Activity

Mon

Wed

Fri

Sun

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

What is this?

Less

More

Memberships

The Funders

53 members • $94/month

Tradeline Secrets

2.6k members • Free

6 contributions to Tradeline Secrets

Apr 28 •

Real Estate Investor Gets $55K at 0% to Buy REOs

Here is a post funding interview with @Jennifer Silletto Jennifer is a licensed real estate agent and REO investor out of Nevada. She came to me after wasting $3,000 with another "business credit guru" who ghosted her for months and never got her a single dollar in funding. 45 days later working with me, she got approved across three 0% business credit cards for $55,000 total. She's now using that funding to buy bank-owned properties in cash, renovate them, and refinance into long-term holds. Every deal she funds with 0% business credit instead of hard money saves her around $8,000 in fees and interest. That's the difference between dealing with a guru selling Paydex scores and Net-30 vendor accounts vs working with someone who's actually been getting people approved for almost a decade. I just dropped the full interview on YouTube where she breaks down: → How she got $55K at 0% in 45 days → Why she stopped using personal credit cards for real estate → How 0% business credit replaces hard money → Her honest take on DIY vs hiring someone who does this every day If you want the same strategy Jennifer used, you already know where to go. Book a call here!

6 likes • Apr 29

[attachment]

4 likes • May 14

Hey Everyone, I have 2 REO's I'm looking at and I need down payment funds to buy the property. Purchase price for one is $125,000 Birmingham, AL (ARV is $250k) and the other is $225,000 Cleveland, OH (ARV is $300k). I will need 15% down for each. Who here would like to deploy their funding and make some interest on it? The one in OH needs LVP in the common areas and sheet rock on the ceiling, which come out to $25-$30k. This will be a buy and hold with sober living as the exit strategy. Home was completely renovated 4 years ago. I plan to flip the one in Birmingham, AL.

Apr 2 •

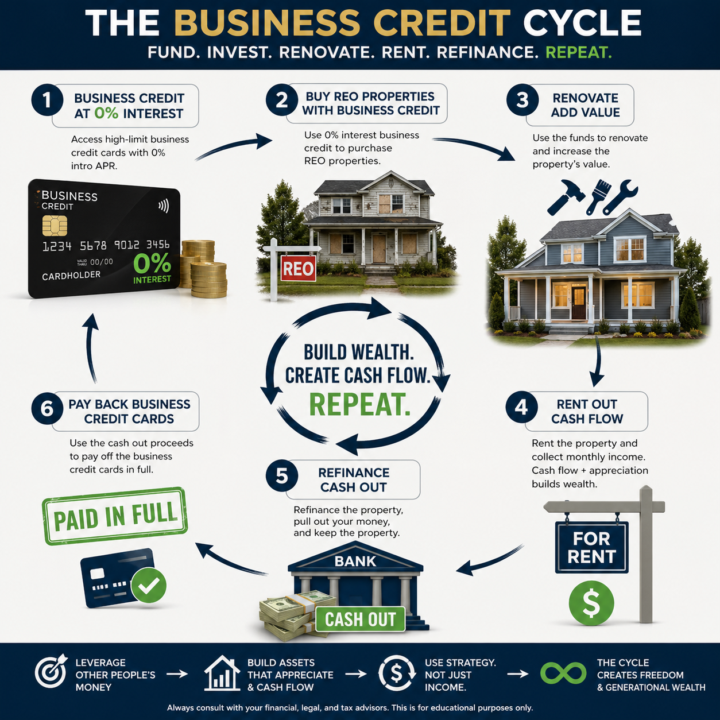

Buying Real Estate With a Credit Card

Here's one of the most underrated deployment plays I've come across: bank-owned real estate (REOs). When a property goes into foreclosure and the bank takes it back, it becomes what's called an REO, Real Estate Owned. Banks aren't in the business of holding property. They want it off their books. That urgency creates buying opportunities that simply don't exist on the open market. We're talking about properties in the $50K–$70K range that cash flow, appreciate, and can be refinanced within 90 days to pull most or all of your capital back out. The strategy works like this: You buy the property, bring in a contractor to renovate, and then refinance at 80% LTV. The refinance pays you back for the purchase and rehab costs, meaning you walk away owning an asset with cash flow and equity, with little to nothing left in the deal. Here's where business credit ties directly into this: Contractors accept credit cards. That means your 0% business credit can cover materials and labor during the rehab window. When the refi closes and the funds hit, you pay the cards off. You just used interest-free capital to bridge a real estate deal. This is exactly the kind of conversation I had recently with one of our community members, @Jennifer Silletto, who has been executing this strategy across multiple properties and has the systems and team in place to walk investors through it. If you're sitting on funding or you're working toward it, this is worth understanding. Drop a comment or connect with me directly if you want to learn more about how she structures these deals.

1 like • Apr 3

@David Ramirez got it

1 like • May 11

you get the funds to buy real estate and I can show you the exit strategy to cash flow. buy to hold or to flip.,

1 like • May 1

@Montrell B I can send you to Greg Silletto at NEXA Lending. [email protected] 951-741-8117 and he can help you with any loans.

