Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Memberships

Acquisition Operator Network

17 members • $49/month

67 contributions to Acquisition Operator Network

11d •

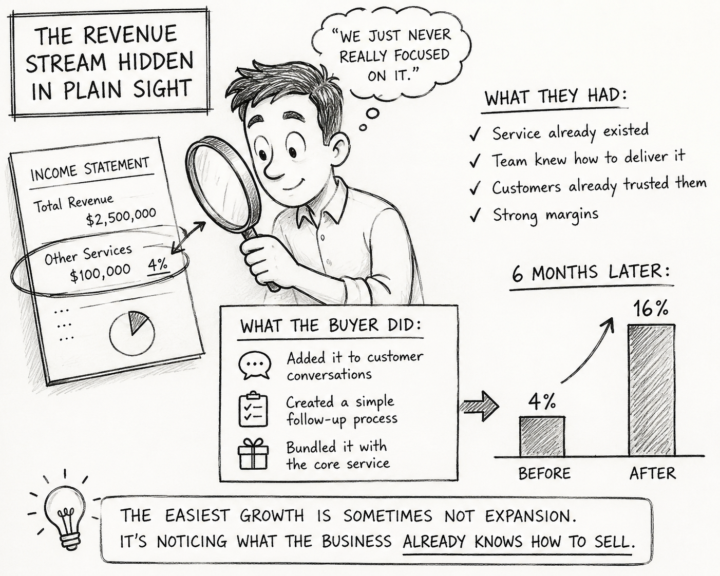

The Revenue Stream Hidden In Plain Sight

While reviewing the financials after closing, the buyer noticed a small revenue line item that barely registered. It represented only about four percent of total sales, and when he asked about it, the seller brushed it aside as an occasional add-on. The employees treated it the same way. Customers seemed to like it, the margins were excellent, yet no one actively promoted it. Curious, the buyer asked why. The seller's answer was simple. "We just never really focused on it." He realized that phrase often hides opportunity. The service already existed. The team already knew how to deliver it. Customers already trusted the company enough to purchase it. There was no research and development required, no new equipment to buy, and no entirely new business line to create. The opportunity was already sitting inside the company. Instead of chasing something new, the buyer focused on what was already there. He trained employees to naturally mention the service during customer conversations. He built a simple follow-up process so it wouldn't be forgotten. He bundled it with the company's core offerings whenever it made sense. Six months later, that same overlooked service represented sixteen percent of total revenue. The growth didn't come from a bold strategic pivot or a revolutionary new idea. It came from paying attention to something the previous owner had simply stopped noticing. That became one of the buyer's biggest post-close lessons. Many buyers spend their time searching for entirely new revenue streams before they've fully understood the opportunities already sitting inside the business they've just acquired. Sometimes the easiest path to growth isn't expansion. It's recognizing what the business already knows how to sell.

1 like • 9d

The part that stood out to me was that the team already knew how to deliver the service. In my experience, getting people comfortable with something completely new can take a long time. Building on something that's already working seems like a much easier place to start after taking over a business.

