. The only way to make money, or achieve anything, is to keep working on it. The way we do value investing can give you great returns with the lowest risk — but you need to keep working at it. It's a long journey. Strategy + mindset + circle. You need all three。 If you have any questions, please let me know. Hope everyone has a great day 🙌 Wendy

3

0

May 13 •

A note on LULU

We used LULU as an example several times during our 6-week crash course in February. Its price has dropped since then — I'd like to update what's happening. First, as I always mentioned, our course is only for educational purposes. We teach methods, strategies and frameworks, not stock recommendations. LULU has been just one of our case studies to illustrate our option strategies, not financial advices. That said, let's talk about where it stands. LULU's financials have looked great over the past few years, and our buy price was based on that track record. However, we do acknowledge there's a lot of uncertainty right now, and apparently that's an "EVENT" for this business. The latest round of selling was driven by the market not buying into the new CEO appointment, the ongoing proxy battle with founder Chip Wilson, and a leadership vacuum until the new CEO officially starts in September. Meanwhile, capital is flooding into AI and storage, etc — for companies with no near-term catalyst, the market simply sells off. That's how it works. What you need to do is make your own judgment: Is this still a good company? Has the fundamental story changed, or is the market just impatient? If you believe the fundamentals are intact, the Rule1 approach is to tranche in — keep reducing your cost basis, and keep selling calls on the shares you've owned, and be patient. In value investing, we don't use stop losses. Our goal is to own the company at the best possible price. But if you believe the fundamentals have deteriorated, then your strategy needs to adjust accordingly. That's your call to make. A few info: 1. Michael Burry added to his LULU position at $135 and $129, etc. LULU now represents 8.2% of his total portfolio. 2. Phil Town's current approach: "The bottom line is we are focused on reducing basis on LULU while we wait for the proxy battle to end this summer and the new CEO to come on board in September. We could see some price volatility between now and the end of the year so be patient as this event plays out."

2 likes • May 15

@Fady Eskandar Totally. We've gotta stay humble and keep learning from the market. That’s how we grow as value investors and actually make big money in the long run. It’s all about consistency—just keep practicing and play the game the right way.

May 13 •

Don't FOMO. Don't Panic. Stay calm and patient.

Just a reminder of who we are and what we do. We are long-term value investors at our core. Our goal is simple: own wonderful companies at great prices — less than 50% of intrinsic value, and of course, the lower the better. As value investors, the most important thing is to understand businesses, understand their moats, evaluate management, and patiently wait — sometimes for a very long time — until Mr. Market offers us a price that gives us a real margin of safety, or be extremely patient waiting for a great business to recover and return to its value. We use options as a tool, not the goal. We're not using them to speculate on price or bet on direction like other traders do. We use them to generate cash flow while we wait and to reduce our cost basis on positions we already own - with strong certainty. That's it. They serve our long-term strategy, not the other way around. Right now, the market is going crazy over AI. Money is pouring into momentum plays. Everyone's posting their 50%, 100%, 200% returns. And if you're sitting here holding value stocks that are flat or down, it's easy to feel like you're doing something wrong. You're not. Value investing and momentum trading are fundamentally different strategies. Different time horizons. Different return expectations. Different levels of effort, time commitments, and different lifestyles. Comparing your value portfolio to someone riding a momentum wave is like comparing a marathon runner's pace at mile 5 to a sprinter's 100-meter dash. They're not playing the same game. And life is a marathon -- the same as investing. Don't FOMO into what's hot, unless you know how to do it skillfully. Don't compare your interim returns to someone else's. That comparison will make you abandon your own strategy at the worst possible time. What truly matters as a value investor, and where you should spend your energy: 1. Understand companies — use 4M analysis. 2. Strictly follow our rules and option tools to tranche in (remember the V-shape strategy?). One tranche at a time. Keep your dry powder for a better price. 3. Be patient. Extremely patient.

May 11 •

Might be time to consider ROLPH Trade

With SPX and QQQ hitting fresh all-time highs, the SOX is up 224% in 13 months. The top 10 Nasdaq 100 performers have averaged 784% gains over the past year — exceeding both the 1999 and 2000 bubble peaks. Meanwhile, consumer sentiment sits at a record low. The entire market narrative rests on two letters: AI. No one can predict the day it ends, the upward trend might keep going for a while, however if you would like to pay insurance to hedge the risk, you may consider ROLPH trade. Remember, follow our rules learnt in session 6, 2% of your portfolio at most as an insurance, you may also tranche in, don't use up all your 2% at once. And this is not a trade to make money, it's an insurance for black swan.

3

0

Apr 30 •

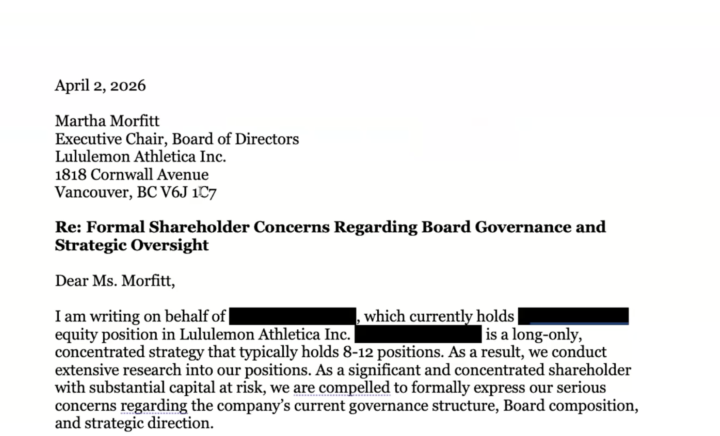

Phil's Team Wrote to LULU's Board

Phil Town's team sent a formal letter to Lululemon's board in April, raising two concerns: 1.A classified board structure giving directors three-year election cycles 2.Multiple long-tenured directors with minimal skin in the game — conditions that had quietly eroded accountability behind recent product failures and strategic missteps. The board responded constructively. LULU's VP and also the Executive Chair Martha Morphet personally called Phil's analyst, and confirmed support for declassification, which now appears in the proxy filing as a board-recommended "yes" vote. Three long-tenured directors have departed, replaced by Chip Berg (former Levi's CEO, bought $1M in shares immediately) and Essie Bracey, bringing real retail and brand-building experience. It shows that LULU's board are responsive to shareholders concerns with new composition, which is at least a positive sign. Also another note is, to us as investors, actually we don't need to hold lots of shares but as long as we can provide constructive feedback and suggestions, which offers value for executeive time, you might consider to try this way to engage in the future as well. The below screenshots are a small part of the letter. LULU's stock price drops a lot these days, but to be honest it doesn't bother us as Rule1 investors if you really understand our system, follow the strategy and bear in mind our goal is long-term value investing, I will cover this in the next days. :) Happy investing, Wendy

4

0

1-10 of 41

@wendy-dai-9150

Founder of BraveSolutions | F.I.R.E Achiever | Ambitious Few | Strong Mind. Clear Vision. Free Life.

热爱自由,无限好奇,终生成长,活出心花怒放的人生!

wechat: WendyD1051

Active 4d ago

Joined Aug 23, 2025

sydney