Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Memberships

Synergy4life Credit Academy

94 members • Free

BSA

342 members • Free

3 contributions to Synergy4life Credit Academy

12d •

🎯 Lock In Your Target! 🎯

Hey everyone! Welcome to Day 2 of our engagement series! 👋🏼✨ Now that the introductions are out of the way, it’s time to move past small talk and get straight to strategy. Your journey continues today by defining the exact target you are chasing. Plain and simple: if you don’t know what your target is, you can’t hit it. Whether you need a 750+ credit score to leverage OPM (Other People's Money) or you're looking to secure your first $50k in business funding, we need to define it today. Vague goals get vague results—so let’s get crystal clear. 👇🏼Comment Section: What is your #1 credit or business goal for the next 90 days? Be specific so the community can support you, give feedback, and help you connect! 🙌🏼 • Example 1: "Clean up 3 negative items on my report." • Example 2: "Structure my LLC to get approved for a business line of credit." New members and OGs, drop your 90-day target below let’s lock in, network, and win together!👇🏼✨

1 like • 10d

I need to file CFPB disputes. Do I upload copy of the credit report or just a brief description of the nature of the problem?

0 likes • 6d

@James Terry got it coach tyty

May 19 •

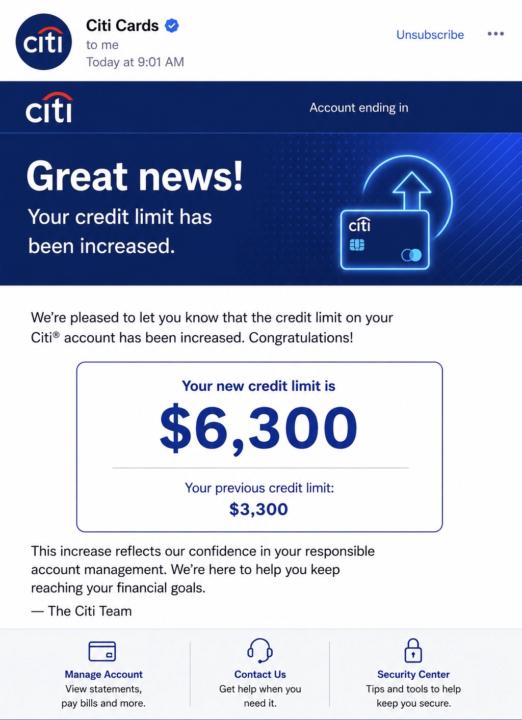

🔥 Credit Line Increase Strategy: How to Ask Like You Know What You’re Doing

A lot of people want higher credit limits, but they ask at the wrong time. They ask when utilization is high. They ask after missed payments. They ask with no prep. Then they get denied and think the bank is against them. Credit line increases are not random. They’re timing, behavior, and positioning. Here’s the clean strategy: 1. Get your utilization under control first Before you ask for an increase, try to get that card balance as low as possible. Best zone: 1%–9% utilization Acceptable zone: under 30% Danger zone: over 50% If your card is maxed out or close to maxed out, the bank may see you as needing credit instead of managing credit. 2. Make sure your payment history is clean Do not request an increase if you recently missed a payment. Most lenders want to see: - On-time payments - Responsible usage - No recent returned payments - No over-limit activity - No recent hardship/payment plan activity You want your profile to look calm, stable, and low-risk. 3. Wait for the right timing Don’t ask every 30 days. A cleaner rhythm is usually: 90–180 days after opening the cardor90–180 days after your last increase Some banks are more generous than others, but the strategy is the same: give them enough positive history to justify the increase. 4. Use the card, but don’t abuse the card Banks like activity. They want to see the card being used, but they don’t want to see desperation. Good example: - Use the card monthly - Pay it down before the statement closes - Let a small balance report if needed - Keep the account active and healthy Bad example: - Max it out - Pay minimums only - Ask for more credit while carrying high debt 5. Ask clean When you request the increase, keep it simple. You do not need to over-explain. Example script: “I’ve maintained responsible payment history and would like to request a credit line increase based on my account performance and current financial profile.” That’s it. Clean. Professional. No begging.

0 likes • May 19

🔥

May 18 •

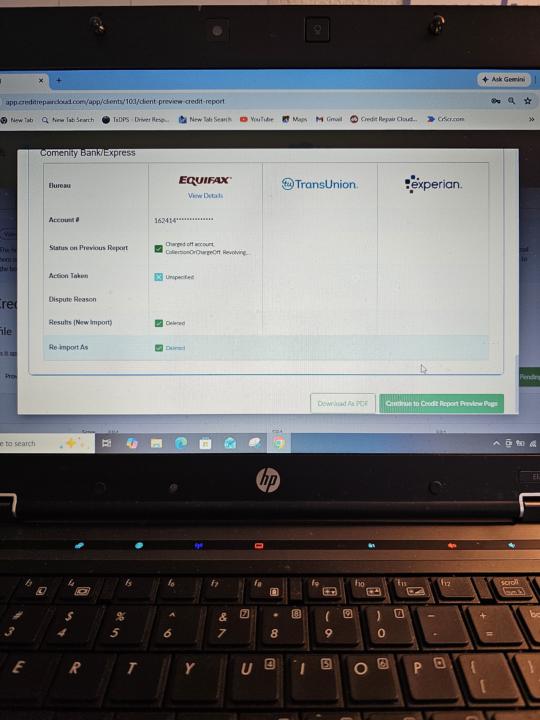

Wins for Johnson Credit Services

Hello fellow Snergy4Life community!!! I have a few great wins that I would like to share. After a great 1 on 1 mentor call with our coach James I have had some great results getting charge offs deleted. He explained that accuracy across all 3 bureaus is the key. Look for the inaccuracies and dispute dispute dispute... Be encouraged and have a great day 😊

1 like • May 19

@James Terry yes sir.

1-3 of 3

Active 3d ago

Joined May 10, 2026