Activity

Mon

Wed

Fri

Sun

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

What is this?

Less

More

Memberships

Cloud Residents · US Credit

754 members • Free

27 contributions to Cloud Residents · US Credit

1d •

Amex Biz Plat ECs for NRAs

Help! I've been getting a juicy offer that I don't know if I can actually take. The offer: 15K MR on $4K spend, per employee card, max 5 ECs now require SSN to activate apparently per chat/phone reps. All say NRA ECs not possible without SSN Ironic bc as a primary card holder, I only needed passport, ITIN and proof of address. Something doesn't make sense. Is there a work around?

7d •

Credit Limits Without a Hard Pull

Most banks are still using the income you told them years ago. That outdated number is quietly capping your credit limits. Here's the full playbook to stack soft pull increases across your cards. Update Your Income First Go into every bank app and refresh your income. If you have household income, include it. You're not lying. You're just not selling yourself short. Banks won't raise what they don't know about. Request the Increase Most banks do credit limit increases with a soft pull. Your score stays exactly where it is. And don't ask for a tiny bump. Ask for 2X to 3X your current limit. They'll either approve or counter-offer. Either way you come out ahead. Get the Timing Right This is where people mess up. Wait at least 3 statement cycles on a new card before requesting. After that, request increases every 30 days. A lot of banks say 6 months, but you'd be surprised how many will approve back-to-back increases if your credit file supports it. Use the Card For the next 2 to 3 months, make that card your workhorse. Gas, groceries, bills, subscriptions. Spend, pay it off, spend again in the same cycle. One or two cycles of heavy usage is enough. Don't carry a balance. Just show activity. Never Accept a Low Limit Quietly If you get approved for a limit that feels low, call in. Give a real reason. A trip, a wedding, a big life event. That one call can take you from USD 5,000 to USD 10,000 or more. Move Limits Between Cards Here's the thing most people don't know about. If you have one card with a high limit you don't fully use, you can shift that limit to a new card at the same bank. That's how people go from USD 5,000 limits to USD 50,000+ on the same accounts. No new application required. For Cloud Residents building credit with an ITIN, these moves matter even more. Soft pulls protect your file from hard inquiries while it's still growing. Strategic limit increases signal trust to other banks. And a thicker profile with higher limits opens doors to better cards down the line.

Poll

20 members have voted

0 likes • 1d

Related comment / Q Interesting you said to include household income. When I did my very first Amex GT app, I included and may have inflated household income a bit. But since I had used that number for the first app, I did it for EVERY app after without reducing in fear it would raise flags. Maybe trigger an FR accidentally. Despite some strong advice from someone who I trust a lot who recommends to lower the income amount in my Amex profile or on a subsequent app, I have not done so bc of my fear of an FR. I dont wanna trip the system and trigger something. So far I have 4 Amex cards (Brill, HH NF, BBP, ABP). Just applied for 2 more that are pending. Again with the same household income amt as my very first app. Am I safe to go on with THAT original income amount?

0 likes • 1d

@John Flack Haven't calculated it. What's a safe ratio threshold?

