Activity

Mon

Wed

Fri

Sun

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

What is this?

Less

More

Memberships

Cloud Residents · US Credit

752 members • Free

Synthesizer: Free Skool Growth

41.8k members • Free

AI Automation Society

360.3k members • Free

73 contributions to Cloud Residents · US Credit

2d •

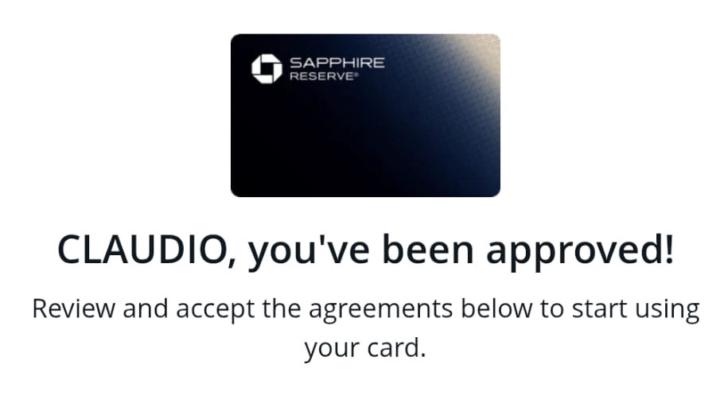

Chase Saphhire Reserve approved (150.000 UR Offer)

Today I got approved for the Chase Saphhire Reserve card. Applied online via the Chase app. Simply clicked on the pre-approval in the app, updated my income (I used the same amount from my last application), and checked the boxes for confirmation. -> Wait 30 seconds. Congratulations! No documents were required. No VPN/Proxy used. I was already pre-approved for both Chase Saphhire Cards in the app for 4 weeks. I was lucky to wait for the best offer ever for CSR. I have an Chase Checking Account for almost 2 years. This was my 4th us credit card (Amex HH (2 years), Amex Green (1 1/2 years), Chase Freedom Unlimited (7 month). Credit Score before the application today: 754 (Equifax). I will try for my first Capital One card in 30 days in the US at an Capital One Cafe... I know, it will be a short time period between both aplications, but I dont know, when I will be back in the USA after my next vacation. Has anyone visited the Capital One Cafe in Las Vegas oder in Denver?

1 like • 20h

150K UR is the best CSR offer you'll see.

6d •

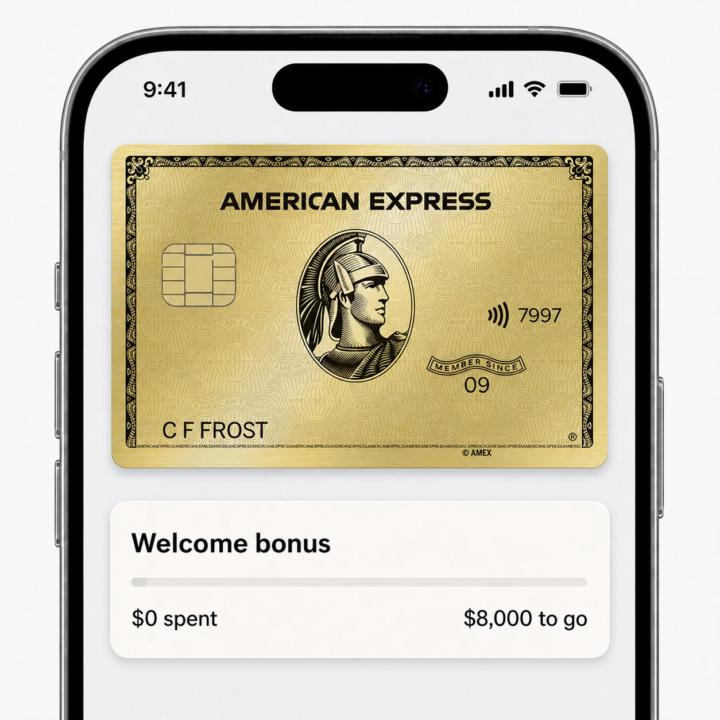

Amex Gold: 60th Anniversary

Amex rolled out changes to the Personal Gold card on April 30. The marketing highlights the shiny stuff - 5X on travel, Hertz status, new dining credit options. But there's a catch buried in the fine print that changes who can even get this card going forward. The signup bonus spend requirement jumped from $6,000 in 6 months to $8,000 in 6 months. That extra $2,000 doesn't sound massive, but for a lot of people who were spending around $1,000 a month, the Gold just went from "perfect fit" to slight "out of reach." Why this matters for Cloud Residents Many in our community are building US credit with an ITIN, often managing spending across borders. The Gold card was one of the best bridge options - easier to hit than the Sapphire Preferred ($5K in 3 months) or Venture X, but still a solid Amex entry point. At $8K in 6 months, it's now essentially in the same tier as those cards. That bridge option is gone. What changed for existing cardholders • 5X back on travel booked through the Amex portal, up from 2X • Mid-tier Hertz rental car status included • Two new options to use the $10 monthly dining credit • No annual fee increase - this part stayed the same Bottom line If you already have the Amex Gold, you're getting a few extras without paying more. If you were planning to apply, the math just got slight tighter. Source: https://www.americanexpress.com/en-us/newsroom/articles/products-and-services/u-s--consumer-american-express-gold--card-introduces-new-and-enh.html

