Activity

Mon

Wed

Fri

Sun

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

What is this?

Less

More

Memberships

Boulder Partners

6 members • Free

The Book of Life

8 members • Free

The Vitality Society

28 members • $170

MJ

Ms. Jane's English Room

2 members • Free

OpenClaw and Autonomous AI

72 members • Free

Beyond Burnout

25 members • Free

The League of Heroes!

4 members • Free

1 contribution to Boulder Partners

19h •

Weekly update 2/27/2026

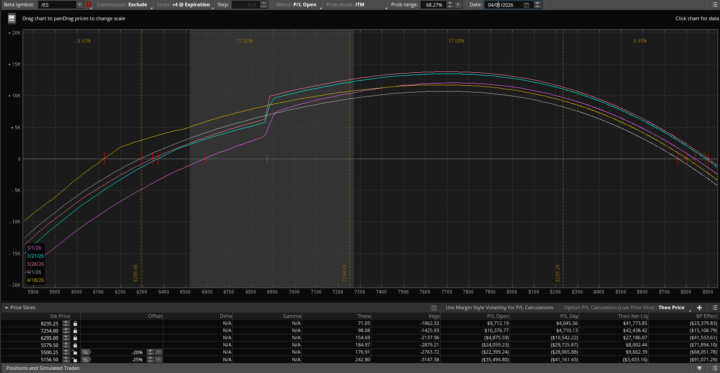

Purchased a debit spread on /CL futures as a hedge against possible war with Iran. Current beta weighted risk is 2.62 against the SPX. Overall theta on futures is 98.63. SPX beta weighted risk ~$18,022. All else being equal, this represents $2,958.90 every 30 days due to theta decay~7.8% monthly. Of note, beta weighted portfolio value is remains close to the current futures balance ($19,948.31). The attached graph shows the current stress test with losses beginning at /ES price of $6,875.25 (which appears to increase with volatility). It has a 5.03% chance of loss over the next 30 days.

1 like • 13h

Love this kind of breakdown, Greggory. It’s not just the trade it’s the way you explain the risk, theta, probabilities… that’s what really builds trust in a community like this. If you keep packaging these weekly updates in a simple structure, it’ll help newer members follow your thinking and not just the numbers. That’s how a group goes from watching trades to actually learning. You’re building this the right way.

1-1 of 1

@innocent-community-growth-2550

Helping community owners activate and scale their spaces, turning visions into thriving, engaged communities.

Active 2h ago

Joined Feb 27, 2026