1 like • May 3

@Montrell B yes. NEXA Lending is the largest broker in the nation and has 280+ investors so they can do many loan types as well, land, construction, commercial, government etc ..

Mar 23 •

🚨 Investors with FUNDING but no deals? Read this.

🚨 Investors with FUNDING but no deals? Read this. Hi, I’m Jennifer Silletto — REALTOR®, investor, and I specialize in purchasing bank-owned (REO) properties that most people don’t know how to access or win. I know REO's because I am an REO listing agent for the banks. Since October 2023, I’ve personally acquired 15 REO properties across the Midwest. Some I’ve held as rentals, others I’ve flipped — so I’m not just finding deals, I’m actively doing them. Here’s where I come in 👇 I work with investors who:✅ Have access to capital (including 0% business credit 💳)❌ But don’t have consistent deal flow These are bank-owned opportunities that are auctioned online through various platforms, inspected by my contractors, I verify ARV and structure them so you can step in as the buyer. 💼 My role: - Identify and secure the opportunity - Provide deal insight and strategy - Guide you through the process based on real experience ⚡ My strategy: From acquisition → renovation → refinance/flip, my projects are structured to move FAST.I typically target a ~90-day turnaround to refinance and close escrow, leveraging my network of reliable contractors and property co-hosts to execute efficiently. 💰 My fee: - $15,000 consulting fee per deal (JV Agreement signed) - Paid at closing + refinance 🏠 Your role: - You take title - You control the project - You fund the deal - You keep the upside This is ideal for someone who wants access to real deals AND a clear execution path — not just a random property. If you’re working with funding (especially through David’s 0% credit strategy) but need actual properties to deploy it, this is where we can collaborate. 📩 Comment “DEALS” or message me directly and I’ll walk you through current opportunities. Let’s put your capital to work. My strategy has been to BRRR and I am able to get most if not all of my initial investment back. I can provide property addresses and photos.

1 like • Mar 24

@Troy Johnston StackEasy.ai I live in Las Vegas. I don't invest where I live because the numbers do not make sense. The numbers make sense in the Mid West. Also, using 0% credit cards (liquidate) and use as a down payment or buy in full is easier when the properties are under $100k. Repairs are also not too crazy expensive. You can pay for renovations using the 0% credit cards. I have a spreadsheet of properties I am interested in. I have my contractors go and view the interior of the property so we know how much renovations is needed. Once I win the bid. It takes about 30 days to close escrow on the purchase. I provide a service and hence I charge a consulting fee. I can help nationwide but that is only with how to make bids on REO's.

Mar 21 •

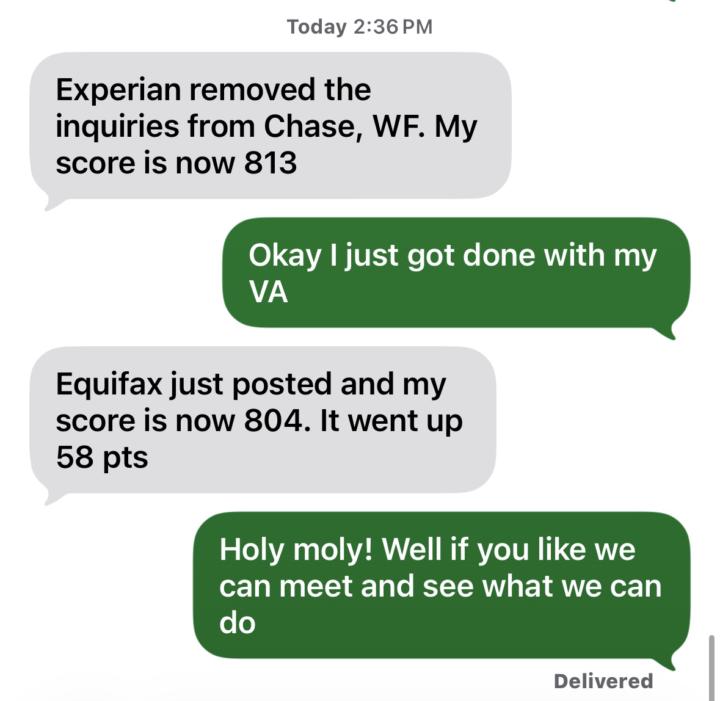

The Plan Is Simple

Remove the inquiries. Let the score update. Stack the funding. That's it. This client had Chase and Wells Fargo inquiries dragging them down. We got Experian to remove them score jumped to 813. Then Equifax posted and they went up 58 points to 804. Now we meet and see what we can do with those numbers. I do this all the time. The plan isn't complicated. The execution is what matters.

1 like • Mar 23

I can vouch for this as it is my text message to David!

1-6 of 6

@jennifer-silletto-6608

Realtor, licensed since 2001 in CA & NV, I acquire REO's & BRRR them as MTR & LTR primarily in So IN. Former LO w/ deep financial & U/W experience.

Active 12h ago

Joined Mar 21, 2026

Powered by