8d •

The unwritten Amex rules no one tells you

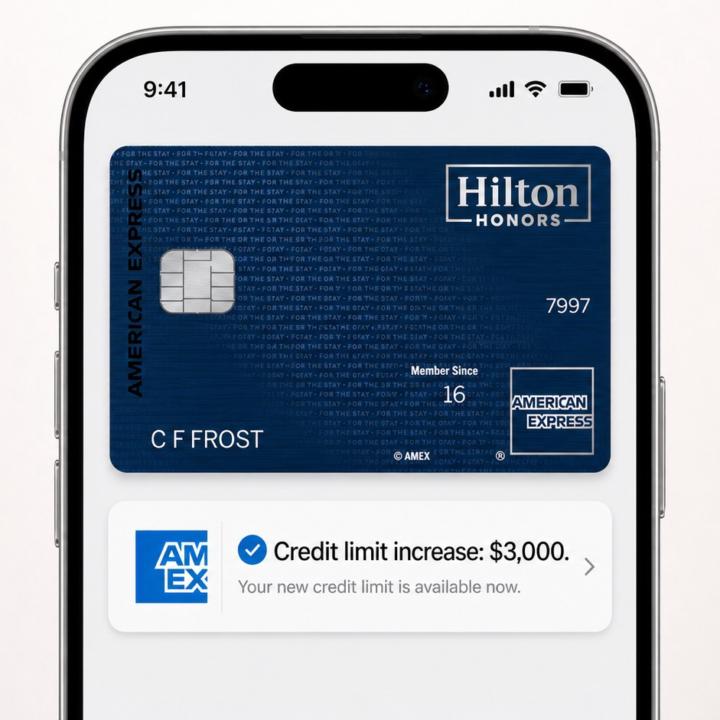

Amex has a system. It is not just about your credit score or your payment history. There are unwritten rules that trigger account restrictions, spending power cuts, and full shutdowns with zero warning. If you are building with Amex as a Cloud Resident, you need to know all of em. 1. Too many retention offers The Amex Platinum fee is nearly USD 1,000 a year. When the annual fee hits, calling and asking for a retention offer - points, statement credits, anything to offset the cost - is fair game. But if you do it every single year, Amex stops seeing you as a valuable customer. They flag you as someone who costs more than you are worth. That lands you in what people call Amex jail. The right play: ask when there is a real fee hike or a genuine reason or every other year. Do not make it an annual habit. 2. Maxing out your Amex credit cards Amex has two card types and they treat them differently. - Charge cards (Platinum, Gold) have no preset spending limit. - Credit cards (Blue Cash, Hilton) have a hard limit. If you max out your Amex credit card, they do not just care about that one card. They will reduce your spending power on your charge cards too, and those restrictions stay until the credit card is paid off in full or most of it. Keep utilization low, especially on the credit card side, or your charge cards will feel it. 3. The RAT team - reward abuse team There is an actual internal team called the Reward Abuse Team. If you have seen the trick floating around social media - buy gift cards, convert to money orders, use money orders to pay the credit card - Amex has already caught on. The RAT team does not send warnings. They close every card on your account, sometimes the entire account itself, the moment they see it. Manufactured spend is a tightrope. Obvious cycling of gift cards through money orders is a guaranteed fall. 4. Bounced/Returned or late payments This one catches people by accident, but Amex does not care about intent. A single bounced payment can trigger a shutdown. Multiple late payments almost certainly will.

Poll

28 members have voted

1 like • 1d

Generally found if I have charges and pmts WITHIN billing cycle, so that statement cuts with low utilization, I have often gotten auto credit limit increases. I guess Amex rewards large spend AND large payments WITHIN cycle with higher CL. I've gotten this 3x across 3 players in the last 12 months. Has anyone else got Auto CL increases from Amex? And if so, did you notice a pattern in your spend or any pattern that triggered the increase?

0 likes • 1d

Another thing I didn't know, and I MAY test is the retention offer request. I got one last year for the Brilliant. And with high spend, thinking to ask again this year. My spend justifies my ask I feel. Am I wrong to ask 2 years in a row?

