Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Memberships

The Hard Money Room

22 members • $47/month

1 contribution to The Hard Money Room

19h •

CPI Falls to 3.5%, Largest Drop Since 2020, BTC Pops Above $64K 📈🟠

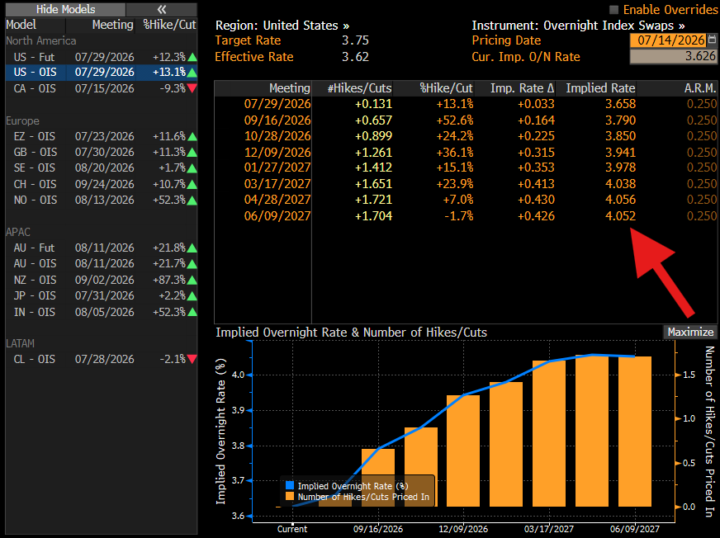

June CPI fell 0.4% month over month. First monthly decline since 2020. Core came in flat against expectations of +0.2%, and the annual rate dropped to 3.5% from 4.2%. Bitcoin popped above $64,000 on the print. Here's what actually happened, and here's why it matters more than the headline. /// THE OIL SHOCK IS WORKING ITS WAY OUT The single biggest drag was gasoline, down nearly 10%, the largest drop since 2022. That's the Iran war energy shock washing out of the data. This is the pipeline I've been hammering for weeks. Oil spikes, it feeds inflation with a lag, inflation dictates the Fed, the Fed dictates liquidity, liquidity dictates Bitcoin. June is the receipt. The shock went in, and now you can watch it come out the other end. /// WHAT THE FED PRICING ACTUALLY DID Read this part carefully, because most people have it backwards. Nobody was pricing cuts. The market was pricing hikes. Going into this print, July hike odds sat at 42%. Waller was out saying the Fed may need to raise to tame core. The June dot plot had 9 of 19 members projecting a 2026 hike. After the print, July hike odds collapsed to 17%. The tightening threat that has been sitting on every risk asset just got knocked down hard. Treasury yields fell, stocks rose, Bitcoin ripped through $64K. /// WHERE THIS GOES NEXT Here's the call. If disinflation continues, the last hike comes off the table too. Once you're pricing zero hikes with a cooling labor market underneath, the conversation turns to cuts. That's the path I've been pointing at. The honest caveat: this is round one of the oil shock, not the end of it. Trump reinstated the naval blockade, Brent pushed back above $85, and the gasoline drop that flattered this number can reverse fast. Traders still see roughly a 60% chance of a hike by September. Annual core is still 2.6%. The pipeline isn't finished. It's reloading. /// WHAT I'M WATCHING The Fed on July 28-29 with the hike threat defused for now. Then whether round two of the oil shock shows up in the July and August prints.

0 likes • 10h

Could the oil shock be working its way back in? Gas prices spiked (here) nearly 10% late last week following resumed bombing. This being just ahead of today's print apparently didn't negatively effect it because it CPI is rearward looking. I'm gathering that closing the straight and the immediate rise in oil prices will likely add another 10% at the pump this week. To me that makes the next print (being rearward looking at now) likely to be ugly. Won't this increase the odds of hikes later in the year?

1-1 of 1

Active 10h ago

Joined Jul 2, 2026

Finger Lakes NY & FL

Powered by