Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

What is this?

Less

More

Owned by Samiel

THE 1 WHO SUCCEED

Memberships

AI Automation (A-Z)

161.3k members • Free

Bizlaunch.io

746 members • Free

CR

Credit Report DIY

634 members • Free

Quantum Creator Growth

53 members • $197/m

79 contributions to Successful 800 Program

11d •

The Truth Hurts: You Can Lead a Horse to Water...

Let’s keep it 100% real for a second. The biggest reason people don't see results in their credit, their business, or their life isn't a lack of information. We live in an era where the blueprints are right in front of you. The real issue? People either don't use the tools they are given, or deep down, they just don't want better for themselves badly enough to change. You can buy the software, join the inner circle, and download the templates. But if those tools just sit there collecting digital dust, your situation stays exactly the same. You can take the horse to the water, but you can’t force them to drink it. If you are tired of looking at the water and you’re actually ready to start drinking, I’m laying out the ultimate 90-Day Gems Hack roadmap. No fluff. Just the exact systems to structure, automate, and fund your life. Choose what side of the fence you're on, and let's get to work.👇

1

0

11d •

im back

i have alotttt of new gems... The Credit Game is changing, fixing credit is the government worse nightmare.

1

0

20d •

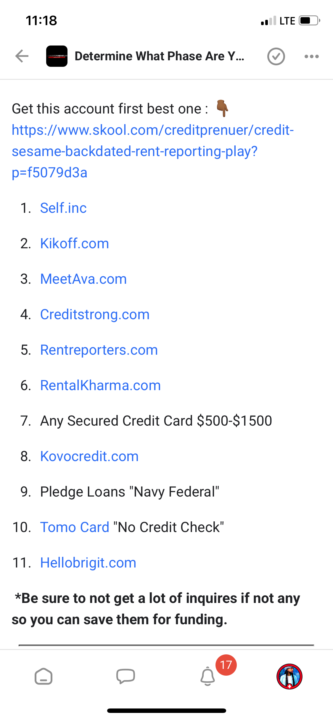

ADD TRADELINE AND PRIMARIES TO YOUR CREDIT

HERE A LIST OF ACCOUNT, THAT CAN BOOST YOUR SCORE, AND GET YOU APPROVE.

1

0

21d •

going live in 2 days

3rd challenge out of 6. next week is when we take action and getting funding

1

0

1-10 of 79

Active 2d ago

Joined Jul 23, 2025