Oct '25 •

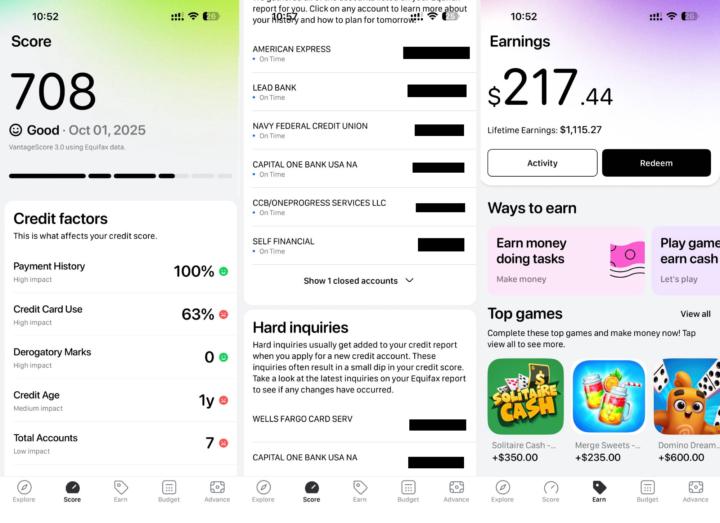

How to Check ITIN Credit Scores Online: My Proven 6-Method Guide

If you're an ITIN holder like me—navigating US credit without an SSN—tracking your score is key to unlocking bank accounts, credit cards, and loans. I've tested these 6 reliable online methods myself, and they're perfect for non-US residents. As of October 2025, they're free or low-cost and skip most verification headaches. Pro tip: Wait for at least 6 months of credit history, and use a US VPN to avoid access issues. Quick Overview of My Go-To Methods: - Equifax.com: My top pick overall. Sign up with your ITIN in the SSN field for a free VantageScore 3.0 and monthly credit report. Upgrade to Premier ($19.95/month) for all three bureaus. If it flags your account, DM @Equifax on X (Twitter) - they fix it fast. - Experian Online Form: Totally free—upload your passport, address proof (like a bank statement), and ITIN letter (CP-565). They'll mail your full report in 7-12 days. Super secure, no need to snail-mail docs. - True Finance App: Easy signup shows your Equifax VantageScore and full file monthly. Great for quick checks on accounts and utilization. Bonus: It's also a cashback app where I earned $1,115 in rewards over the last few months via games, tasks, and surveys. - myFICO Free Plan: Delivers Equifax FICO 8 score with monthly alerts. New accounts often pause—call support; they reactivate in minutes with basic questions. Premier ($39.95/month) covers all bureaus. - Credit Karma: Updates Equifax VantageScore every few days with real-time alerts for new accounts or inquiries. Free pre-approvals for cards (after 6 months history)—handy for testing options. - Bilt Rewards App: Monthly Experian FICO 9 score, plus easy + Bilt Mastercard (via Wells Fargo). Ideal if you're into rewards. Key Notes: Mix and match these for full coverage across bureaus—don't rely on one. What's your experience with ITIN credit tracking? Drop a comment if you've tried any, or if you need tips on getting started. Let's help each other build that credit! 🚀

1 like • Feb 19

@Ain - Cloud Resident ✋ I'm running into errors too for the $1 offer. Payment fails. CC shows pending charge and pending refund. Tried 10x using different CCs. Not a CC issue as far as I can tell. Customer service call center says it's an error with either of both of experien and TransUnion. Used @Aaron Ng 's advice to FBM them, waiting on a reply.

0 likes • 1d

For Experien, it's great to have the upload option but if I'm reading correctly, they send you a hard copy of your report? Is there an online option? As an NRA, the hard copy mailed to me is much less secure as I am not physically there.

2d •

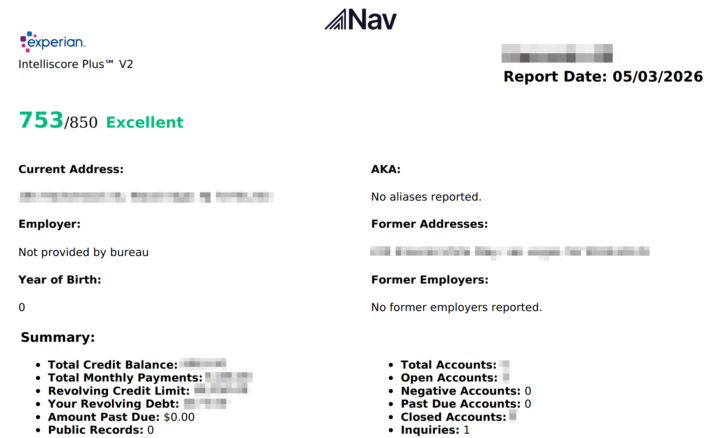

Experian Credit Score With Your ITIN (via Nav)

Most ITIN holders assume they can't see their Experian credit file online without a Social Security Number. You can. Sometimes. Shoutout to @momo for surfacing this method here first. Here's the updated standalone guide. Go to Nav.com, sign up for the free plan. You'll enter your name, DOB, address, and ITIN. Nav runs an Experian soft pull for identity verification and you're in immediately. If not, you can always retry. Once you're in, here's what Nav shows you: - VantageScore 3.0 from Experian - Score Factors - Payment History - Debt Usage - Credit Age - Account Mix - Debt vs Income - Hard Inquiries count - Current Address - Former Addresses Debt Usage drill-down: revolving credit limit, usage percentage, total revolving debt. Account Mix drill-down: split into mortgage, auto, revolving, and other accounts. Inquiries drill-down: total inquiries vs how many actually impact your score. Summary page: date of your first credit account, total balance across all accounts, total minimum monthly payments. Downloadable full report in PDF. This is genuinely useful if you're building US credit remotely and want to see where Experian has you — especially before applying for new cards. Now the caveats, because this matters. Nav's ITIN access for Experian is hit or miss. Some get through on the first try. Others don't, no matter what. If Nav doesn't work for you, alternatives exist: - Experian credit report by mail - Experian through Equifax Complete Premier - Experian FICO 9 through the Bilt app One more thing: VantageScore is not FICO. Almost all lenders pull FICO models when you apply. Nav's VantageScore 3.0 is directionally accurate, but don't treat a 720 VantageScore as a guarantee you'll get approved. Use it to track trends, not to predict underwriting decisions. If you try Nav with your ITIN - drop a comment below.

Poll

26 members have voted

0 likes • 1d

,🙏Gonna try Nav and report back.

1-10 of 27