Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Memberships

Ultimate Freedom Network (UFN)

949 members • Free

Spanish After Hours

7.3k members • Free

OFM | Fameu (free course)

10.4k members • Free

MyFirstHack | Cybersecurity

93.2k members • $9/month

Free Skool Course

71.6k members • $1

Pocket Singers Free

18.6k members • Free

Top Chess Community

20.3k members • Free

Symoné GovTech Community(Free)

24k members • Free

Join Mihai to make money fast

1.3k members • Free

8 contributions to Business Ownership Academy

3d •

Top Reasons Why SBA Lenders Reject Franchise Loans

SBA lenders often reject franchise loans due to a combination of tightening market conditions, borrower financial red flags, and poor deal architecture. In 2026, the lending environment for SBA 7(a) acquisition loans has become more restrictive, requiring a more strategic approach to secure funding. Top Reasons Why SBA Lenders Reject Franchise Loans - Tightening Standards and "The Box": Many banks have a specific "box" or risk profile they are willing to fund. If a deal doesn't perfectly fit their internal covenants or regulatory risk levels, it may be denied, even if it is a strong opportunity. - Operational Inefficiencies: Lenders often reject applications due to non-financial "hair" on the deal, such as name variations or address discrepancies on a credit report that trigger automated algorithm declines. - Financial Red Flags: High personal credit card utilization and collateral shortfalls are major deterrents [Conversation History]. While some "air ball" loans are approved based on strong cash flow, many banks still require deals to be backed by real estate or a second lien on a personal residence. - Lack of Transferable Experience: Lenders want to see that the buyer has the background necessary to run the business successfully. A lack of industry-specific or management experience can be a primary reason for a decline. - Incompetent Lenders: Working with a bank that is not a Preferred Lender (PLP) or one that relies on monthly loan committees can lead to a deal falling through late in the process. How to Get Your Franchise Loan Approved - Prioritize "Certainty of Close": Choose a PLP lender who can underwrite the file in-house rather than sending it to the SBA for approval, which significantly speeds up the process and increases the likelihood of closing. - Tell a Compelling Story: Work with a Business Development Officer (BDO) who acts as your advocate. A good BDO knows how to present "hair on the deal"—such as a lack of existing revenue or a new operator—by highlighting compensating factors like high credit scores, significant reserves, or past project success.

1 like • 2d

Hey everyone

Jun 5 •

Real Estate & Business Expo

1 DAY TO GO Tomorrow is the day. The Real Estate & Business Expo goes live tomorrow with Beau Eckstein, Michael Zuber, and Trent Lee. Get ready for actionable insights on business ownership, real estate investing, funding, and wealth building. What You’ll Learn - How to get started in real estate investing (even in today’s market) - Proven franchise and business models replacing W-2 income - How SBA loans and other funding options actually work - Real deal structures and case studies - How to scale a business using systems, teams, and leverage - The “Triangle Method” for building long-term wealth 📅 Tomorrow | June 06 | 9am PST | Live on Zoom 👉 Last chance to reserve your spot. https://www.eventbrite.com/e/real-estate-business-expo-tickets-1985666575179

0 likes • 20d

@Raina Brook Hello how are you doing today ! what have you been trying so far in this community" Any results yet or you are just getting started..

0 likes • 11d

@Linda Barbara Fleishman Great question, Linda. In my experience, execution is where most people struggle. Many people have access to information and strategies, but consistently taking action and adapting when things don't go as planned is often the hardest part. It's similar in e-commerce dropshipping finding products and learning marketing is relatively easy, but success usually comes down to testing consistently, analyzing data, and sticking with the process long enough to find what works.

