Activity

Mon

Wed

Fri

Sun

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

What is this?

Less

More

Memberships

Acquisition Operator Network

14 members • Free

41 contributions to Acquisition Operator Network

2d •

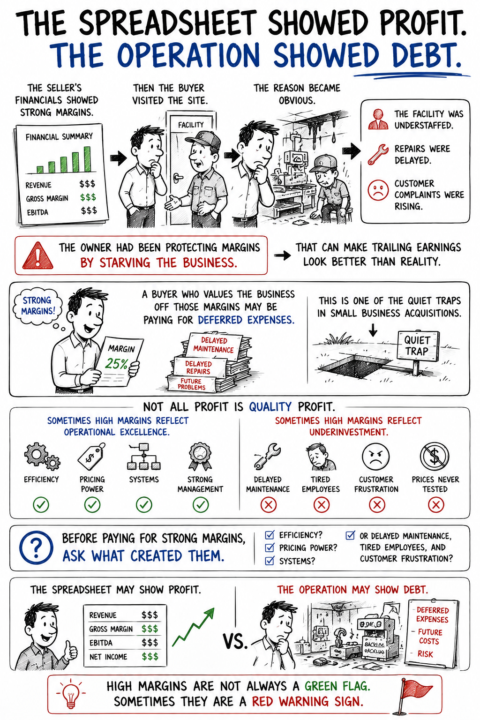

The Spreadsheet Showed Profit. The Operation Showed Debt.

The seller’s financials showed strong margins. Then the buyer visited the site. The reason became obvious. The facility was understaffed. Repairs were delayed. Customer complaints were rising. The owner had been protecting margins by starving the business. That can make trailing earnings look better than reality. A buyer who values the business off those margins may be paying for deferred expenses. This is one of the quiet traps in small business acquisitions. Not all profit is quality profit. Sometimes high margins reflect operational excellence. Sometimes they reflect underinvestment. The difference matters. Before paying for strong margins, ask what created them. Efficiency? Pricing power? Systems? Or delayed maintenance, tired employees, and customer frustration? The spreadsheet may show profit. The operation may show debt

0 likes • 2d

Not all profit is quality profit is probably the biggest takeaway here. Strong margins are great if they come from good systems and execution. They’re a lot less impressive if they come from burning out staff and ignoring maintenance for years.

4d •

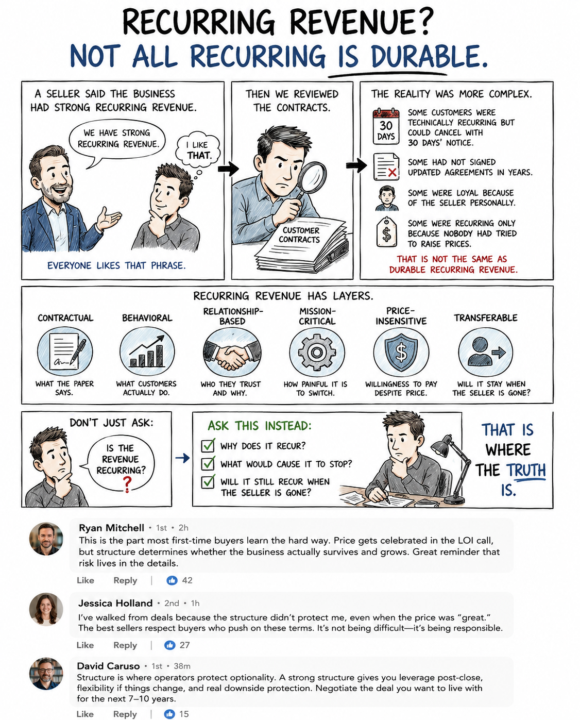

Recurring Revenue? Not All Recurring Is Durable.

A seller said the business had strong recurring revenue. The buyer liked that phrase. Everyone likes that phrase. Then we reviewed the contracts. Some customers were technically recurring but could cancel with 30 days’ notice. Some had not signed updated agreements in years. Some were loyal because of the seller personally. Some were recurring only because nobody had tried to raise prices. That is not the same as durable recurring revenue. Recurring revenue has layers. Contractual. Behavioral. Relationship-based. Mission-critical. Price-insensitive. Transferable. A buyer should not simply ask, “Is the revenue recurring?” A buyer should ask, “Why does it recur, what would cause it to stop, and will it still recur when the seller is gone?” That is where the truth is.

0 likes • 3d

Honestly, this post made me realize how easy it is to confuse consistency with durability. A customer paying for years feels safe on paper, but if pricing has never been tested, contracts are weak, or the seller relationship is the glue holding everything together, that recurring revenue may not survive a transition nearly as well as people assume.