15d •

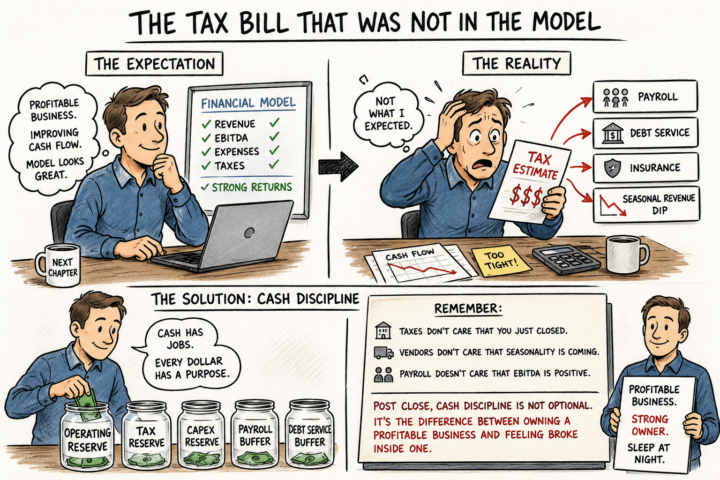

The Tax Bill That Was Not In The Model

The buyer knew taxes were coming. He had accounted for them in his projections and understood they were part of owning a profitable business. What he did not anticipate was how much the timing would matter. The business was performing well. Revenue was steady, cash flow was improving, and the early months of ownership felt encouraging. Then the tax estimate arrived. The amount itself was not catastrophic. The problem was when it arrived. The tax payment landed at the same time as payroll, debt service, insurance renewals, and a seasonal slowdown in revenue. Suddenly, a profitable business felt much tighter than the financial model suggested. As he dug deeper, the buyer realized the previous owner had managed these situations very differently. Sometimes the seller paid taxes late. Sometimes he reduced his personal draws. Sometimes he moved cash between businesses to cover short-term obligations. None of those practices appeared in the financial statements. The model accurately reflected the income. What it did not reflect was the discipline required to manage the timing of cash. That realization changed how the buyer thought about liquidity. He created separate cash reserves for operating expenses, taxes, capital expenditures, payroll, and debt service. He stopped viewing every dollar in the bank account as available money and started treating cash as having specific jobs. That shift transformed how he operated the business. One of the most overlooked post-close lessons is that many cash flow problems are not caused by bad businesses. They are caused by buyers confusing a bank balance with spendable cash. Taxes do not care that you recently acquired the company. Vendors do not care that seasonality is approaching. Payroll does not care that EBITDA looks healthy on paper. Post-close, cash discipline is not optional. It is often the difference between owning a profitable business and feeling broke while operating one.

1 like • 12d

This was a good reminder that the bank balance doesn't tell the whole story. There are always future obligations that still have to be covered, even when things are going well.

14d •

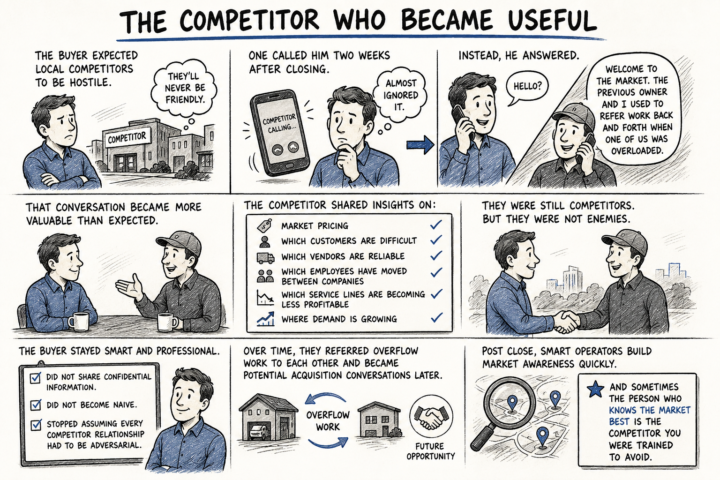

The Competitor Who Became Useful

After closing, the buyer assumed local competitors would view him as the new guy in town and treat him accordingly. He expected distance, suspicion, and maybe even hostility. Then, two weeks after the acquisition, one of his competitors called. His first instinct was not to answer. Fortunately, he did. The conversation started simply enough. The competitor welcomed him to the market and explained that he and the previous owner had often referred work back and forth whenever one business became overloaded. What seemed like a courtesy call quickly turned into one of the most valuable conversations the buyer had during his first few months of ownership. The competitor shared insights that never appeared in diligence reports or market studies. He explained how local pricing really worked. He pointed out which customers were notoriously difficult to serve. He identified vendors that consistently delivered and those that frequently created headaches. He discussed employees who had moved between companies over the years and highlighted service lines that were becoming less profitable as the market evolved. Most importantly, he shared where he believed future demand was heading. They were still competitors. But they were not enemies. The buyer realized that some of the best market intelligence comes from people who have been operating in the same environment for years. They see changes, trends, and challenges long before those things show up in industry reports. He remained professional and careful. He did not share confidential information. He did not assume every competitor relationship would be productive. But he stopped treating every competitor as someone to avoid. Over time, the relationship became genuinely useful. The two businesses occasionally referred overflow work to one another. They exchanged perspectives on market conditions. Years later, the competitor even became a potential acquisition conversation. The experience changed how the buyer viewed competition.

