Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

What is this?

Less

More

Memberships

The Perfect Loophole

68 members • Free

7 contributions to The Perfect Loophole

Apr 11 •

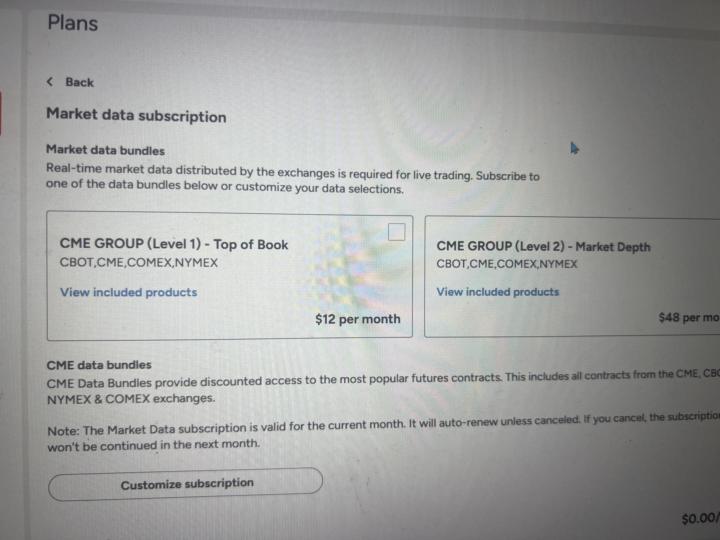

Market Data Subscription

Hey Perfect Loophole Team! Which CME GROUP LEVEL are you using on Trade Ninja that works with the system we’re implementing ?

0

0

Apr 3 •

Where are the NEW videos...?

I know some of you are wondering where the HELL are the new videos... And rightfully so. I'm doing my best to edit the videos but due to my vision issues, I see double for days in a row and its very frustrating to get anything done... I will get them out and I'm working diligently to make sure I deliver something that you all can level up from.... Thank you all for being patient with me. I'll try to speed up the process with this adobe software to get these courses out to y'all...

1 like • Apr 3

Strength and Courage Jerrell 💪

Mar 27 •

Archer Aviation - TaTi REPORT

Please download this information into your AI LLM... This is the assessment on something I am investing in long-term... Archer Aviation. This include Prompt Framework below...

1 like • Mar 27

My findings: Below is a clean Archer report built in the style of your master prompt and grounded in the dossier you uploaded. I used your prompt framework from the uploaded master prompt and aligned the substance with the Archer dossier you provided. Archer Aviation (ACHR) Report Executive Summary Archer Aviation is still a certification-and-scale story, not a mature operating company. The bullish case rests on FAA progress, early pilot operations in 2026, and Archer’s unusually large liquidity cushion for a pre-revenue eVTOL company. The bearish case is that Archer remains deeply cash-burning, effectively pre-revenue, exposed to dilution, and vulnerable to any certification, manufacturing, or legal setback. The most important positive data point is that Archer reported 100% FAA acceptance of Midnight’s Means of Compliance in January 2026, which management frames as a major step toward the next certification phases and targeted passenger-carrying flights in 2026. The most important negative data point is that the company is still fundamentally financing time, not monetizing scale, with only about $0.3 million of 2025 revenue against a roughly $618 million net loss. Default trade stance: cautious. Archer is interesting, but unless price action confirms a reversal, it is still better treated as a speculative setup than an investable trend. Your uploaded dossier’s conclusion is still the right posture: either wait for confirmation above resistance, or treat any entry near lows strictly as a defined-risk bounce trade. Company Overview and Business Model Archer’s core product is the Midnight eVTOL aircraft. The business model has four main pillars: aircraft sales, direct air taxi operations, defense and hybrid-electric programs, and monetization of aerospace/powertrain technology. That mix matters because it gives Archer several narrative paths to revenue, but today most of those paths are still conditional rather than proven. The strongest commercial demand headline remains the United-related aircraft agreement, but Archer’s own materials make clear that these agreements are conditional and subject to further definitive terms and regulatory progress. So the order book is best viewed as a demand signal, not bankable revenue.

Mar 23 •

VERY IMPORTANT tool you’ll need…

When you guys have Ninjatrader on your system/pc let me know so I can get you plugged in… This exposes one of the loopholes in REAL TIME‼️ I cant remember the date I recorded this but it should be in the video…

1 like • Mar 24

Locked in with Trade Ninja. Live account, I will be funding in two days when my new debit comes.

Mar 23 •

THIS IS PART 3...

Most traders look at the E-mini S&P 500 and only see price. They do not see what is actually moving it. In this video, I break down the different sectors behind the E-mini S&P 500, and I also go into 3 key segmented sectors: banks, brokers, and transportation. Because if you do not understand what sectors are leading, lagging, or breaking down underneath the surface… then you are trading blind.

3 likes • Mar 24

Insightful video

1-7 of 7