5d •

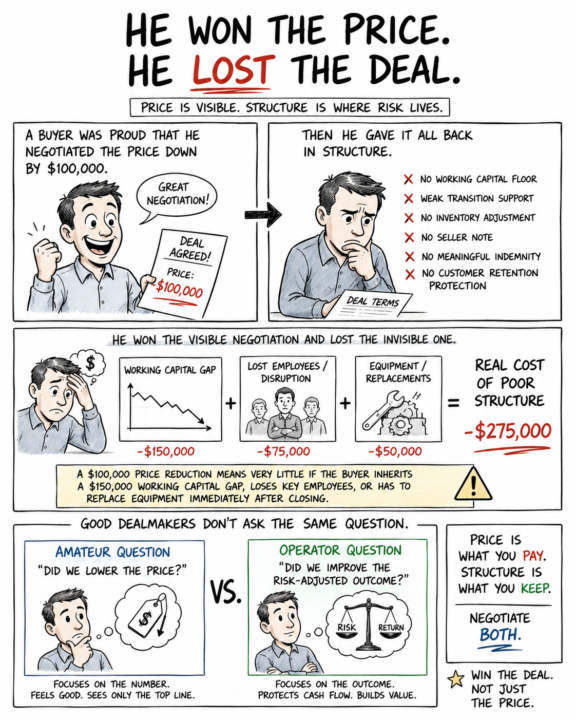

He Won The Price. He Lost The Deal

A buyer was proud that he negotiated the price down by $100,000. Then he gave it all back in structure. No working capital floor. Weak transition support. No inventory adjustment. No seller note. No meaningful indemnity. No customer retention protection. He won the visible negotiation and lost the invisible one. That happens often. Purchase price is emotionally satisfying because everyone can see it. Structure is quieter. But structure is where risk lives. A $100,000 price reduction means very little if the buyer inherits a $150,000 working capital gap, loses key employees, or has to replace equipment immediately after closing. Good dealmakers do not ask, “Did we lower the price?” They ask, “Did we improve the risk-adjusted outcome?” Those are not the same question.

2 likes • 4d

This is the part most first time buyers learn the hard way. Price gets celebrated in the LOI call, but structure determines whether the business actually survives and grows. Great reminder that risk lives in the details.

6d •

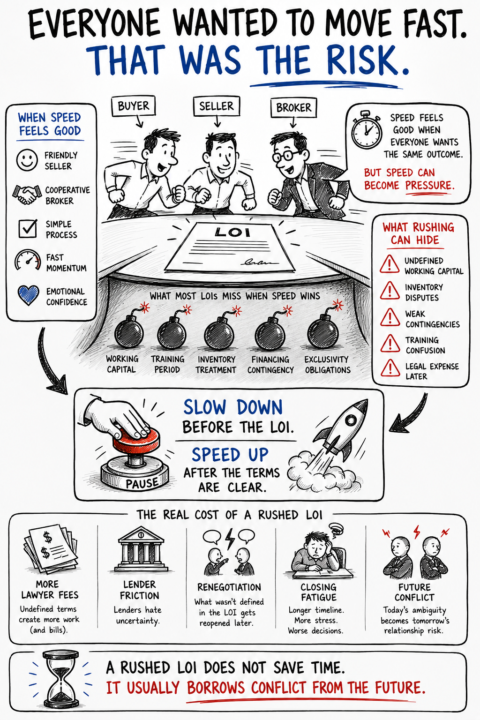

EVERYONE WANTED TO MOVE FAST. THAT WAS THE RISK.

The buyer wanted to move quickly. The seller wanted to move quickly. The broker wanted to move quickly. That was the problem. Speed feels good when everyone wants the same outcome. But speed can become pressure. One buyer almost signed an LOI without defining working capital, training period, inventory treatment, financing contingency, or exclusivity obligations. The deal felt simple because the parties liked each other. Liking each other is not a substitute for clarity. The best time to define hard terms is when everyone is still cooperative. Once money is spent, lawyers are involved, lenders are waiting, and closing fatigue sets in, every undefined term becomes more expensive. Slow down before the LOI. Speed up after the terms are clear. That is the rhythm. A rushed LOI does not save time. It usually borrows conflict from the future.

0 likes • 5d

I really appreciate how this frames speed as something that should follow precision, not replace it. There is a tendency to think moving quickly creates efficiency, but in many cases it simply postpones complexity until the stakes are higher. Defining difficult terms while trust is still high seems less like slowing down and more like protecting the deal from avoidable downstream erosion.

7d •

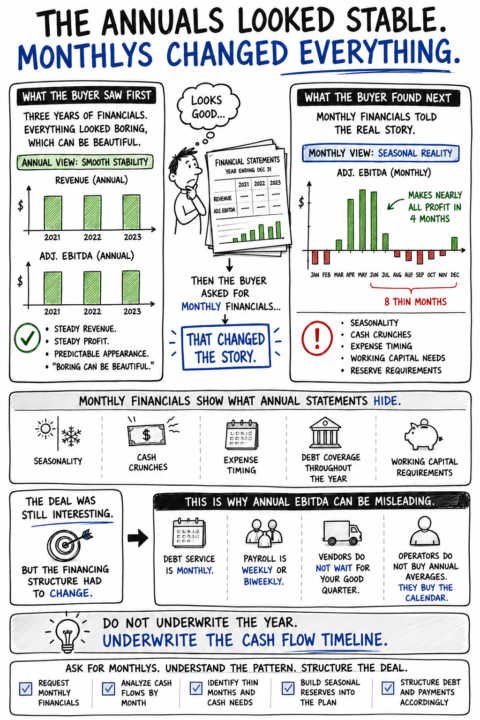

The Annuals Look Stable. The Calendar Tells the Truth.

The buyer asked for three years of financials. The seller sent them. Revenue was steady. Profit was steady. Everything looked boring, which can be beautiful. Then the buyer asked for monthly financials. That changed the story. The business made nearly all its money in four months. The remaining eight months were thin. On an annual basis, it looked stable. On a monthly basis, it required cash discipline and seasonal reserves. The deal was still interesting. But the financing structure had to change. Monthly financials show what annual statements hide. They reveal seasonality, cash crunches, expense timing, and whether the business can support debt throughout the year. This is why annual EBITDA can be misleading. Debt service is monthly. Payroll is weekly or biweekly. Vendors do not wait for your good quarter. Operators do not buy annual averages. They buy the calendar

1 like • 6d

This is such a strong example of why averages can create false confidence. Annual stability can smooth over operational realities that become extremely important once debt, payroll, and reserves enter the equation. Looking at monthly patterns feels less like accounting detail and more like understanding the actual rhythm the operator will inherit.

1-10 of 41

@charles-trotter-9675

Looking to grow via Acquisitions and build Generational Wealth

Active 2d ago

Joined Mar 8, 2026