Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

What is this?

Less

More

Owned by Triston

The goal is to help as many people as possible repair and rebuild their own credit.

Memberships

Credit 2 Cash Mastery

201 members • $29/m

BnB Cashflow Society

128 members • $47/m

CEO's ONLY UNIVERSITY

249 members • $150/month

CREDIT 2 MILLIONS

66 members • $97/month

35 contributions to SAVAGE UNIVERSITY

Mar '25 •

NAVY FEDERAL BACK DOOR METHOD 🔥

I got more homework for y'all. If you don't have a Navy Fed membership, JOIN NOW‼️ I saw a few people mentioned they couldn’t get into Navy Fed This method has worked for majority of my clients To gain access to a Navy Federal CU membership: - Call Navy Fed (only can be done over the phone) - Tell the rep ‘your Grandpa served in the Navy for years and he past away, but you don't remember too much of his information,and that you only know what Branch he was in. - (Pick Any Branch) If this doesn’t work, call back to reach a different rep. Once you get the right rep they will Walk you through the entire process and your in! This method helped thousands of people get into Navy Fed SUCCESS RATE: 100/100

0 likes • Oct '25

@Jonathan Rude Yes sir it works

0 likes • Jan 2

@Tyler Berry always🙌

Apr '25 •

💥Equifax or Experian 72 hr Credit Sweep Method/Data breach fast removal instructions 🧹🚀

*Disclaimer I have nothing to do with how long it takes them to remove your accounts. I’m just sharing what worked for me and a client of mine I made sure to test this at least 2 times before posting and both times took 48hrs to remove. Even if it takes longer than 2 days just run the play cause it’s clearly an expedited method to get negatives removed. Don’t hit my DM saying “it’s been 2 days and no results” I will respectfully ignore. I’m just here to share my success with the groups that I’ve learned from Step 1️⃣ -Go to chat gpt and type “Write me a letter to Equifax stating that I am a victim of the data breach and would like all accounts mentioned to be blocked and deleted pursuant to 15 USC 1681c-2(a).” -Copy and paste the template into word and edit your personal info and negative accounts on it then save . This will be your dispute letter that you attach to your complaint Step 2️⃣ -Go to identitytheft.gov and make an ftc report for the negative accounts. At the very end , put in the comment box “I am filing this FTC Identity Theft Affidavit to report fraudulent accounts appearing on my consumer FICO credit report which i do not recognize as reported and which are the result of identity theft and fraud. I am also aware that all of my information was exposed in the Equifax Data Breach. Please remove the accounts and inquiries listed: …… *Save to your phone /computer Step 3️⃣ -Go to https://www.equifaxbreachsettlement.com -Scroll down and click on “Find out if your information was impacted” -Fill out form and screenshot the results if it says “Your information WAS impacted” -Orrrrr just use the screenshot attached to this post 😉 Step 4️⃣ -Login to my.equifax.com -Go to dispute center -Go to file a dispute -Click on the negative accounts you want to dispute -click account ownership and fraud issues -click “I am a victim of identity theft and have a police report or FTC ID Theft Report

1 like • Nov '25

@Emilyn Garcia hey I’ll make sure to fix this

Oct '25 •

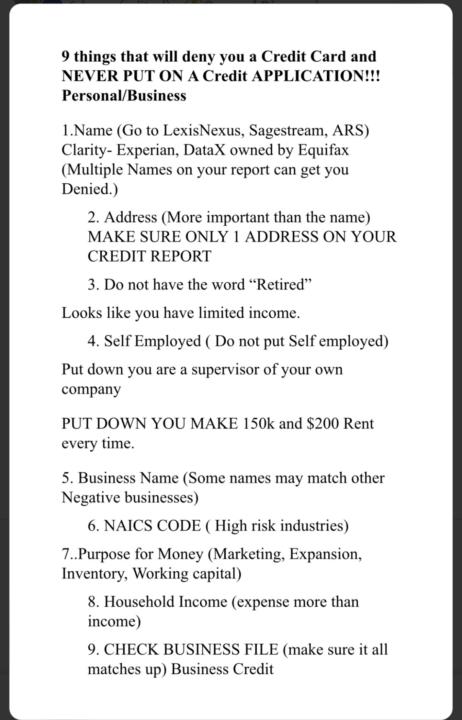

9 things that will deny you a Credit Card and NEVER PUT ON A Credit APPLICATION!!!

[attachment]

0

0

1 like • Jul '25

yes it is

Apr '25 •

✅This Will Be A Good Way To Build Your Credit!💳

Top 5 Primary Trade lines To Put On Credit Report 1. Credit Strong - Reports To All 3 2. Kovo - Reports To All 3 3. Meet Ava- Reports To All 3 4. Loqbox- Reports To All 3 5. Kikoff- Equifax & Experian All Will Report A $2500 Dollar Line Of Credit To Your Report For $20 Dollars A Month So If You Get All 5, For $100 Dollars A Month That Will Have $10,000 Dollars Worth Of Trade Lines Reporting Every Month Which Will Super Boost Those Scores 👍🏿😯😎 🚨🚨🚨Then go get a car from carmax keep it 28-30 days take it back get refund and now you have a paid off car on your credit🚨🚨🚨🚨💥🤯 You can take a full 30 days (up to 1500 miles) to decide if the car you buy is right for your life. As long as the condition is consistent with when you purchased it and you've driven fewer than 1500 miles since your purchase, you can bring it back within 30 days and we'll help you complete your return.

3

0

1-10 of 35

Active 23h ago

Joined Jan 15, 2025

Powered by