26d •

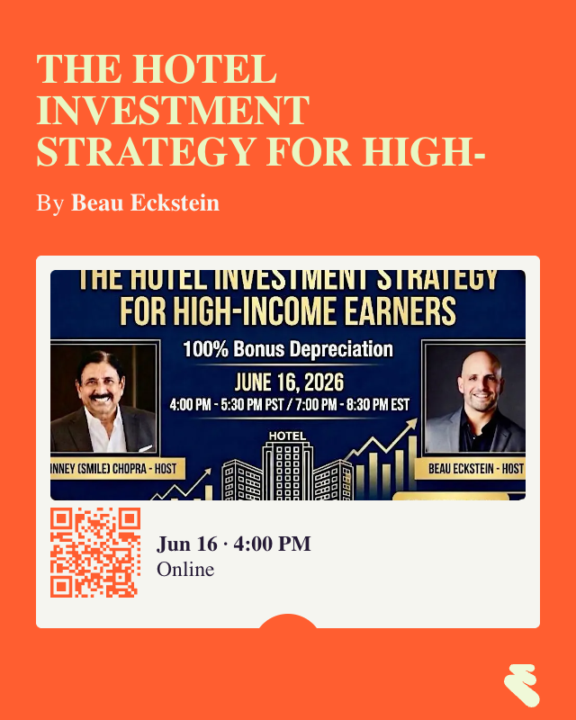

The Hotel Investment Strategy for High-Income Earners

Learn how to maximize your hotel investments with smart bonus depreciation moves tailored for high earners. Discover how accredited investors are using hotel investments to build wealth while potentially creating significant tax advantages. If you're a high-income earner, business owner, physician, executive, or accredited investor, you may be looking for ways to do more than simply earn income—you may be looking for ways to keep more of it. Join us for a special educational webinar where we'll explore how hotel conversion and re-flag investments can potentially provide: - Passive income - Equity growth - Value-add appreciation - Cost segregation benefits - 100% Bonus Depreciation opportunities - Long-term wealth-building strategies Many investors are surprised to learn that hotels are among the most depreciation-rich real estate asset classes due to the significant amount of furniture, fixtures, equipment, technology systems, and land improvements they contain. Through cost segregation, these assets may qualify for accelerated depreciation, creating substantial first-year tax deductions. What You'll Learn - How 100% Bonus Depreciation works - Why hotels are one of the most attractive asset classes for depreciation strategies - How cost segregation can accelerate tax deductions - Strategies accredited investors use to potentially reduce taxable income - The differences between passive and active real estate tax treatment - Real Estate Professional Status (REPS) considerations - How hotel conversions and re-flags create value through repositioning and brand upgrades - How investors evaluate hospitality opportunities for cash flow, appreciation, and tax efficiency Featured Case Study: Marriott Hotel Conversion & Re-Flag Opportunity We'll review a real-world hotel repositioning project involving the conversion of a downtown Columbus property into a flagship Marriott-branded hotel. Topics include: - Value-add acquisition strategy - Renovation and rebranding plan - Market and demand drivers - Potential investor returns - Cost segregation opportunities - Bonus depreciation planning considerations - Exit strategy and long-term wealth creation potential

0 likes • 25d

Interesting strategy. Many investors focus only on returns, but understanding how tax efficiency, depreciation, and value-add opportunities work together can have a major impact on overall wealth creation. Looking forward to learning more about the hotel conversion and re-flag approach and how it fits into a long-term investment portfolio.

0 likes • 11d

@Henry Andrew so have heard about ecommerce dropshipping?

12d •

Can a seller note cover the entire 10% down?

A lot of people ask if a seller note can cover the full 10% equity injection on an SBA acquisition loan. The short answer? Usually no. Here’s how it typically works in today’s lending environment: A common structure is what I call the “5% / 5% split.” The seller carries 5% of the deal on full standby, and the buyer brings the other 5% in cash. That combination helps satisfy the SBA’s typical 10% equity requirement. But here’s the important part most people miss: Banks want to see that YOU have some skin in the game. Why? Because lenders want confidence that the buyer is financially committed to the success of the business. If the structure relies entirely on debt, underwriting gets much harder, especially in today’s tighter lending environment. Now, for a seller note to even count toward equity injection, it generally must be on full standby. That means the seller receives no principal or interest payments for a specific period, and in some cases, for the life of the SBA loan. This is where deal structure matters. As SBA 7(a) acquisition lending tightens, banks are scrutinizing deals more carefully. They want prudent structures with proper alignment between buyer, seller, and lender. That’s why creative financing is not just about reducing cash out of pocket. It’s about building a deal structure the bank will actually approve. The right capital stack can make or break the transaction. If you’re working through an acquisition and want clarity on how to structure your deal properly, book a call at bookwithbeau.com

0 likes • 11d

Great explanation, Beau. The "skin in the game" piece is often overlooked by first-time buyers who focus solely on creative financing. Lenders aren't just evaluating the business they're evaluating the buyer's commitment and ability to navigate challenges after closing. The 5%/5% structure seems to strike a balance between reducing upfront capital requirements and giving banks the confidence they're looking for.

20d •

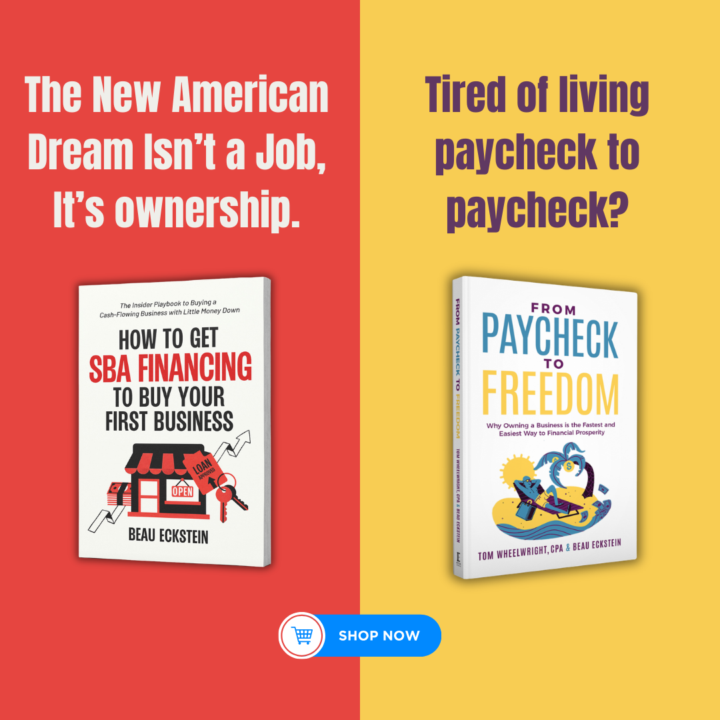

The "Gateway" Strategy

1. Start Small - Use a "gateway business" to transition into ownership without immediately leaving your current job. 2. Semi-Passive - Models Explore niche opportunities like AI vending or textile recycling for a more passive income stream. 3. Low Entry - Focus on business models that allow you to move into ownership with manageable startup costs. Build your exit strategy while you’re still employed. Find your ideal gateway business at bookwithbeau.com. Buy now: 👇 How to Get SBA Financing to Buy Your First Business From Paycheck to Freedom

1 like • 18d

@James Simmons Hello how are you are doing it nice to meet you i hope you are enjoying this community

1-8 of 8

@ozaha-kerry-8247

USA-based entrepreneur dedicated to business growth, personal development, and building impactful connections.

Active 1d ago

Joined Jun 9, 2026

America/Los Angeles