Poll

17 members have voted

0 likes • 20h

Amex keeps making it harder

4d •

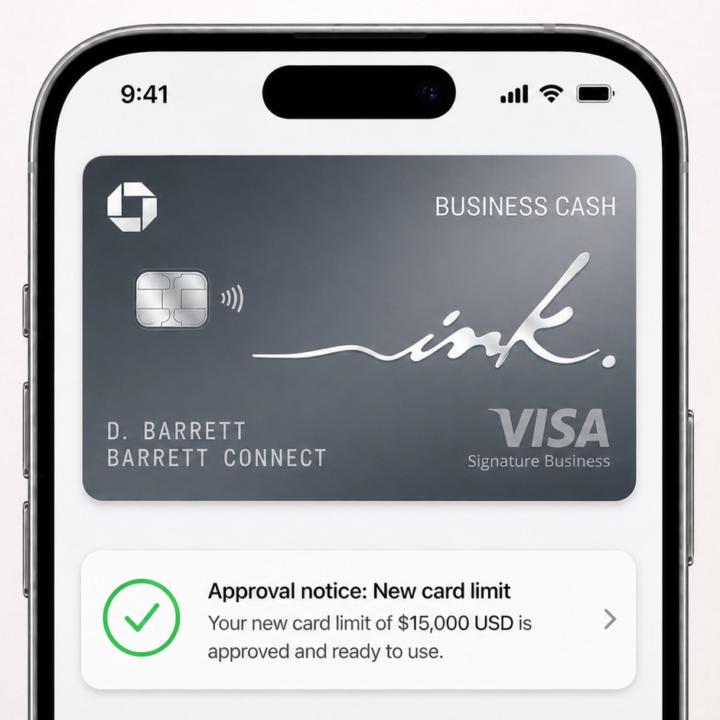

5 Banks That Approve New LLCs

Most people think you need old LLC with business credit score and a stack of bank statements to get approved for a business credit card. That's not how it actually works. There are banks right now that will approve a brand new LLC on personal credit alone. - No income docs. - No revenue verification. - No accountant needed. If you're a Cloud Resident building your US credit with an ITIN, this is one of the fastest ways to stack business credit early - while your LLC is still fresh and before you have revenue to show. Here are the 5 banks doing it. Chase Cards: Ink Business Unlimited or Ink Business Cash They pull Experian. 12 months 0% APR on both. You can apply for 2 cards on a single hard pull. Limits go as high as USD 50,000 on a clean credit file. American Express Cards: Blue Business Plus or Blue Business Cash They pull Experian, but here's the advantage: if you already have any personal Amex relationship, subsequent business applications are soft pulls. You can test multiple cards without damaging your score. Starting limits typically are around USD 2,000. Wells Fargo Card: Signify Business 12 months 0% APR. You do need a 60-day relationship with Wells Fargo before applying. Most starting limits I've seen are around USD 10,000. Worth opening a business checking account now and letting it age. US Bank Cards: Business Triple Cash or Business Platinum They pull TransUnion. No prior relationship required to get approved. Currently offering 0% APR for 12 months - worth noting this is shorter than the 18-month promo they ran for years. Starting limits are usually small, around USD 3,000, but they tend to increase to USD 10,000 and above over time. Bank of America Cards: Business Advantage 0% APR for 7 months. They prefer applicants with a existing checking account - deposits over 90 days tend to unlock better limits. If you're planning ahead, park some money there first. Bottom line: if your personal credit is solid and your LLC is newly formed, you don't need to wait for business revenue to start stacking cards. These 5 banks are the real no-doc plays.

Poll

38 members have voted

0 likes • 20h

Amex biz soft pull after personal card is 100% real. Tested it.

