Activity

Mon

Wed

Fri

Sun

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

What is this?

Less

More

Memberships

Cloud Residents · US Credit

752 members • Free

2 contributions to Cloud Residents · US Credit

Mar 23 •

How important is it to keep putting spend on cards?

I have a couple of Amex cards (HH & Surpass) and after I got the WB I stopped putting spend on the cards. I feel like this put me on some sort of bad list with Amex as I just can't get approved for any other new cards besides the Biz Plat last year. Is it important to keep putting spend on the cards? Even if they're small charges?

1 like • Mar 24

@Apple Service Will try that, thanks!

0 likes • Mar 24

@John Flack Got my basic HH a year ago and the Surpass around 9 months ago. HH I almost never use. Surpass I use the quarterly credits, but not much outside of that.

Feb 18 •

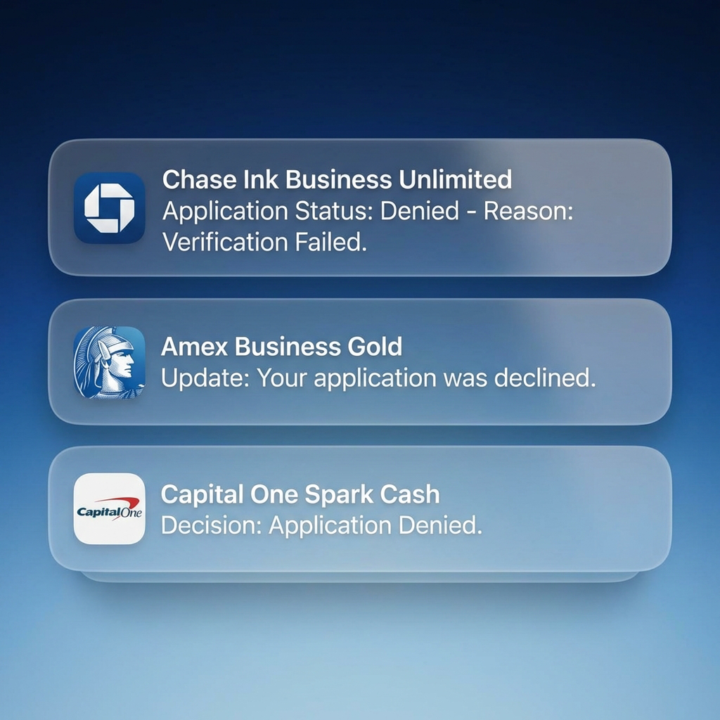

The 5 Application Killers (And How to Avoid Them)

There are 5 specific things you should never put on business credit card applications because they instantly trigger denials. Banks won't tell you what you did wrong. You just get a rejection and a hard inquiry slapped on your report. Here is exactly how to avoid that. 1. Employment Status Never put "unemployed," "retired," or "self-employed." Banks view these as unstable. Always use employed. Even if you are a business owner, you can be an employee of your own business. Underwriters don't fact-check job titles - they just judge how risky you look on paper. 2. Inflated Income or Revenue Avoid inflating your numbers. Banks don't always ask for proof, but they compare your income claims against industry data, deposits, business age, and your existing credit limits. If the numbers don't match your profile, they decline you automatically. 3. Ignoring Personal Credit Business credit approvals still mirror your personal limits. If your highest personal limit is $5k, they are not giving you $30k on the business side. They’re just not. 4. Too Many Applications Applying at 5 banks back-to-back looks desperate. Plus, many banks use the same underwriting systems, so it looks like applying for the same card multiple times. The safe zone is 0-3 inquiries in the past 6 months per credit bureau. 5. Funding Reason Only use "good" reasons for needing funding. Never write "debt payoff" or "to cover bills." Banks see that as financial trouble. Use growth reasons instead: Inventory expansion, advertising, hiring. More growth means more money to repay the bank. See you in comments, Ain - Cloud Resident

1 like • Feb 18

Re: 4. Too Many Applications Would you still count declines in your 0-3 safe zone? lol

1-2 of 2