1 like • 12d

The part about answering the phone stood out to me. One small decision ended up creating a relationship that probably wouldn't have happened otherwise.

14d •

Operator Mindset

What is the biggest post-close surprise you think most first-time buyers underestimate? Why?

Poll

3 members have voted

1 like • 12d

I chose Systems. From these posts, it seems like buyers often assume they're acquiring documented processes, but sometimes they're really acquiring years of habits and knowledge that only exist in someone's head.

13d •

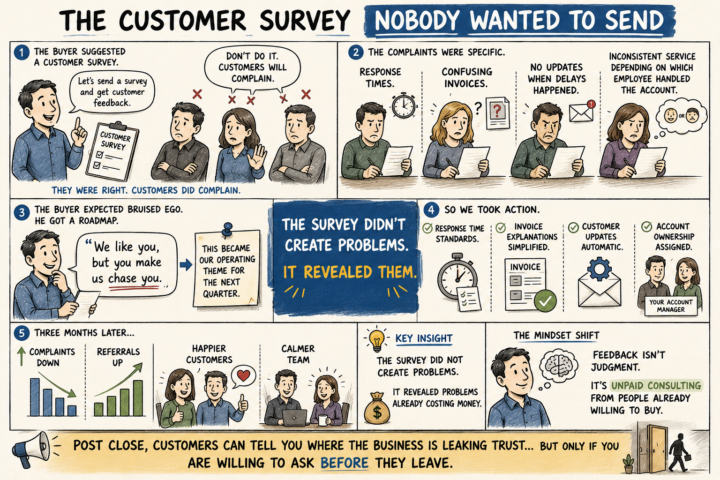

The Customer Survey Nobody Wanted To Send

When the buyer suggested sending a customer satisfaction survey shortly after closing, the team immediately pushed back. They warned him that customers would use it as an opportunity to complain, create unnecessary problems, and damage morale. They were right. The surveys came back with plenty of complaints. But something unexpected happened. The complaints were remarkably consistent. Customers weren't upset about everything. They were frustrated by very specific issues. Response times were inconsistent. Invoices were confusing. Delays weren't communicated. Service quality varied depending on which employee handled the account. The buyer had expected criticism. Instead, he received an operating roadmap. One customer wrote a comment that changed the way he viewed the business. "We like you, but you make us chase you." That single sentence became the company's operating theme for the next quarter. The team established response time standards. Invoice formats were simplified so customers could understand exactly what they were paying for. Automatic updates were sent whenever work was delayed. Every major customer was assigned a clear account owner so there was never confusion about who to contact. Within three months, customer complaints declined significantly. Referrals increased. Employee stress decreased because they were spending less time dealing with frustrated customers. The survey hadn't created new problems. It had simply revealed the problems that were already costing the business money. The team had resisted asking for feedback because they viewed criticism as something to avoid. The buyer saw it differently. Feedback wasn't judgment. It was free consulting from people who had already chosen to do business with the company. That experience became one of his biggest post-close lessons. Customers can often tell you exactly where your business is leaking trust. But only if you're willing to ask before they decide to leave.

1 like • 12d

I liked how the complaints turned into an action plan. Sometimes the uncomfortable conversations end up being the most useful ones.

1-10 of 67

@kevin-mcgee-7313

Looking to escape the corporate world and set my own future. Acquiring businesses truly resonates with me.

Active 9d ago

Joined Mar 9, 2026