6d •

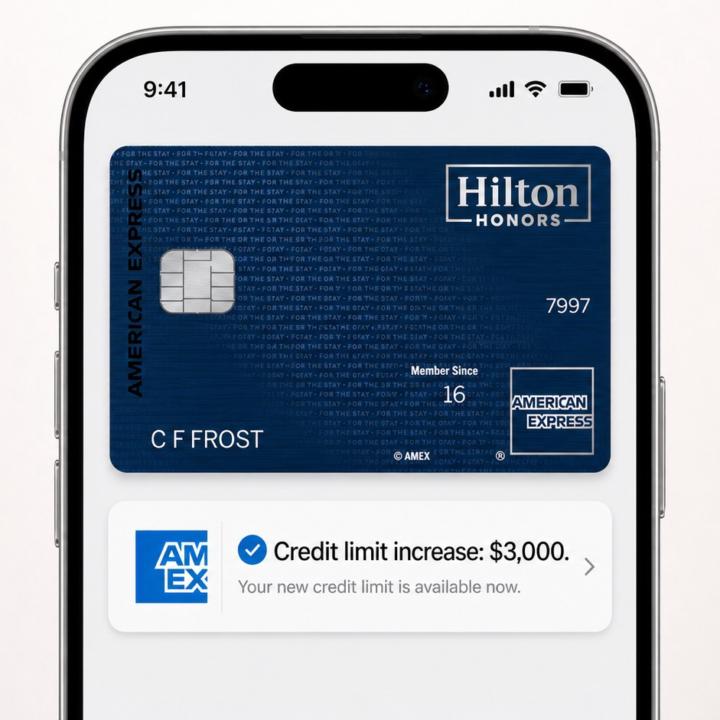

Credit Limits Without a Hard Pull

Most banks are still using the income you told them years ago. That outdated number is quietly capping your credit limits. Here's the full playbook to stack soft pull increases across your cards. Update Your Income First Go into every bank app and refresh your income. If you have household income, include it. You're not lying. You're just not selling yourself short. Banks won't raise what they don't know about. Request the Increase Most banks do credit limit increases with a soft pull. Your score stays exactly where it is. And don't ask for a tiny bump. Ask for 2X to 3X your current limit. They'll either approve or counter-offer. Either way you come out ahead. Get the Timing Right This is where people mess up. Wait at least 3 statement cycles on a new card before requesting. After that, request increases every 30 days. A lot of banks say 6 months, but you'd be surprised how many will approve back-to-back increases if your credit file supports it. Use the Card For the next 2 to 3 months, make that card your workhorse. Gas, groceries, bills, subscriptions. Spend, pay it off, spend again in the same cycle. One or two cycles of heavy usage is enough. Don't carry a balance. Just show activity. Never Accept a Low Limit Quietly If you get approved for a limit that feels low, call in. Give a real reason. A trip, a wedding, a big life event. That one call can take you from USD 5,000 to USD 10,000 or more. Move Limits Between Cards Here's the thing most people don't know about. If you have one card with a high limit you don't fully use, you can shift that limit to a new card at the same bank. That's how people go from USD 5,000 limits to USD 50,000+ on the same accounts. No new application required. For Cloud Residents building credit with an ITIN, these moves matter even more. Soft pulls protect your file from hard inquiries while it's still growing. Strategic limit increases signal trust to other banks. And a thicker profile with higher limits opens doors to better cards down the line.

Poll

20 members have voted

0 likes • 20h

@Al K I've been through FR. They check bank balances, not the income number you typed. Changing it now is riskier than leaving it.

3d •

Parker Shuts Down - Ramp Is The #1 Replacement

Parker is done. Officially shut down May 4, 2026. Patriot Bank confirmed. Cards are dead. If you had one, you already got the email - some of us here in Cloud Residents received it too (including me). This one stings. Parker was one of the best go-to cards for e-commerce. Shopify sellers, high-revenue businesses, anyone who needed real spending power without the usual underwriting headache. Gone. Here's what you switch to: Ramp. And honestly Ramp was already the better product. Why it's the easiest approval in the game right now: • Net 30 - straightforward, no tricks • Zero documents. No P&L statements, no YTD, no tax returns. Nothing • Link your business bank account and Ramp pulls everything itself • Approves 40-60% of your average bank account balance • Limits up to USD 350K - seen it firsthand • All you need: an ITIN and a business bank account (no sole prop) I've watched over 12 Ramp approvals come through in the last month and assisted with a few closely. The pattern holds. It works. $1,000 Bonus is still one of the easiest to claim too. Flex One is a backup option (onboarding sucks). I've been using it for about a year and a half. If Ramp somehow doesn't work, it's there. But Ramp is plan A for a reason. For more options: the business credit cards section inside the classroom is going live soon. I'll add more alternatives there. Parker was good. Door's closed. But the better door was already open. See you in comments, Ain - Cloud Resident

0 likes • 2d

Same 😓

1-10 of 73

Active 19h ago

Joined Nov 14, 2025

İstanbul, Türkiye

Powered by